This isn't a story of collapse or boom. It's a structural evolution. The companies tracking these shifts early are securing better spaces at better terms. Those moving slowly are finding their options narrowing.

Here's what's happening — and what it means for your business.

Key Takeaways

- Class A dominance: 87.9% of large Manhattan leases in Q4 2024 went to Class A or Trophy buildings

- Shrinking footprints: Average Manhattan new-lease size fell from 32,870 SF in 2019 to 27,932 SF in 2025

- Office-to-residential conversions are pulling older supply off the market, tightening affordable options quickly

- Investment sales have rebounded — Manhattan hit $3.2B in Q3 2024, more than double the year prior, signaling that pricing has likely bottomed

- Non-Midtown neighborhoods like NoMad, Flatiron, and Union Square are capturing the majority of high-growth company leasing activity

Trend 1: The Flight to Quality in NYC Office Leasing

The divide between good buildings and everything else has never been sharper.

According to Savills' Q4 2024 Manhattan office report, 87.9% of all Manhattan leases of 50,000 SF or more were signed in Class A or Trophy buildings. Meanwhile, Midtown Trophy availability sat at just 8.6% as of Q2 2024 — scarce by any measure. Class B/C availability, by contrast, stood at 21.8%, more than double the Trophy rate.

What This Looks Like on the Ground

The numbers aren't abstract. Bloomberg renewed 946,815 SF at 731 Lexington Avenue. Bain & Company signed for 235,201 SF at 22 Vanderbilt. These deals reflect a market where companies are actively trading up, not just renewing in place.

Class A+ buildings in Manhattan recorded 88% of their 2019 visitation rates in March 2025, compared to just 75% across the broader Manhattan average — employees follow quality spaces.

Older Class B stock tells the opposite story. Even at discounted rents, many buildings are struggling to attract tenants. Landlords in this segment are making lobby upgrades and offering substantial concessions just to stay competitive.

CoStar reported that high-end Manhattan landlords were giving away nearly a quarter of total rent as concessions — including 11.2 months of free rent and up to $150 PSF in tenant improvement allowances.

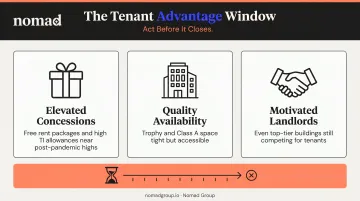

Why This Window Matters for Tenants

The current market offers something unusual: access to higher-quality spaces at more competitive effective rents than pre-pandemic. Concessions remain elevated, and landlords in quality buildings are still motivated to fill space — but that's changing fast.

Class A leasing reached 17.9M SF year-to-date through Q3 2025, the highest January-through-September volume in more than 30 years. Three conditions currently favor tenants — and all three are eroding:

- Elevated concessions: free rent packages and TI allowances remain near post-pandemic highs

- Quality availability: Trophy and Class A space is tight but not yet locked up

- Motivated landlords: even top-tier buildings are competing for tenants

As inventory tightens, this leverage won't last.

Nomad Group has seen this firsthand. Authentic Insurance moved from a costly coworking setup into a full-floor Flatiron office that delivered 30% under comparable coworking costs — with room to scale to 40+ desks. The upgrade wasn't just about prestige; it was about getting more for less while the opportunity existed.

Trend 2: The Flex Space and Hybrid Workspace Boom

Hybrid work didn't just change where people work. It changed how companies think about how much space they actually need.

Commercial Observer reported that the average Manhattan new-lease size fell from 32,870 SF in 2019 to 27,932 SF in 2025 — a roughly 15% compression driven by companies right-sizing for actual attendance patterns rather than maximum headcount.

How Companies Are Adapting

The shift shows up in what tenants are asking for:

- Shorter initial terms with contraction or expansion rights built in

- Fully fitted, plug-and-play suites that avoid lengthy buildout timelines

- Managed office products where facilities and operations are handled externally

- Modular configurations that accommodate hybrid schedules without wasted desk space

Traditional landlords have responded by launching their own flex suites. Coworking providers have continued expanding. The more substantive shift is the emergence of structured managed-office models — purpose-built for scaling companies that need control over their environment without absorbing the overhead of running it themselves.

Where Flex by Nomad Fits

Nomad Group's Flex by Nomad model was built for this moment. Rather than funneling clients into generic coworking memberships or long-term leases they'll outgrow, it delivers full-service office solutions built on in-house infrastructure — at a lower cost than conventional coworking operators, without the tradeoffs.

