Introduction

When a high-growth tech startup signs its first real office lease in Manhattan, the negotiation spotlight often falls on the headline rent per square foot. But understanding leasehold improvements can matter just as much — what gets built, who funds it, and how it hits your books.

Research shows that Manhattan tenants receive an average of 24% of total rent value as concessions, with buildout allowances reaching up to $148/sf in neighborhoods like Midtown South. Misunderstanding these terms can cost companies six figures.

This guide covers:

- What leasehold improvements are and how to identify them

- Qualifying examples across common office buildout scenarios

- Who pays — and the landlord vs. tenant funding structures

- Accounting treatment under ASC 842

- What happens to improvements when the lease ends

Key Takeaways

- Leasehold improvements are permanent interior modifications made to suit a tenant's specific needs—like partition walls, flooring, or custom lighting

- Funding comes from landlords (TIA or turnkey), tenants, or a mix of both

- Under ASC 842, improvements are capitalized as PP&E and depreciated over the shorter of useful life or remaining lease term

- Improvements typically transfer to the landlord at lease end unless the lease specifies otherwise

- Negotiate the right terms upfront to protect capital during and after buildout

What Are Leasehold Improvements?

Leasehold improvements are any permanent alteration or addition made to the interior of a leased space to accommodate the specific requirements of a tenant. Also called tenant improvements (TIs) or build-outs, these modifications must meet three defining characteristics:

- Interior to the leased premises — changes made within the tenant's specific suite

- For the benefit of a specific tenant — customized to meet that occupant's operational needs

- Permanently affixed — attached to the building structure rather than movable

Leasehold improvements are reported as property, plant and equipment (PP&E) assets on the balance sheet and accounted for separately from the lease itself. They're most commonly associated with commercial real estate—office spaces, retail stores, restaurants—where tenants often inherit raw or semi-finished spaces that require customization before operations can begin.

Improvements can be commissioned before move-in or mid-lease, by either the landlord or the tenant, depending on what the lease agreement stipulates.

What Qualifies as a Leasehold Improvement?

Examples of qualified leasehold improvements include:

- Interior partition walls (glass-walled conference rooms, private offices)

- Flooring (carpet, hardwood, tile, raised flooring systems)

- Lighting fixtures and upgraded electrical systems within the suite

- Built-in shelving, cabinetry, and millwork

- Interior plumbing and kitchen/pantry installations

- Paint, drop ceilings, and acoustic treatments

- HVAC units serving only the tenant's space

The common thread across all of these: each modification permanently attaches to the building and serves only that specific tenant.

Key test: Does it affix to the structure and benefit this occupant alone? If yes, it qualifies. Movable furniture, freestanding equipment, and personal property do not.

What Does NOT Qualify as a Leasehold Improvement?

The following are classified as building improvements rather than leasehold improvements:

- Exterior improvements (landscaping, parking lots, roofing, facades)

- Building-wide systems (elevators, escalators, shared HVAC, fire suppression)

- Structural enlargements or additions to the building envelope

- Common area renovations (lobbies, hallways, shared restrooms)

- Window and door replacements on the building exterior

Under IRC Section 168(k)(3), Qualified Improvement Property (QIP) specifically excludes expenditures for building enlargement, elevators or escalators, and the internal structural framework. This distinction carries real consequences: building improvements follow different depreciation schedules than leasehold improvements, which affects both your tax position and balance sheet treatment.

Common Examples of Leasehold Improvements

Office-Specific Examples

For startups and high-growth companies in Manhattan neighborhoods like Flatiron, NoMad, and SoHo, typical leasehold improvements include:

- Glass-walled conference rooms and collaborative meeting spaces

- Acoustic panels and sound-masking systems for open-plan environments

- Custom reception areas with branded signage

- Upgraded electrical capacity for high-density tech infrastructure

- Mix of collaborative open zones alongside private enclosed offices

- Wet pantries with coffee bars and kitchen facilities

- Data cabling and network infrastructure

What NYC Buildouts Actually Cost

In competitive markets like NYC, a "vanilla box" space—bare concrete floors, exposed ceilings, basic utilities—almost always requires significant buildout before occupancy. For a 3,000 sq ft professional office in Manhattan, budgets typically range from $420,000 to $520,000, while a 6,000 sq ft tech office can require $1.2M to $1.5M.

