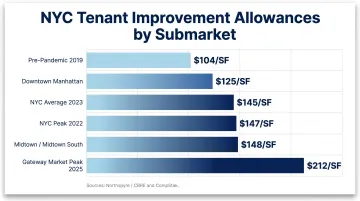

The stakes are high: NYC office tenant improvement allowances averaged $145/SF in 2023, up from $104/SF pre-pandemic (Northspyre). That's an extra $200,000+ in buildout funds for a typical 5,000-square-foot office. Yet many tenants leave money on the table because they don't know how to negotiate, what qualifies, or how the math works when construction costs exceed the allowance.

This guide breaks down what tenant improvements are, how allowances work, who pays (and in what scenarios), how to negotiate a better deal, and what the tax and ownership implications mean for your business.

TLDR:

- Tenant improvements are permanent modifications to leased space (walls, flooring, HVAC) funded partially or fully by the landlord

- NYC TI allowances averaged $145/SF in 2023; gateway markets hit $212/SF in 2025

- Ownership typically reverts to the landlord at lease end, regardless of who paid

- Longer lease terms and stronger creditworthiness unlock higher allowances

- Cash TI allowances trigger immediate taxable income for tenants; QIP depreciation is 15 years with 100% bonus depreciation for property acquired after January 19, 2025

What Are Tenant Improvements?

Tenant improvements (TI) — also called leasehold improvements or build-outs — are modifications made to a commercial space to configure it for a tenant's specific operational needs. Unlike a residential lease where you move into a turnkey unit, commercial tenants typically sign for raw or partially finished space and customize it to match their business requirements.

NAIOP defines this through the "Work Letter" concept: a legal document outlining the landlord's obligations relative to improvements necessary to prepare the premises for occupancy. In a "turnkey" arrangement, the landlord delivers the space ready for the tenant's stipulated use — walls built, lights installed, flooring laid.

These improvements become part of the building's permanent structure and stay in place for the full lease term. The key distinction: TIs fund a specific tenant's buildout, while building improvements — lobby renovations, elevator upgrades — benefit all tenants and are paid for solely by the landlord.

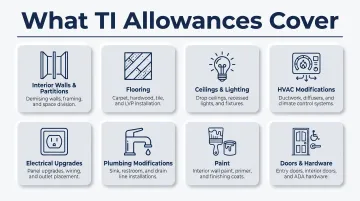

What TI Typically Covers

Tenant improvement allowances fund permanent or semi-permanent changes to the space. According to Cushman & Wakefield, TIAs typically cover:

- Interior walls and partitions (demising walls, glass-front offices, conference rooms)

- Flooring (carpet tile, hardwood, polished concrete, tile in pantries)

- Ceilings and lighting (dropped ceilings, LED fixtures, track lighting)

- HVAC modifications (zoning, ductwork, supplemental systems)

- Electrical upgrades (outlets, wiring for workstations, server rooms)

- Plumbing modifications (wet pantries, additional restrooms)

- Interior and exterior paint

- Doors and hardware (entry systems, interior doors, ADA-compliant fixtures)

What ties these together: each item is a capital improvement that stays with the building — which is exactly where landlords draw the line on what they'll fund.

What TI Does NOT Cover

Landlords draw the line at removable items that don't add lasting value to the building. Explicitly excluded from TI allowances:

- Furniture, fixtures, and equipment (FF&E) not permanently attached

- Desks, chairs, shelving, and storage systems

- Internet/data cabling and telecom equipment

- Decorations, artwork, and signage

- Kitchen appliances and break room furnishings

- Moving expenses and relocation costs

- Outdoor upgrades (rooftop improvements, exterior signage)

Investopedia notes that building-wide systems — elevators, roofs, fire protection, alarm and security infrastructure — are also excluded, since they represent capital expenses that benefit every tenant in the building, not just yours. Understanding where that line falls is the first step to negotiating a TI allowance that actually covers your buildout.

How Does a Tenant Improvement Allowance Work?

