Introduction

Midtown Manhattan is one of the most active commercial real estate markets in the world — and right now, it's a buyer's market in ways that haven't existed in years. Post-pandemic repricing, distressed asset sales, and a flight to quality have reset valuations across multiple asset classes. Occupancy is recovering, but prices haven't fully caught up yet.

Cushman & Wakefield's Q4 2025 Manhattan Office MarketBeat puts Midtown office inventory at 261 million square feet — roughly 63% of Manhattan's total office stock. That scale, combined with ongoing market bifurcation, means buyers who know where to look are finding opportunities that simply didn't exist five years ago.

This guide covers the state of Midtown's commercial market, property types available, key submarkets, what buyers must evaluate before signing, and how to approach a purchase with confidence.

TLDR

- Midtown holds ~63% of Manhattan's office inventory, with Class A assets absorbing 84.9% of new leasing activity

- Q4 2025 sale comps range from $233/SF to $526/SF depending on asset quality and submarket

- Distressed properties trading at deep discounts are creating genuine value-add opportunities for prepared buyers

- NYC's mortgage recording tax adds 2.55% of the loan amount as a buyer closing cost — model it before committing

- Off-market deals dominate — access depends entirely on your advisor's relationships

Why Midtown Manhattan Remains a Top Commercial Real Estate Market

Midtown's dominance is structural. The submarket holds the highest concentration of financial institutions, professional services firms, and corporate headquarters in the country — demand that has persisted through multiple economic cycles, including the post-pandemic reset.

The Flight to Quality Bifurcation

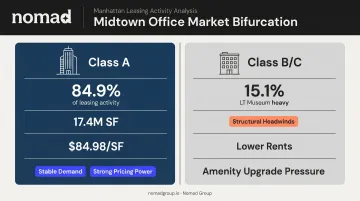

The post-pandemic market didn't weaken Midtown uniformly. It split it. According to Cushman & Wakefield's Q4 2025 data, Class A leasing accounted for 17.4 million square feet — or **84.9% of all Midtown leasing activity**. Overall asking rents across Midtown averaged $76.03/SF, while Class A commanded $84.98/SF.

That gap shapes decisions on both sides of the market. Class B and C assets face structural headwinds, while well-positioned Class A properties maintain pricing power. Tenants evaluating Midtown space should factor in where a building sits in this split — Class A assets signal stability for long-term leases, while landlords holding secondary stock may need to compete on price or amenity upgrades to retain occupancy.

Return-to-Office as a Demand Tailwind

Major financial employers have been pulling workers back. JPMorgan moved toward broader five-day office attendance in 2025. BlackRock implemented a four-day in-office requirement in 2023. The cumulative effect on leasing is measurable: Colliers reported Manhattan Q4 2024 leasing hit 10.21 million square feet — the strongest quarter since 2019 — with full-year 2024 leasing reaching 33.34 million square feet.

RTO mandates translate directly into leasing conviction. Companies making multi-year in-office commitments need space that supports that culture — and they're willing to sign longer terms to secure it. For landlords, that means more predictable occupancy; for tenants, it means competition for quality space is real and accelerating.

Infrastructure No One Can Replicate

Grand Central Terminal and Penn Station together serve hundreds of thousands of commuters daily. Midtown sits within reach of three major international airports. This transit density is irreplaceable for companies requiring accessibility for employees spread across the tristate area — and it creates a demand floor that suburban markets simply don't have.

Types of Commercial Properties for Sale in Midtown Manhattan

Midtown's for-sale market isn't monolithic. Different asset classes attract different buyer profiles, and each comes with distinct underwriting considerations.

Office Buildings and Office Condominiums

Full office building acquisitions typically suit institutional capital or large owner-occupiers seeking to control an entire asset. Pricing from Q4 2025 verified transactions shows meaningful range:

| Property | Sale Price | Price Per SF |

|---|---|---|

| Two Grand Central Tower | $273.0M | $432/SF |

| 75 Rockefeller Plaza | $200.0M | $526/SF |

| 845 Third Avenue | $79.9M | $233/SF |

Office condominiums — where buyers purchase individual floors or strata units within a building — lower the entry threshold significantly. They're common in Midtown and typically attract owner-occupiers, professional service firms, and family offices that want to own their headquarters without taking on full-building risk.

Retail and Mixed-Use Properties

Ground-floor retail condos in Midtown's high-foot-traffic corridors remain compelling for national retailers, restaurant groups, and financial services branches. Cushman & Wakefield's Q4 2025 retail data shows the corridor spread clearly: Upper Fifth Avenue averages $2,394/SF in asking rent, while Third Avenue runs closer to $251/SF. Pricing is driven by frontage, pedestrian volume, and visibility.

Mixed-use properties — commercial lower floors with residential or hospitality above — have attracted investors who want to diversify income streams and reduce vacancy risk. These require buyers comfortable navigating both commercial and residential/hospitality regulation at once.