These figures also shape how much tenant improvement allowance (TIA) is realistic to negotiate. Building class, neighborhood, and lease term all affect what a landlord will offer — which is why understanding your full buildout scope before entering negotiations matters as much as knowing the per-square-foot rate.

Who Pays for Leasehold Improvements?

Since improvements are permanently attached and typically become the landlord's property at lease end, landlords often fund some or all of the work as a leasing incentive, especially in competitive markets. However, tenants frequently pay a portion or all of the cost, particularly when the buildout is highly customized.

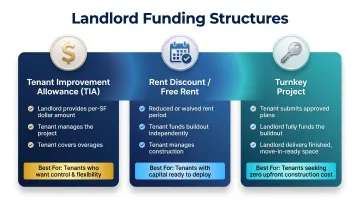

Tenant Improvement Allowance (TIA)

The most common funding method. The landlord offers a per-square-foot dollar amount that the tenant draws on to fund improvements, with the tenant overseeing and managing the project.

Formula: TIA = Allowance per Sq Ft × Leased Square Footage

Any costs exceeding the allowance become the tenant's responsibility.

NYC Market Benchmarks:

The average TIA in NYC was $145/sf in 2023, compared to $147/sf in 2022. Breakdown by submarket:

- Midtown: $148/sf

- Midtown South: $148/sf

- Downtown: $125/sf

Manhattan tenants receive an average of 24% of total rent as concessions (TIA plus free rent), with some submarkets offering up to 17 months of free rent alongside TIA concessions.

Other Funding Structures

Beyond the TIA, three other structures commonly appear in lease negotiations:

- Build-out allowance — The landlord packages a predefined set of improvements at a standard quality level and oversees the work. The tenant pays for any upgrades above that package.

- Rent discount — The landlord offers free or reduced rent for a set period, expecting the tenant to use the savings for improvements. The tenant manages the project independently.

- Turnkey project — The tenant submits detailed plans and a cost estimate; if approved, the landlord funds and delivers the finished space at move-in. This carries the lowest management burden for the tenant but may limit customization control.

How Are Leasehold Improvements Accounted For?

Leasehold improvements touch several areas of accounting — from how they're recorded on the balance sheet to how they're depreciated, taxed, and tested for impairment. Here's how each layer works.

Capitalization

Improvements exceeding the company's capitalization threshold whose useful life extends beyond one year are recorded as a fixed asset on the balance sheet under Property, Plant & Equipment (PP&E) rather than expensed immediately. Costs include direct materials, labor, and design fees.

Depreciation Under GAAP/ASC 842

Leasehold improvements are tangible assets (PP&E) and are depreciated over the shorter of the lease term or the improvement's useful life. Straight-line depreciation is the standard method — though another method (such as units-of-production) may apply if it better reflects how the asset is consumed.

Any change in depreciation period—such as early lease termination—is treated as a change in accounting estimate going forward.

TIA Accounting Treatment Under ASC 842

When a landlord provides a tenant improvement allowance, it is classified as a lease incentive that reduces the Right-of-Use (ROU) asset.

Example:

- ROU asset: $1,000,000

- TIA received: $100,000

- Adjusted ROU asset: $900,000

- Separate leasehold improvement asset recorded as PP&E: $100,000

Incentives paid at or before lease commencement are accounted for as a direct adjustment (reduction) to the ROU asset's opening balance per ASC 842-20-30-5. This differs from prior treatment under ASC 840, where TIAs were recorded as a separate liability.

Tax Treatment — Qualified Improvement Property (QIP)

Key tax provisions:

- Depreciable life: 15 years for QIP placed in service after December 31, 2017

- Bonus depreciation: The One Big Beautiful Bill Act (OBBBA), enacted July 4, 2025, permanently reinstated 100% bonus depreciation for qualified property acquired after January 19, 2025

- ADS election: If a taxpayer elects to be a real property trade or business, QIP is treated as 20-year ADS property and is not eligible for bonus depreciation

This IRS/tax treatment differs from GAAP depreciation — a tax advisor can help determine which provisions apply to your specific situation.

Beyond depreciation and tax treatment, leasehold improvements also carry impairment risk if circumstances change mid-lease.