A Tenant Improvement Allowance (TIA) is a pre-negotiated sum the landlord agrees to contribute toward buildout costs. The allowance is almost always expressed on a per-square-foot basis — for example, "$80 per square foot" — making it easy to calculate total funding based on the size of your leased space.

NYC Market Context: What to Expect

NYC TI allowances vary significantly by submarket, building class, and lease term:

| Location/Metric | TIA Per SF | Source |

|---|---|---|

| NYC average (2023) | $145/SF | Northspyre/CBRE |

| NYC peak (2022) | $147/SF | Northspyre/CBRE |

| Pre-pandemic baseline (2019) | $104/SF | Northspyre/CBRE |

| Midtown/Midtown South | $148/SF | Northspyre/CBRE |

| Downtown Manhattan | $125/SF | Northspyre/CBRE |

| Gateway market peak (2025) | $212/SF | Bisnow/CompStak |

TI allowances in NYC have increased 112% since 2016 (Savills x CompStak). However, the same research warns that "TIAs have not kept pace with surging construction costs" and "the gap is now wider than ever," worsened by new tariffs pushing material costs higher.

For a 5,000 SF office in Midtown, a $148/SF allowance equals $740,000 in landlord-funded improvements — but that may not cover the full buildout cost.

Nomad Group has completed 300+ tenant buildouts across NYC neighborhoods including NoMad, Flatiron, and SoHo. The team works with clients from day one to scope realistic buildout costs against the allowance negotiated in the lease — so you know exactly where you stand before a single wall goes up.

How TI Allowances Are Delivered

TIA funds typically flow to the buildout in one of two ways:

Landlord manages construction — The landlord hires contractors, oversees the work, and pays invoices directly. You approve plans and changes but don't handle procurement or payments. Simpler for the tenant, but expect less flexibility on design and contractor choice.

Tenant manages, landlord reimburses — You hire contractors, run the project, then submit invoices for reimbursement up to the allowance cap. More control over design and contractor selection, but you'll need upfront capital and the bandwidth to coordinate.

What Happens When Costs Exceed the Allowance

If construction costs exceed the negotiated TIA, the tenant covers the difference out of pocket. If you negotiated a $100/SF allowance but the buildout costs $125/SF, you're responsible for the extra $25/SF.

Conversely, if the buildout comes in under budget, the treatment of leftover funds depends entirely on lease language:

- Rent reduction — credit applied to future rent payments

- Cash back — landlord returns unused funds (rare)

- Forfeiture — unused funds revert to the landlord (most common)

This must be negotiated explicitly before signing. Don't assume leftover funds belong to you.

Who Pays for Tenant Improvements — and How?

In most commercial leases, the landlord pays via the TI allowance because it's in their interest to attract and retain quality tenants. A customized space makes tenants more likely to renew than relocate at lease end.

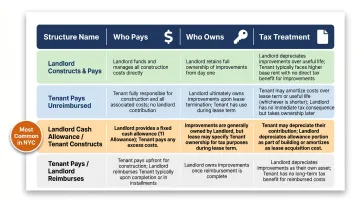

Four Payment and Ownership Scenarios

According to GBQ, four distinct structures create different tax and ownership outcomes:

| Structure | Who Pays | Who Owns | Tax Treatment |

|---|---|---|---|

| Landlord constructs and pays | Landlord | Landlord | Landlord depreciates; tenant has no tax impact |

| Tenant constructs and pays (unreimbursed) | Tenant | Tenant | Tenant owns and depreciates |

| Landlord provides cash allowance; tenant constructs | Tenant (funded by landlord) | Tenant | Cash is taxable income to tenant; tenant depreciates improvements |

| Tenant pays; landlord reimburses as rent substitute | Tenant (reimbursed) | Complex | Complex tax treatment; generally unfavorable |

The third structure — landlord cash allowance with tenant construction — is the most common in NYC office leasing. Tenants must recognize the cash allowance as taxable income immediately upon receipt, which can create a significant tax event in the year of lease commencement.

Who Owns the Improvements at Lease End?