Distressed and Value-Add Assets

Midtown's post-pandemic repricing has surfaced genuine distress. Recent transactions illustrate the range:

- 135 West 50th Street, a 23-floor office building, sold at auction at a 97.5% discount — bidding opened at $7.5 million

- 1740 Broadway (Blackstone's defaulted loan) traded at roughly a 50% discount, per PERE Credit

These aren't average market conditions — they're property-specific situations. But they signal that over-leveraged owners are still working through their capital stacks, and well-capitalized buyers with repositioning expertise have a real acquisition window.

Key Midtown Submarkets to Know Before You Buy

Geography shapes value more than almost any other variable in Midtown. The same building quality can trade at dramatically different prices depending on which blocks it sits on.

Grand Central / East Midtown

Landmark towers along Park Avenue, Lexington Avenue, and the Grand Central hub define Midtown's most established office corridor. The NYC Department of City Planning's Greater East Midtown Rezoning has unlocked significant modernization capacity, enabling transfers of unused landmark development rights tied to public-realm improvements. The practical result is a mix of new-build development sites and repositioning plays in aging existing stock.

Nomad Group has direct operational experience here, including asset management work at 11 East 44th Street — used as swing space during a tech client relocation. For buyers, the corridor's combination of transit access and rezoning-driven upside makes it one of the more active repositioning markets in Manhattan.

Fifth Avenue / Plaza District

The Plaza District is Midtown's prestige address tier. Buyers here are typically institutional investors or ultra-high-net-worth individuals, and yield takes a back seat to trophy positioning and tenant quality. A few realities to factor in:

- Highest price per square foot in Midtown, often by a significant margin

- Tenant rosters typically include law firms, financial services, and Fortune 500 headquarters

- Competition at acquisition is intense; off-market relationships matter more here than anywhere else in the corridor

Midtown South: NoMad and Flatiron

Midtown South deserves separate attention from traditional Midtown. Cushman & Wakefield puts Midtown South inventory at 73.5 million square feet, with an overall asking rent of $83.58/SF and Class A at $105.64/SF — higher than traditional Midtown Class A averages.

Colliers reported Midtown South Q4 2025 leasing demand at 4.43 million square feet, up 30.9% year-over-year. That's a meaningful demand signal for buyers evaluating this corridor.

Nomad Group refers to the NoMad/Flatiron corridor as "Unicorn Lane" — a concentration of venture-backed, high-growth companies that has driven sustained demand from well-capitalized tenants seeking long-term headquarters. For investors, that tenant profile translates directly to lease stability and lower rollover risk.

What Buyers Should Evaluate Before Purchasing Commercial Property in Midtown

Due Diligence Essentials

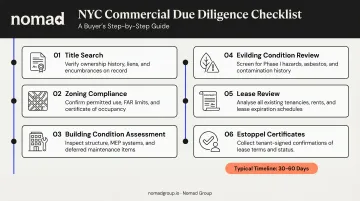

NYC commercial due diligence is more layered than most markets. A typical due diligence period runs 30 to 60 days, and buyers should plan for every layer:

- Title search — confirm clean ownership and identify any encumbrances

- Zoning compliance — especially critical for change-of-use scenarios; NYC's zoning code has meaningful complexity

- Building condition assessment — structural, mechanical, electrical, and envelope reviews

- Environmental review — Phase I at minimum, Phase II if contamination history exists

- Lease review — full rent roll, lease expiration schedules, rent escalation structures, and SNDA agreements

- Estoppel certificates — confirm tenant representations about lease status directly with occupants

SNDA (Subordination, Non-Disturbance, and Attornment) agreements are particularly important in leased acquisitions — they protect the tenant's lease position post-financing while recognizing lender rights. Missing this in due diligence creates risk at the financing stage.

Financial Underwriting

Core metrics every Midtown buyer must model:

- Cap rate and NOI — the basis for income valuation

- DSCR (Debt Service Coverage Ratio) — lenders typically require 1.20–1.25x minimum

- Projected IRR across realistic hold periods (5, 7, and 10 years)

- NYC Mortgage Recording Tax — budget 2.55% of the loan amount for mortgages of $500,000 or more. On a $10M mortgage, that's $255,000 — model it as a line item before running return scenarios.

Midtown pricing is deal-specific enough that broad cap rate averages have limited use. Anchor your underwriting to transaction comps — the $233–$526/SF range from Q4 2025 is a practical starting point.

Buying vs. Leasing Commercial Space in Midtown

The decision isn't universal — it depends heavily on your business stage and capital position.

The Case for Buying

Ownership makes the most financial sense when:

- Your space needs are stable and long-term (7+ year horizon)

- You can build equity rather than paying rent into a landlord's balance sheet

- Excess floors can be subleased to generate offsetting income

- Your balance sheet benefits from owning a real asset

Current conditions add a timing dimension. Distressed sale pricing has reset acquisition basis on certain assets, and locking in cost certainty through ownership becomes a genuine advantage — Midtown's long-cycle appreciation history has consistently rewarded patient, well-capitalized buyers.

