For high-growth companies, landlords, and investors, the stakes are real. The decisions being made right now about where and how to lease office space will influence talent, culture, and competitive positioning for years. This article breaks down the key trends defining NYC's commercial real estate market in 2026 and what they mean for companies planning their next move.

Key Takeaways

- Manhattan office availability has dropped from 19.5% in Q1 2024 to 14.6% in Q1 2026 — eight consecutive quarters of decline

- Trophy and Class A spaces are tightening fast; Class B/C buildings remain structurally challenged

- AI and tech firms now drive 22.1% of Manhattan's tech/media office requirements — the highest level in over a decade

- Expansion deals have surged to 18% of leasing activity in 2026, up from 11% in 2024 — companies are growing, not just renewing

- Office-to-residential conversions are shrinking lower-quality inventory, cutting tenant options across key submarkets

The "Flight to Quality" Is Defining the NYC Office Market

When tenants in Manhattan talk about upgrading their office space, they're not just chasing nicer finishes. They're making a calculated bet that the right physical environment attracts better talent, builds stronger culture, and signals credibility to clients and recruits alike.

That logic is showing up clearly in the data.

Trophy Space Is Running Out

According to Newmark's Q1 2026 Manhattan Office Report, Midtown trophy direct availability sits at just 3.4% — and has not recorded a single quarterly rise since Q1 2023. Avison Young confirms trophy availability volume fell 22% year-over-year to 16.9 MSF, while Class A availability dropped 18% YoY to 25.2 MSF.

Class B buildings tell a very different story. Vacancy in that tier remains elevated, with demand concentrated almost entirely in modern, amenitized assets.

That divide shows up directly in pricing. Newmark reports Manhattan's overall asking rent at $78.25/SF, while Cushman & Wakefield places Class A asking rents at $83.25/SF — up during Q1 2026 — and 9.3% above Q1 2020 levels for Midtown Class A specifically.

What This Means for Tenants

The best spaces are shrinking faster than they're being replaced. Companies that wait for "the right moment" risk finding that their preferred buildings no longer have viable options.

Nomad Group sees this pattern consistently across NoMad, Flatiron, and Union Square — the corridor the firm calls "Unicorn Lane." Companies that move decisively on high-quality buildings in this area tend to secure better terms and better spaces; those that delay face a narrowed field. For teams ready to commit, having tenant representation and in-house construction management under one roof compresses the time between signed lease and move-in day significantly.

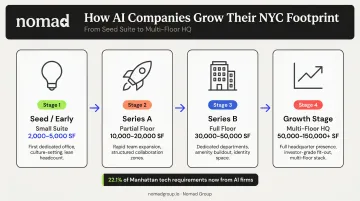

AI and Tech Companies Are Fueling the Strongest Demand in Over a Decade

The technology sector's rebound in Manhattan is moving faster than most market recoveries — and AI companies are driving most of the momentum.

The Numbers Behind the Surge

Newmark's Q1 2026 data puts total tech/media office requirements at 8.8 MSF — the highest level in more than ten years — with 22.1% of that demand coming specifically from AI firms. Harvey AI completed a 92,663 SF expansion in Midtown South. Anthropic is in the market for over 350,000 SF, according to Newmark. Cursor AI is searching for over 150,000 SF.

At 8.8 MSF, this is the kind of demand concentration that reshapes neighborhood availability — and it's already showing up in the data.

Where Demand Is Concentrating

Midtown South — encompassing NoMad, Flatiron, and SoHo — has become the epicenter of this activity. Newmark reports that Midtown South availability fell to 16.9%, its lowest level since Q4 2020, as AI and tech tenants cluster in these neighborhoods for talent density, transit access, and proximity to peer companies.

This is the same corridor where Nomad Group has focused its leasing activity for years. The firm has placed clients like Extend (NoMad), Authentic Insurance (Flatiron), and Nirvana (Union Square) — all companies that sought out exactly the kind of high-character, Class A environments that tech talent gravitates toward.

