This scenario plays out more often than it should. The culprit isn't usually negligence — it's a fundamental misunderstanding of how tenant improvements and betterments (TIBs) work, who owns them, who's responsible for insuring them, and what actually happens when they're damaged. Before you sign a lease or break ground on a buildout, understanding these dynamics can save you from six-figure surprises.

Key Takeaways

- TIBs are permanent upgrades you pay for that legally become part of the building, and typically the landlord's property

- Insurance pays TIB claims differently than furniture: without repairs, you recover only a fraction based on remaining lease time

- Lease language determines who insures and repairs TIBs; the landlord's policy doesn't automatically protect your investment

- 79% of commercial properties are underinsured, often because tenants exclude TIB values from coverage limits

- Reviewing lease terms and coordinating insurance before buildout prevents costly gaps

What Are Tenant Improvements and Betterments?

TIBs are fixtures, alterations, installations, or additions a tenant makes to a space they occupy but don't own, at their own expense. Because they can't be legally removed when the lease ends, they become part of the real property — and in most cases, the property of the building owner.

Common NYC office TIB examples:

- Glass partition walls and conference room enclosures

- Custom reception desks built into the space

- Upgraded electrical systems and server room infrastructure

- Plumbing additions (wet pantries, espresso bars)

- Specialty lighting fixtures and controls

- Branded interior finishes and millwork

- Built-in cabinetry and shelving

The line between TIBs and non-TIBs comes down to permanence. Items you can pack up and take with you don't qualify:

- Portable furniture and desks

- Movable shelving units

- Laptop stands and monitors

- Artwork and decorative items

The "Use Interest" Concept

While TIBs legally belong to the landlord once installed, the tenant holds a "use interest" — the right to use those improvements for the duration of the lease. This use interest creates the tenant's insurable interest and is why including TIB value in your own property coverage matters, even though you don't technically own the improvements.

TIAs vs. Tenant-Funded Improvements

A Tenant Improvement Allowance (TIA) is money the landlord provides to fund buildout costs. Manhattan TIAs averaged $118.65 per square foot in Q1 2025 for new deals and expansions, down from $138.65/SF in 2024. Improvements funded entirely by the landlord through a TIA may not qualify as your TIBs for insurance purposes. When you contribute funds above the TIA, those additional costs typically are TIBs — and that distinction directly affects your coverage.

Getting this classification right from the start matters. Nomad Group has structured buildout costs across 300+ NYC tenant buildouts, and proper TIB documentation consistently prevents coverage gaps when tenants need it most.

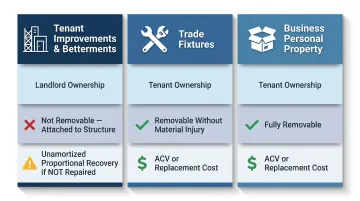

TIBs vs. Trade Fixtures vs. Business Personal Property: What's the Difference?

These three categories are often confused, but insurance treats each one differently — especially when it comes to claim payouts.

| Category | Ownership | Removable? | Valuation If Not Repaired |

|---|---|---|---|

| TIBs | Landlord (tenant has use interest) | No | Unamortized proportional cost based on remaining lease term |

| Trade Fixtures | Tenant (if removable without material injury) | Yes | ACV or replacement cost under standard BPP terms |

| Business Personal Property | Tenant | Yes | ACV or replacement cost |

Trade Fixtures

Trade fixtures are items a tenant installs for business purposes that can be legally removed when the lease ends without causing material injury to the premises. Examples include retail display cases, certain branded kiosk structures, or specialized equipment mounted but not permanently affixed. These remain the tenant's property and are covered under business personal property insurance at actual cash value or replacement cost.

Business Personal Property (BPP)

Unlike trade fixtures, BPP covers movable items owned by the business outright: furniture, computers, equipment, inventory. It's covered under the tenant's policy and valued at replacement cost or actual cash value depending on the coverage selected.

Why TIB Valuation Works Differently

When TIBs are damaged and not repaired, insurance pays only a proportion of the original cost based on remaining lease term — not full replacement value. The calculation works like this:

(Original Cost × Days remaining in lease) / (Days from installation to lease expiration) = Recovery

Example: You install $500,000 of TIBs at the start of a 10-year lease. Five years later, they're damaged in a fire and not repaired. Your recovery comes to $250,000 — only half the original cost, reflecting the five years of use remaining. This is called the unamortized value.

If TIBs are repaired promptly, you recover actual cash value or replacement cost (if that coverage is active). If the landlord or another party repairs them, your policy pays nothing because you haven't suffered a financial loss.

Misclassifying TIBs as trade fixtures — or ignoring the category entirely — means recovering far less in a claim than you spent on the buildout.

How Lease Language Determines Your TIB Responsibilities

The lease — not the insurance policy — determines who owns improvements, who must replace damaged property, and who's obligated to obtain coverage. Review this language before signing.

Three Common Lease Scenarios

Scenario 1: The lease requires the tenant to insure TIBs and repair them after a loss. Your policy must cover them and your BPP limit must include their full value.

Scenario 2: The lease makes the landlord responsible for insuring and repairing TIBs. You may be able to remove them from your BPP limit using endorsement CP 14 20 — but verify this carefully with your broker.

Scenario 3: The lease is silent on the matter. This creates ambiguity and risk for both parties. Don't assume silence means the landlord covers it.

The Danger of Relying on Landlord Promises

Even when a lease places repair responsibility on the landlord, circumstances change. The landlord may go bankrupt, the building may be deemed too damaged to rebuild, or the landlord may exercise a termination clause after significant damage.

In any of those scenarios, you lose access to your TIBs entirely — even if those improvements were never physically damaged. Leasehold Interest Coverage (ISO form CP 00 60) addresses exactly this risk. It covers the unamortized portion of TIB investments when a lease is cancelled due to covered property damage, and it must be added separately — it's not included in standard property policies.

