Introduction

Choosing the wrong office in New York City doesn't just waste money — it can stall a company's momentum at exactly the wrong moment. For scaling companies navigating that decision, the terminology matters: dedicated flexible office space refers to a fully private, lockable suite leased to a single company on shorter-term structures (typically 1–3 years), as distinct from open coworking environments where hot desks and shared memberships are the norm.

According to CBRE's 2025 Americas Office Occupier Sentiment Survey, 73% of tenants hit full capacity on peak days but carry only 34% average occupancy — meaning most companies are paying for significant unused space under lease structures that don't reflect how they actually work.

NYC's dedicated flex market is shifting fast. Lease terms are compressing, neighborhoods are diversifying, and the gap between premium private flex and commodity coworking is widening. Companies that understand these trends now will negotiate from a position of knowledge — not catch up after availability shrinks and asking rents climb.

Key Takeaways

- Demand for dedicated private flex offices is rising as companies prioritize privacy, identity, and culture over shared coworking.

- Lease terms have compressed to 1–3 years, with expansion options increasingly standard.

- NYC's dedicated flex market is seeing a "flight to quality" — well-designed, built-out spaces lease faster.

- Demand is spreading from Midtown into NoMad, Flatiron, SoHo, and Williamsburg, driven by tech and AI company growth.

- Elevated vacancy rates are giving tenants unusual leverage — a window that may narrow as the market recovers.

The Growing Preference for Dedicated Private Flex Over Open Coworking

Why Companies Are Leaving Shared Coworking Behind

Post-pandemic NYC has produced a clear pattern: companies that once parked 20–50 person teams in WeWork or similar environments are now actively seeking fully private suites on flexible terms. They want the shorter commitment of coworking without the cultural and operational compromises that come with shared space.

Companies transitioning out of coworking consistently cite the same friction points:

- Cultural dilution — building company identity in borrowed space is fundamentally difficult

- Brand disconnect — client meetings in generic conference rooms undermine positioning

- Hidden costs — meeting room fees, printing, and storage can add 30–40% to base membership costs

- Productivity friction — open coworking floors create constant interruptions that compound across teams

Authentic Insurance's experience is a concrete example. Tied to a costly mid-tier coworking commitment, they worked with Nomad Group to secure a full-floor, 5,500 sq ft dedicated space at 30 West 21st Street in Flatiron — delivered at 30% under comparable coworking costs, with room for 40+ desks and a clear expansion path.

Who's Driving Demand

Those friction points are pushing a distinct set of companies into the dedicated flex market. AI companies alone leased 486,000 SF in Manhattan through Q3 2025 — already surpassing the 414,000 SF leased across all of 2024. The majority of these deals involved short-term (2–3 year) structures with expansion clauses, and 54% targeted Class A buildings. Smaller AI firms are particularly active: one broker closed 10 AI tenant deals in summer 2025, most under 5,000 SF.

Beyond AI, the primary movers in dedicated flex deals include:

- Fintech and insurtech firms building regulated-environment headquarters (Authentic Insurance, Kaiko, Alternative Payments)

- SaaS and data companies requiring stable team environments for product development (deepIntent, Optimove, Zenlytic)

- Generative AI startups seeking identity-driven spaces that signal maturity to investors and clients (Flora/FloraFauna AI, Accrete, Fauna Robotics)

For Series A/B companies in these sectors, the move from shared coworking to dedicated flex isn't just an amenity upgrade — it's an operational and cultural signal.

Optimove's transition to a full-floor space at 1407 Broadway with a 3,000+ sq ft private rooftop terrace illustrates this directly: the rooftop became the center of company culture, and the dedicated environment gave the team something a hot desk arrangement simply cannot provide.

Shorter Lease Terms and Flexible Structures Are the New Normal

The New Lease Term Reality

Lease terms that historically ran 7–10 years in Manhattan are now commonly structured at 1–3 years for dedicated flex arrangements, with options to expand, contract, or exit built in from day one. CBRE data shows that average prime office lease terms between 2021 and 2024 ran 107 months for prime buildings and 86 months for non-prime — but AI firms and high-growth startups are actively targeting 2–3 year deals with expansion clauses, well below those averages.

Cushman & Wakefield's Q4 2025 Manhattan Office MarketBeat confirms the macro conditions enabling this shift:

| Submarket | Vacancy Rate (Q4 2025) |

|---|---|

| Manhattan Overall | 21.1% |

| Midtown | 20.0% |

| Midtown South | 23.9% |

| Downtown | 22.2% |

With Manhattan vacancy still at 21.1% — even after falling 90 basis points in Q4 2025 — landlords are more motivated than they've been in a decade to accept shorter initial terms in exchange for quality tenants. Tenant concessions averaged 26% of lease value in 2024, a 6.8% year-over-year increase, according to NAIOP.