Why This Trend Has Staying Power

That tightening availability reflects something structural, not cyclical. AI company formation is accelerating, not plateauing. As firms move from seed to Series A to growth stage, their space needs evolve quickly — from a few thousand square feet to full-floor footprints. Each funding milestone tends to trigger a new space search, creating sustained, layered demand in NYC's innovation corridors.

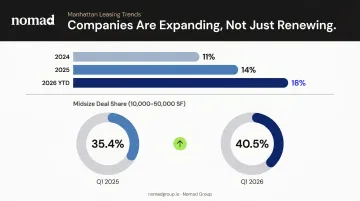

Tenants Are Expanding, Not Just Renewing

The clearest signal of market confidence right now: companies are no longer just protecting their existing footprints — they're actively growing them.

The Shift in Leasing Behavior

Avison Young's Q1 2026 analysis shows expansion activity reached 18% of Manhattan leasing in YTD 2026, up from 14% in 2025 and just 11% in 2024. That's a sustained, multi-year trend — not a one-quarter blip.

The midsize deal bracket is also expanding. Deals in the 10,000–50,000 SF range accounted for 40.5% of Q1 2026 Manhattan leasing, up from 35.4% a year earlier. This is the core range for high-growth companies scaling their teams from 50 to 200+ employees.

What It Signals

This pattern reflects genuine organizational confidence. Companies don't sign expansion deals when they're uncertain about the future.

Growth-stage firms across finance, technology, law, and media are committing to new and larger spaces — a sign they've settled on office as a competitive tool, not a cost to minimize.

Nomad Group's own client experience mirrors this. Flora (FloraFauna AI) doubled their office footprint within 30 days of their initial move-in. Authentic Insurance secured a full-floor space and was already working to bring a sister company into the building within one month of occupancy. For scaling companies making space decisions right now, these examples show how quickly growth can outpace an initial lease — and why building in flexibility from the start matters.

Office-to-Residential Conversions Are Tightening Office Supply

While tenant demand is strengthening, the supply of practical, usable office space is steadily shrinking — particularly at the lower end of the quality spectrum.

The Conversion Pipeline

Newmark reports that 16.7 MSF of Manhattan office space has either commenced conversion to residential use or is planning to do so, following 3.9 MSF already converted since 2020. CBRE notes that 60% of the current conversion slate is located in Midtown, with a median building age of 68 years.

Two policy mechanisms are accelerating this pipeline:

- City of Yes Housing Opportunity — expands non-residential conversions citywide and moves the eligibility date to buildings constructed before 1991

- AHCC / 467-m tax exemption — provides real property tax relief for conversions of non-residential buildings into eligible rental housing, for projects commencing by June 30, 2031

The Second-Order Effect for Tenants

As structurally obsolete Class B and C buildings exit the office supply pool permanently, tenants searching for quality space in desirable neighborhoods face fewer viable options. For companies running searches in submarkets like NoMad or Flatiron, the gap between "available" and "worth leasing" keeps widening. Knowing which buildings are 12 months from a conversion filing — versus which represent a stable, long-term home — is the difference between a lease that works and one that doesn't.

What's Driving These NYC Commercial Real Estate Trends

Three distinct forces are converging to shape NYC's commercial real estate market right now — and understanding each one clarifies where the market is heading.

Return-to-Office Has Matured

The debate about returning to physical offices is settled among growth-stage companies. Most have landed on hybrid or full-time in-person policies and are now designing their spaces around them. Office culture has become a recruiting and retention differentiator, particularly for AI and tech firms competing for engineering talent.

That shift in posture — from uncertainty to commitment — is translating directly into leasing activity.

Investment Confidence Is Returning

Manhattan investment sales reached their highest total since 2019 in 2025, according to BNP Paribas Real Estate. Q1 2026 saw notable transactions, including 65 East 55th Street selling for $730M ($1,327/SF) and a partial interest in 100 Park Avenue trading at $208.3M. Capital moving back into Manhattan assets typically signals — and accelerates — tenant confidence at the leasing level. When investors commit at that scale, it validates the market for occupiers too.