Impairment

Leasehold improvements are long-lived assets within the scope of ASC 360-10 and are tested for impairment separately from lease term reassessments.

An impairment test is required when any of the following indicators arise:

- Early lease termination

- Significant shift in business strategy

- Physical damage to the improvements

If the carrying value exceeds the recoverable amount, an impairment loss must be recognized on the income statement.

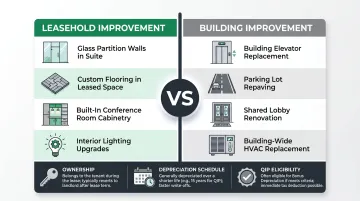

Leasehold Improvements vs. Building Improvements

Leasehold improvements benefit only one specific tenant's space — interior, attached, and suite-specific. Building improvements benefit the property as a whole or multiple tenants, affecting shared systems or the overall structure.

Contrast examples:

| Leasehold Improvement | Building Improvement |

|---|---|

| Installing glass partition walls in Suite 400 | Replacing the building's elevators |

| Custom flooring in your leased space | Repaving the parking lot |

| Built-in conference room cabinetry | Renovating the shared lobby |

| Interior lighting upgrades in your suite | Building-wide HVAC replacement |

The distinction matters for:

- Accounting and depreciation treatment

- Ownership at lease end

- Tax implications and QIP eligibility

Misclassifying a leasehold improvement as a building improvement — or vice versa — can trigger IRS scrutiny, skew your depreciation schedule, and create errors in financial statements that auditors will flag.

What Happens to Leasehold Improvements at Lease End?

Default Ownership Rule

In most commercial leases, improvements permanently attached to the space become the landlord's property when the lease expires. Per ISO CP 00 10, improvements and betterments "become part of the real property and, in most cases, are owned by the building owner." Landlords may repurpose or retain improvements for future tenants.

Restoration Clauses

Some leases include restoration clauses requiring tenants to return the space to its original condition, removing improvements at the tenant's expense. These obligations can run into $50,000 to $200,000+, especially for significant buildouts.

Before signing, clarify these terms:

- Clarify restoration obligations before signing

- Carve out exceptions for improvements that add long-term value (HVAC, flooring, lighting)

- Tie restoration obligations to landlord notice given well before lease end

- Get any agreements to leave improvements in writing

Renewal Influence

Restoration costs aren't the only financial lever at lease end — remaining improvement value shapes the renewal decision too. Improvements with significant useful life left create a real economic incentive to renew rather than relocate. Building out a new space from scratch runs $140 to $260/sf in Manhattan, which frequently outweighs the cost of negotiating renewal terms. Tracking the depreciated value of improvements gives finance teams a concrete basis for renewal vs. relocation decisions.

Frequently Asked Questions

What is a typical tenant improvement allowance?

TIA amounts are expressed on a per-square-foot basis and vary by market, building class, and lease length. In NYC, the average TIA was $145/sf in 2023, with Midtown and Midtown South averaging $148/sf. Allowances in competitive markets like Manhattan tend to run higher than national averages.

Who owns tenant improvements?

In most commercial leases, the landlord owns improvements at lease end since they are permanently affixed to the property. Lease terms may occasionally allow tenants to retain or remove certain improvements, and this should be specified in the lease agreement.

What is the difference between tenant improvement and building improvement?

Tenant improvements (leasehold improvements) are interior modifications that benefit only one specific tenant, while building improvements are changes to the overall structure or shared systems that benefit the property or all tenants.

What are examples of leasehold improvements?

Common examples include permanently affixed, interior modifications serving only that tenant:

- Interior partition walls and custom flooring

- Lighting upgrades and built-in cabinetry

- Interior plumbing within the suite

- Electrical system upgrades

What are considered qualified leasehold improvements?

For tax purposes, qualified improvement property (QIP) includes interior improvements to nonresidential buildings placed in service after the building was first put into use. Exterior work, elevators, escalators, building-wide HVAC, and structural enlargements do not qualify.

What is tenant improvement coverage?

Tenant improvement coverage refers to commercial property insurance that protects the value of improvements made to leased space. It can be carried by either the landlord or tenant depending on the lease. Coverage terms should be negotiated alongside the lease itself.