The Trade-Off Companies Must Navigate

Shorter terms come with a real trade-off: the per-square-foot rate for a 2-year dedicated flex deal will typically exceed what a 7-year direct lease would command. For most high-growth companies, that premium is worth paying. The flexibility delivers concrete wins that a locked-in lease simply can't:

- Skips the 12–18 month construction timeline entirely

- Avoids long capital commitments before headcount visibility improves

- Preserves the ability to expand when a Series B closes

Nomad Group's advisory approach with scaling companies focuses on negotiating flexibility into lease terms from the outset: expansion rights tied to business milestones, right of first refusal on adjacent floors, and sublease provisions that provide downside protection. Getting those provisions in the initial lease is far easier in today's market than it will be in 12–18 months as conditions tighten.

The Flight to Quality — Premium Buildouts, Amenities, and Design

Why Generic Space Is Losing

NYC's return to office has not been a return to mediocrity. Companies and employees coming back three to four days a week are making deliberate choices about where they show up — and bare-bones, generic office space is losing those decisions.

The data reflects this clearly. Cushman & Wakefield reports that Class A new leasing in Manhattan reached 24.1 million SF in 2025 — the second-highest level in 30 years. In Midtown South specifically, Class A space accounted for 52% of total leasing in 2025, up from 36.8% in 2024. Meanwhile, Midtown Manhattan's prime vacancy rate has compressed to just 2.9%, meaning the very best product is nearly gone.

What High-Growth Companies Are Actually Requesting

Across Nomad Group's 300+ completed tenant buildouts, certain design priorities recur consistently:

- Natural light — consistently the first requirement, not a nice-to-have

- Branded environments — custom finishes, materials, and layouts that reinforce company identity

- Collaborative zones alongside focus areas — central open workstation areas balanced with private meeting rooms and phone booths

- Outdoor access — rooftop terraces and terraces have become genuine culture anchors (Optimove's 3,000+ sq ft private rooftop is the clearest example)

- High-end finishes — hardwood floors, glass-fronted offices, warm architectural detailing

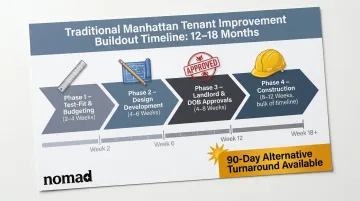

The Buildout Timeline Advantage

For high-growth companies, the operational advantage of a fast-turnaround dedicated flex space is substantial. A traditional tenant improvement buildout in Manhattan typically runs 12–18 months across four phases:

- Test-fit and budgeting — 2–4 weeks

- Design development — 4–6 weeks

- Landlord and DOB approvals — 4–8 weeks

- Construction — the bulk of the timeline

Nomad Group's 90-day buildout turnaround compresses that timeline significantly. The Extend AI buildout at 135 West 29th Street went from white-box to fully operational — including HVAC — in just five weeks. Extend subsequently raised a $17 million Series A shortly after moving in. Investors notice the office. A polished, purpose-built headquarters signals that a company is organized, funded, and ready to scale.

For companies evaluating dedicated flex options, operators who can deliver fast, high-quality buildouts create real value — not just in time saved, but in capital preserved and momentum maintained.

NYC Neighborhood Diversification in the Dedicated Flex Market

Beyond Midtown: Where Dedicated Flex Demand Is Growing

The historical default for NYC office demand — Midtown Manhattan, Plaza District, Hudson Yards — no longer reflects where high-growth companies are actually leasing. Demand has migrated south and east, and the data supports this shift.

The Flatiron NoMad Partnership reported a 27% year-over-year increase in leased office square footage in the corridor during Q3 2024, totaling more than 650,000 SF across 72 Class A and B leases. Nearly 60,000 office employees commuted into the Flatiron/NoMad district each weekday in September 2024 alone — 3.7 million employee visits for the quarter.

Nomad Group operates what they call "Unicorn Lane" — a corridor running through NoMad, Flatiron, and Union Square that has emerged as NYC's primary cluster for venture-backed tech and AI companies. Client placements across this corridor include:

- Extend AI — 3,500 sq ft at 135 West 29th Street (NoMad), full custom buildout in 5 weeks

- Authentic Insurance — 5,500 sq ft at 30 West 21st Street (Flatiron), full-floor headquarters

- Nirvana Health — dedicated space at 821 Broadway (Union Square), co-designed with in-house design team

Williamsburg is the other significant demand center. Flora/FloraFauna AI secured 5,000 sq ft at 300 Kent Avenue (The Refinery at Domino), a Class A waterfront building — and doubled their footprint within a month of moving in.

The borough's pull is straightforward: rents run roughly 40% below Manhattan Class A, the talent base lives nearby, and the industrial character of buildings like The Refinery simply cannot be replicated in a generic Midtown tower.