In most commercial leases, tenant improvements legally revert to the landlord when the lease expires — even if the tenant paid for some or all of them.

Fox Rothschild confirms: improvements made under a TI allowance "will remain the property of the landlord after the lease expires."

However, many leases require the tenant to restore the space to its original condition at lease end, which can be costly. Troutman Pepper Locke documents the standard REBNY Form provision: all fixtures, partitions, and installations "become the property of the landlord and shall be surrendered with the leased premises" unless the landlord elects to have them removed at the tenant's expense.

Best practice: Negotiate restoration scope at lease signing to limit the obligation to specialty alterations only (internal staircases, raised flooring, supplemental HVAC) — not standard office finishes.

TI vs. Building Improvements

Tenant improvements benefit an individual tenant's buildout. Building improvements benefit all tenants and are funded solely by the landlord. As Investopedia puts it, building improvements "benefit everyone in the property and generally change the overall structure of the building itself."

Examples of building improvements landlords fund separately:

- Lobby renovations

- Elevator upgrades

- Roof replacement

- Fire protection and alarm systems

- HVAC systems serving the entire building

Knowing the difference protects you at the negotiating table — don't accept building-wide capital costs as items the landlord will deduct from your TI allowance.

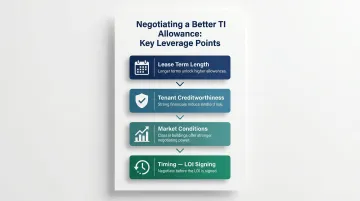

How to Negotiate a Better TI Allowance

Tenant improvement allowances are negotiable — and knowing the leverage points can unlock tens of thousands of dollars in additional funding.

Key Leverage Points

Lease Term Length Post-2020, higher TIAs have become "more strongly tied to longer lease terms," according to Savills x CompStak. Landlords require longer commitments to offset the upfront capital they invest in buildouts. A 7-year lease will command a higher TI allowance than a 3-year lease.

Tenant Creditworthiness Strong financials signal to landlords that you'll fulfill the lease term, reducing their risk. Well-funded companies or those with institutional backing typically secure higher allowances because landlords are confident in their ability to pay rent for the full term.

Market Conditions Tenant-favorable markets force landlords to compete aggressively to fill space. The current market (2025) is bifurcating: trophy asset landlords are regaining leverage while lower-tier buildings face mounting challenges and may need higher TIAs to stay competitive. If you're considering a Class B building, you have stronger negotiating power.

Timing The best time to negotiate TI terms is before the Letter of Intent (LOI) is signed. Once you've committed to a deal framework, your leverage drops. Come to the table with a detailed, itemized construction budget so your ask is grounded in real numbers, not guesswork.

The Rent vs. TI Tradeoff

Landlords sometimes offer tenants a choice: a larger TI allowance or lower base rent. How do you evaluate this?

A higher TI allowance gives you upfront capital for buildout but locks in elevated rent for the life of the lease. It's the right call if you need extensive customization, have limited cash reserves, or are confident you'll stay for the full term.

Lower base rent, on the other hand, preserves monthly cash flow — a better fit for startups with minimal buildout needs or companies that prioritize flexibility over upfront capital.

If you're Series A or earlier and every dollar of runway counts, lean toward lower rent. If you're post-Series B with a 50-person team that needs a purpose-built space, take the TIA.

Work With an Experienced Tenant Rep Broker

The most direct way to secure a better TI package is working with a broker who knows what landlords in specific submarkets are offering and can benchmark your allowance against comparable deals.

Nomad Group's team has negotiated leases across 2M+ square feet in NYC and knows which landlords in NoMad, Flatiron, and SoHo are offering competitive TIAs, what concessions are standard, and how to advocate exclusively for the tenant's interests throughout the process.

Tax and Ownership Implications of Tenant Improvements

Most NYC office tenants are caught off guard by one fact: receiving a cash TI allowance from your landlord counts as taxable income. How you structure the arrangement — and what you build — determines your tax exposure on both sides of the deal.