Restoration-to-Original-Condition Clauses

Many NYC commercial leases require tenants to remove improvements and restore the space to its original condition at lease end. Demolition costs in NYC typically range from $10 to $30 per square foot. A 10,000 SF office could face $100,000 or more in unexpected restoration costs.

These clauses are negotiable. Tenants can strike the clause, cap restoration costs, or obtain a waiver for landlord-pre-approved improvements. Nomad Group works with clients to address these clauses before signing, when negotiating leverage is at its peak — not after a buildout is already complete and options narrow.

Insurance Coverage Considerations for TIBs

TIBs Are Included in BPP by Default — But You Must Account for Their Value

TIBs are automatically included in most business personal property (BPP) insurance forms under ISO CP 00 10. No separate endorsement is required. But you must include the full value of the TIBs in your BPP limit to avoid a coinsurance penalty.

Coinsurance explained: If you're underinsured relative to the total value of your covered property, the insurer may only pay a proportional share of any claim — not the full loss amount. The standard formula:

(Amount of Insurance Carried / Amount of Insurance Required) × Amount of Loss = Recovery

If you carry only 50% of the required coverage, you recover only 50% of a loss — even if your policy limit is higher than the claim amount.

Landlord Insurance Exposure

TIBs are physically part of the building and technically fit the definition of "building" on the landlord's policy too. If a landlord doesn't increase their building coverage to reflect TIBs installed by tenants, they may face a coinsurance penalty — even if the lease makes the tenant responsible for insuring them.

The fix is straightforward: when the tenant covers TIBs, the landlord should use endorsement CP 14 20 to explicitly exclude TIBs from their building coverage. This step is frequently skipped during lease negotiations — and it's one of the most common sources of coverage disputes after a loss.

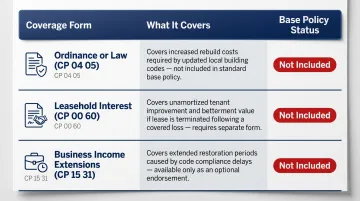

Additional Coverage Types to Discuss

Three additional coverage forms are worth discussing with your insurance advisor before finalizing your policy:

| Coverage Form | What It Covers | Included in Base Policy? |

|---|---|---|

| Ordinance or Law (CP 04 05) | Increased construction costs when rebuilding to updated building codes costs more than the original TIB value | No — optional endorsement |

| Leasehold Interest (CP 00 60) | Unamortized TIB value if the lease is terminated due to a covered loss, even when TIBs aren't directly damaged | No — separate coverage form |

| Business Income Extensions (CP 15 31) | Extended "period of restoration" when building code compliance delays TIB repairs | No — optional endorsement |

Common TIB Mistakes Tenants Make

Not Accounting for TIB Value When Setting Insurance Limits

Many tenants set BPP coverage based on furniture and equipment alone, completely ignoring buildout costs. If you spent $400,000 customizing an office in Flatiron, that value needs to be reflected in your coverage. According to Marsh's 2024 data, 79% of commercial properties are underinsured, covered for only 63% of required value on average.

Document all TIB costs at the time of buildout — contractor invoices, receipts, architect fees — and review coverage limits with your broker before construction begins.

Assuming the Landlord's Policy Covers Your Buildout

Landlord insurance covers the building structure and the landlord's interests — it does not protect your investment in improvements you paid for. First-time commercial tenants often learn this the hard way.

Even if the landlord's policy technically covers TIBs as part of the building, without explicit coordination and contractual language, you can't rely on it and may have no legal claim to the payout.

Failing to Revisit TIB Coverage as the Lease Progresses

Your financial exposure shifts as the lease term advances — the unamortized value of TIBs decreases over time, which affects how much coverage you actually need. Revisit your policy when you:

- Renew a lease (renewals often reset the TIB amortization clock)

- Expand your space

- Make additional improvements

- Change insurance carriers

Not Maintaining Documentation

In Bread & Butter v. Certain Underwriters at Lloyd's (2010), the NY Appellate Division held that the insured must prove TIBs were "made or acquired" at their expense. Without contractor invoices, lease documentation, and business asset purchase records, TIB claims may be denied. Keep organized records from day one.

Frequently Asked Questions

What are tenants' improvements and betterments?

TIBs are fixtures, alterations, or additions a tenant makes to rented space at their own expense that become a permanent part of the building and typically cannot be removed when the lease ends. They become the landlord's property in most cases.

What do tenants' improvements and betterments cover?

TIBs typically include built-in walls, upgraded flooring, custom lighting, plumbing or electrical additions, and any permanent structural changes a tenant funds. They exclude movable furniture, equipment, or any items the tenant can take at lease end.

Do commercial tenants need insurance?

Yes. Commercial tenants are typically required by their lease to carry property and liability insurance, and that coverage should include the value of any TIBs. The landlord's policy does not protect a tenant's personal property or buildout investments.

Does landlord insurance cover renovations?

Landlord insurance generally covers the building structure, not improvements funded by the tenant. Even though TIBs become part of the building, tenants shouldn't rely on the landlord's policy — they need their own coverage to protect that investment.

What does "walls in" mean in tenants' improvements and betterments?

"Walls in" (also called "studs in") means the tenant is responsible for everything inside their leased space — flooring, ceilings, interior walls, and any installed improvements. It marks the boundary where the landlord's coverage ends and the tenant's begins.

What is the 80% rule in property insurance?

The 80% coinsurance rule requires insuring property for at least 80% of its replacement value. If TIBs aren't factored in and coverage falls below that threshold, the insurer may only pay a proportional share of a claim rather than the full loss.