Policy Is Shaping Supply

NYC's M-CORE program (Manhattan Commercial Revitalization) supports renovation of aging commercial buildings south of 59th Street that are at least 250,000 SF and built before 2000. NYCIDA will consider applications covering up to 10M SF of eligible office space. This program is influencing which older buildings get upgraded versus converted, concentrating quality supply in specific corridors.

Future Signals to Watch

The market will keep moving. These are the forward indicators worth tracking over the next one to three years:

- Sublease absorption — Manhattan sublease space is down 50.7% from its Q1 2023 peak and now sits below Q4 2019 levels, signaling that excess supply is genuinely being absorbed

- AI/tech footprint expansion in Midtown South, particularly NoMad, Flatiron, and SoHo, as firms scale from early-stage to growth-stage space requirements

- Rent growth spreading from trophy assets into next-tier Class A buildings as top inventory tightens

- Increased competition for mid-block Class A space in established growth corridors, where the ratio of demand to viable supply is shifting

Taken together, these signals point in one direction: the leverage tenants held through 2022 and 2023 is eroding. The best buildings in NoMad, Flatiron, and SoHo have fewer available options today than they did 12 months ago, and landlord concession packages are tightening alongside them.

Nomad Group works with scaling companies navigating exactly this market — 2M+ square feet of NYC leasing experience across NoMad, Flatiron, SoHo, and Bryant Park, with in-house construction teams that can turn a signed lease into an operational office in 90 days. For companies with near-term growth plans, starting the search earlier leaves more options on the table.

Conclusion

Three takeaways define this market moment:

- NYC's office recovery is real and data-backed. Sustained leasing activity, shrinking availability, and genuine demand from AI, tech, finance, and legal tenants confirm this isn't a headline — it's a trend

- Strategy matters more than ever. The gap between trophy/Class A performance and Class B/C performance is wide and growing — building selection directly impacts outcomes

- Proactive companies win — the firms securing the best spaces on the best terms are moving with intention, not reacting to a tightening market after the fact

Available inventory in top Manhattan submarkets has already contracted meaningfully. Companies that understand where this market is heading — and act accordingly — will be better positioned than those waiting for conditions to stabilize further. In a market that has already moved significantly, waiting is its own risk.

For NYC companies navigating this environment, Nomad Group's tenant representation team helps high-growth companies move decisively — from identifying the right space to negotiating terms and delivering a built-out office, typically within 90 days.

Frequently Asked Questions

How is commercial real estate doing in New York City?

NYC's commercial real estate market is in a meaningful recovery. Manhattan office availability has dropped from 19.5% in Q1 2024 to 14.6% in Q1 2026, leasing activity is running well above historical averages, and strong demand from AI, tech, financial, and legal tenants is absorbing top-quality space at a consistent pace.

What is the 3 3 3 rule in real estate?

The 3 3 3 rule is an investment guideline for property owners: cover three years of mortgage payments from income, hold the property long enough to preserve its value, and don't sell before the three-year mark. It applies primarily to residential and investment property contexts, not commercial office leasing decisions.

What is driving office leasing demand in NYC right now?

The primary drivers are maturing return-to-office policies, the surge in AI and tech expansion, and renewed confidence from FIRE sector tenants — all fueling a broad shift from renewal-based to growth-driven leasing. Companies are treating physical office space as a competitive tool rather than an overhead line item.

Is now a good time to lease office space in New York City?

For companies with clear growth plans, moving sooner is advisable. Class A and trophy inventory is tightening fast — availability has declined for eight consecutive quarters, and competition in Midtown South is intensifying. Favorable terms are easier to secure before the market tightens further.

What neighborhoods in NYC are best for tech and AI company office space?

Midtown South neighborhoods — particularly NoMad, Flatiron, and SoHo — are the most sought-after for tech and AI tenants. These areas offer talent density, strong transit access, and a concentration of modern Class A inventory in buildings that support the engineering and product culture these companies depend on.

What is the difference between Class A and Class B office space in Manhattan?

Class A (and trophy) space features modern infrastructure, premium amenities, and prime locations — commanding higher rents than older, less well-appointed Class B buildings. Given the current flight to quality, the demand gap has grown substantially: Class A availability is falling while Class B vacancy remains elevated.