Qualified Improvement Property (QIP)

IRS Publication 946 defines QIP as "any improvement to an interior portion of a building that is nonresidential real property if the improvement is placed in service after the date the building was first placed in service."

Exclusions: Building enlargements, elevators/escalators, and internal structural framework.

Depreciation: QIP has a 15-year recovery period under the General Depreciation System (GDS) and 20 years under the Alternative Depreciation System (ADS).

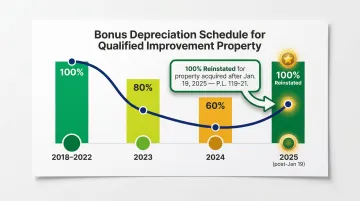

100% Bonus Depreciation Reinstated

P.L. 119-21 reinstated 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025 (IRS Publication 946). This means office tenants placing improvements in service now can potentially deduct the full cost in year one — a significant tax planning opportunity.

Bonus Depreciation Schedule:

- 2018-2022: 100%

- 2023: 80%

- 2024: 60%

- 2025 (property acquired after Jan 19, 2025): 100% (reinstated)

Tenant-Side Tax Treatment

That depreciation benefit, however, comes after an initial tax hit. When a landlord provides a cash TI allowance and the tenant constructs the improvement, GBQ confirms: "the tenant has immediate income recognition upon cash receipt. The tenant may then depreciate the improvement."

The Section 110 exclusion — which allows some tenants to exclude construction allowances from gross income — applies only to retail tenants with short-term leases of 15 years or less (26 U.S.C. Section 110). Office tenants don't qualify and must recognize the full cash TIA as taxable income in the year received.

Landlord-Side Tax Treatment

When a landlord provides a cash TI allowance, the IRS treats it as a lease acquisition cost and amortized over the lease term. If the improvement is tenant-specific, the landlord can typically deduct the remaining basis upon lease termination.

Before signing: For NYC office leases — where TI packages on larger spaces can reach seven figures — the difference between a landlord-managed buildout and a cash allowance can mean a substantial taxable income event for the tenant in year one. A CPA familiar with commercial real estate should review the structure before the lease is executed, not after.

Frequently Asked Questions

What is a typical tenant improvement allowance for commercial leases?

NYC office TI allowances averaged $145/SF in 2023 — Midtown and Midtown South at $148/SF, Downtown at $125/SF (Northspyre/CBRE). Gateway markets reached $212/SF in 2025. Longer lease terms and stronger tenant creditworthiness typically unlock higher per-square-foot allowances.

How do I negotiate a tenant improvement allowance, and is it worth trading higher rent for more improvements?

Negotiate before signing the LOI, using a detailed construction budget as leverage. The rent-vs.-TI tradeoff depends on your cash position and lease commitment: higher TI makes sense if you need extensive buildout and plan to stay long-term; lower rent benefits cash-strapped startups with minimal buildout needs.

Do tenants have to pay back a tenant improvement allowance?

TI allowances generally do not need to be repaid. Break the lease early, though, and the agreement may require repayment of a prorated portion as a termination penalty. That amount is typically calculated on a straight-line amortization basis from lease commencement.

Who owns tenant improvements and who is responsible for paying for them?

Ownership typically reverts to the landlord at lease end, regardless of who paid. However, many leases require the tenant to restore the space to its original condition — a potentially costly obligation. Review and negotiate restoration clauses before signing to limit exposure to specialty alterations only.

What is a TI package in construction?

A TI package refers to the complete scope of work funded by the tenant improvement allowance, including construction plans, specifications, and budget. It defines exactly what modifications will be made to the leased space and serves as the contract between landlord, tenant, and contractor.

What are qualified tenant improvements?

"Qualified Improvement Property" (QIP) under IRS rules covers interior improvements made to a nonresidential building after it was placed in service. Eligible improvements qualify for a 15-year depreciation period and may be eligible for bonus depreciation. A tax advisor can confirm whether your specific buildout costs qualify and which depreciation method applies.