The Case for Leasing

Leasing remains dominant for most Midtown occupiers — and for good reason. Full-year 2024 Manhattan leasing of 33.34 million square feet confirms that most companies are still solving their space needs through tenancy, not ownership.

Leasing wins when:

- Capital is better deployed into core business growth

- Headcount projections are uncertain (scaling up or down)

- Maintenance and capital expenditure risk should stay with the landlord

- Flexibility at lease expiration matters more than equity accumulation

For high-growth companies navigating these decisions, working with a tenant representation specialist — like Nomad Group — ensures lease terms are structured around your growth trajectory, not just today's headcount.

Middle-Ground Structures

Two hybrid options sit between full ownership and a standard lease:

- Sale-leaseback: A company sells its building and leases it back, monetizing real estate equity while retaining operational control of the space

- Office condos: A lower-entry ownership option that avoids full building exposure and suits companies wanting some equity upside without a large capital commitment

Both structures require careful modeling against current financing costs. Interest rates directly affect whether buying outperforms leasing over your target hold period — so run the numbers before committing.

How to Navigate the Midtown Commercial Market Successfully

Understand Where Deals Actually Happen

A significant share of Midtown commercial transactions never reach public listing platforms. They move through broker relationships, direct outreach to building owners, and private networks. Buyers who rely exclusively on marketed listings are working with an incomplete picture of the opportunity set.

The practical implication: your advisor's relationships matter as much as their market knowledge.

Engage a Full-Service Partner Early

The most successful Midtown buyers engage advisors before they've identified a specific property — not after. Early engagement means you can access off-market conversations, model multiple scenarios before committing, and enter negotiations with a clear basis and underwriting framework.

For companies planning to occupy their Midtown space, this is where a firm like Nomad Group adds a layer most acquisition advisors can't: once you've secured the lease, their in-house team handles buildout (with a 90-day turnaround and 300+ completed buildouts) and ongoing facilities management. That continuity from lease signing to move-in removes the need to source and coordinate a separate construction team at a critical juncture.

The Acquisition Timeline

Understanding this timeline upfront helps you resource the process correctly and avoid being caught off-guard by stages that routinely extend deals:

- Market search and shortlisting — 4 to 8 weeks

- Letter of Intent (LOI) — typically non-binding, outlines key economic terms

- Negotiation and contract execution — 2 to 4 weeks

- Due diligence period — 30 to 60 days (title, zoning, engineering, lease review, financing)

- Financing commitment — parallel to due diligence, but can extend timeline

- Closing — NYC commercial closings typically run 60 to 120 days from signed contract, depending on financing complexity, title issues, and any zoning questions that surface

Complex acquisitions — distressed assets, change-of-use plays, or properties with multi-tenant leases requiring SNDA negotiations — tend toward the longer end of that range.

Frequently Asked Questions

What is the average price per square foot for commercial real estate in Midtown Manhattan?

Pricing varies significantly by asset class and submarket. Verified Q4 2025 transactions ranged from $233/SF (845 Third Avenue) to $526/SF (75 Rockefeller Plaza). Class A office asking rents run $84.98/SF, with Midtown South Class A averaging $105.64/SF. A single average doesn't capture the market's current dispersion — consult transaction comps and current broker data for the specific asset class you're evaluating.

Is it better to buy or lease commercial space in Midtown NYC?

It depends on your growth stage, capital position, and certainty around long-term space needs. Established companies with stable headcount and 7+ year horizons typically benefit from ownership economics. High-growth companies prioritizing flexibility and capital efficiency are generally better served by leasing.

What types of commercial properties are available for sale in Midtown Manhattan?

The main categories include full office buildings, office condominiums (floor-by-floor strata ownership), ground-floor retail condos, mixed-use properties combining commercial and residential/hospitality income, development sites, and distressed or value-add assets from over-leveraged owners.

What should I look for when evaluating a commercial property purchase in Midtown?

Start with the fundamentals: submarket location, tenant quality and lease creditworthiness, building condition, and zoning compliance (especially for change-of-use scenarios). On the financial side, focus on:

- Cap rate and NOI as your primary underwriting anchors

- NYC's mortgage recording tax, which must be modeled as a closing cost

- Current broker comps to validate your per-SF assumptions

How long does it take to close on a commercial property in New York City?

NYC commercial closings typically run 60 to 120 days from signed purchase contract. The due diligence period alone is usually 30 to 60 days. Financing complexity, title issues, and any zoning complications are the most common factors that push timelines toward the longer end.

Are there off-market commercial properties available in Midtown?

Yes — a meaningful share of Midtown commercial transactions occur entirely off-market, through broker relationships and direct owner outreach. Public listing platforms show only part of what's available. Working with a well-connected local advisor is the primary way buyers access deal flow that never reaches CoStar or LoopNet. Nomad Group's deep relationships across Manhattan's core neighborhoods give clients visibility into opportunities that aren't publicly listed.