What Drives Neighborhood Selection

These placements illustrate a broader shift in how high-growth companies evaluate NoMad versus Hudson Yards versus Williamsburg. The criteria have changed:

- Where the team actually lives now outweighs where the firm's founders used to work

- Neighborhood character matters: AI and creative companies want spaces that reflect their identity, not a corporate tower lobby

- Multi-line subway access across boroughs often beats a prestigious address

- Outer-Midtown and Brooklyn submarkets offer meaningfully better economics — without sacrificing build quality

What's Driving NYC's Dedicated Flex Market Trends — And What to Expect Next

Structural Drivers: Hybrid Work and Funding Cycles

Hybrid work is not a transitional phase — it's the baseline. According to the Partnership for New York City's March 2025 survey, 57% of Manhattan office workers are at their workplace on an average weekday, representing 76% of pre-pandemic attendance. The breakdown matters:

- 30% work in-office 3 days per week

- 26% work in-office 4 days per week

- Only 10% are full-time, five-day in-office

This pattern drives companies toward dedicated spaces sized for realistic peak occupancy — not theoretical full-time headcount. A 40-person company with a three-day hybrid policy doesn't need 40 desks every day, but they do need a real, private, branded environment when people show up.

Funding cycles amplify this. NYC startups raised $2.1 billion in December 2025 alone — a 190% year-over-year increase — creating a consistent pipeline of post-raise companies that need their first real office. Dedicated flex structures align naturally with this moment: lower initial capital outlay, shorter commitment horizon, and enough flexibility to course-correct if headcount projections shift.

Future Signals: AI Demand and Market Bifurcation

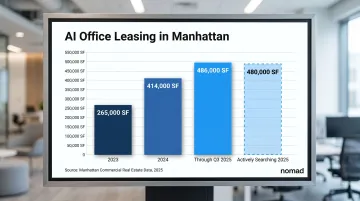

AI company leasing in Manhattan has followed a steep trajectory:

- 2023: 265,000 SF leased

- 2024: 414,000 SF leased

- Through Q3 2025: 486,000 SF leased, with an additional 480,000 SF actively searching

This demand is disproportionately concentrated in the NoMad/Flatiron corridor. AI One's 5,594 SF deal at 49 West 23rd Street in Flatiron in December 2025 is a representative example of where the sub-5,000 SF AI startup market is landing.

The flex market itself is bifurcating. JLL's April 2026 Flexible Office Space report identifies AI as a "powerful new driver of flex demand" specifically because ongoing workforce transformation makes long-term planning difficult — flex provides what JLL calls "real-time optionality."

Commodity coworking, meanwhile, is losing prestige and competing primarily on price. The gap between premium dedicated flex (private, managed, high-spec, shorter-term) and generic shared workspace is widening — and quality-focused companies are moving toward the former.

Flex by Nomad is built on in-house infrastructure and direct access across NYC's highest-demand neighborhoods — Flatiron, NoMad, SoHo, and beyond — structured to deliver private, managed office solutions without the overhead of commodity coworking.

The window for securing dedicated flex space at favorable terms will narrow. Manhattan's prime vacancy has already compressed to 2.9%, total 2025 leasing reached nearly 31 million SF (the highest since 2019), and net absorption turned positive at 7.6 million SF.

Companies that move now — while vacancy remains elevated in Midtown South and Downtown — will negotiate from a position of strength that won't last.

Frequently Asked Questions

What is the difference between a dedicated flexible office and a traditional coworking space in NYC?

A dedicated flexible office is a fully private, exclusive suite leased to one company — with lockable access, the ability to brand the environment, and a defined lease term. Traditional coworking involves shared space, shared amenities, and membership arrangements alongside other businesses.

What does a typical lease term look like for a dedicated flexible office in NYC today?

Current market conditions have pushed typical dedicated flex terms toward 1–3 years, down from the historical 5–10 year norm. Expansion options, right-of-first-refusal on adjacent space, and early exit clauses are increasingly standard — particularly in submarkets like Midtown South where vacancy remains elevated.

Which NYC neighborhoods have the strongest dedicated flexible office market right now?

The NoMad/Flatiron corridor and Union Square are the primary hotspots for high-growth company demand, alongside historically active Midtown and Grand Central submarkets. Williamsburg is emerging as a genuine alternative, particularly for tech and creative firms whose teams are based in Brooklyn.

Is a dedicated flexible office a good fit for a startup that just closed a Series A round?

Generally, yes. Post-Series A companies need a real office to build culture and attract talent, but a 7–10 year lease before headcount stabilizes is a real capital risk. Dedicated flex offers the private, branded environment a growing team needs without a commitment that could become a liability within 18 months.

How much more does a dedicated flexible office in NYC cost compared to a traditional long-term lease?

Dedicated flex carries a per-square-foot premium over traditional leases, reflecting shorter terms and managed services. Weigh that cost against avoided buildout capital, faster occupancy timelines, and the flexibility of not locking into a 10-year commitment.

How is NYC's return-to-office trend affecting demand for dedicated flexible offices?

NYC's return-to-office rate — at 76% of pre-pandemic levels versus a national average of roughly 55% — is directly fuelling demand for private dedicated space. Companies need functional, real offices for employees coming in three to four days per week, but the hybrid baseline means flexibility needs to be baked into the lease structure from the start.