For high-growth companies, this matters practically: a Series A startup that doesn't know whether it'll have 20 or 60 people in two years shouldn't be locked into a 7-year lease for a space sized to the higher number. Flex formats keep capital deployable and headcount options open — both critical when the growth curve is still being written.

Trend 3: Office-to-Residential Conversions Are Reshaping Supply

The supply side of NYC's office market is changing in ways that many tenants haven't fully priced into their planning.

Bisnow reported that development sites and conversion buildings accounted for 42% of Q3 2024 NYC CRE transactions. This reflects just how much capital is flowing into repositioning older assets rather than leasing them.

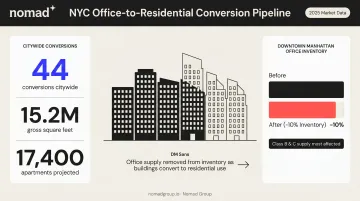

The Scale of the Pipeline

The NYC Comptroller's Q1 2025 data puts the pipeline in sharp relief:

- 44 completed, ongoing, or potential conversions identified citywide

- 15.2 million gross SF in total, expected to yield roughly 17,400 apartments

- 9.5M SF of Manhattan office space planned or in conversion as of Q2 2024 (Newmark)

- Downtown office inventory projected to shrink by 10% from conversions alone

That's a meaningful reduction in available supply — concentrated at the lower end of the quality spectrum, where Class B and C tenants have historically found their best value.

Policy Is Accelerating the Trend

NYC's 467-m and 485-x tax programs have made conversions more financially viable for developers. The 467-m program provides real property tax exemptions for conversions of non-residential buildings, while 485-x covers new multifamily development and eligible conversions — with benefit periods extending up to 40 years for qualifying projects.

The practical implication for tenants: Buildings that offered lower-cost alternatives in prior cycles are being pulled from office supply entirely. Companies waiting on affordable Class B options will find fewer of them as these incentives extend through multi-decade benefit periods.

Acting early on lease decisions is no longer a negotiating tactic — it's a supply reality.

Trend 4: CRE Investment Sales Are Rebounding as Values Stabilize

For the past two years, buyers and sellers couldn't agree on price. That standoff has largely broken.

Manhattan CRE investment sales reached $3.2 billion in Q3 2024 — more than double the volume of Q3 2023. Five-borough trades hit $4.9 billion in the same quarter, up 21% from the prior quarter. Individual transactions reinforced the trend: 590 Madison Avenue sold for $1.1 billion ($1,052 PSF), and 1177 Avenue of the Americas traded at $571.1 million in Q3 2025.

What This Means Beyond Investment

The capital markets recovery has direct implications for tenants:

- Improved landlord liquidity means landlords are more willing to fund tenant improvement allowances

- Price discovery means landlords have more clarity on asset values, reducing the stall tactics common when markets were frozen

- Lender activity is returning — CBRE noted that following the Fed's first rate cut of 2025, U.S. CRE investment volume is expected to grow roughly 15% for the year, revised up from an earlier 10% projection

Landlords who have successfully recapitalized or sold assets are now in a stronger position to offer competitive deal structures — larger TI packages, flexible lease terms, and faster execution. If you're negotiating a lease in one of Manhattan's core submarkets, the window to capitalize on motivated, well-positioned ownership is open right now.

Trend 5: Sub-Market Growth and the Rise of Non-Midtown Hubs

Midtown isn't disappearing. But it's no longer the only market driving leasing activity.

Cushman & Wakefield's Q3 2025 Manhattan report shows meaningful leasing concentration in non-Midtown neighborhoods, with Madison/Union Square and Greenwich/NoHo together accounting for 64.7% of Midtown South year-to-date leasing activity. Recent leases like The Farmer's Dog signing 58,800 SF at 568-578 Broadway in SoHo reflect sustained demand from consumer tech and creative companies in these neighborhoods.

That demand shows up in the rent and vacancy data too.

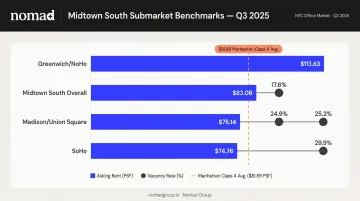

Submarket Rent Benchmarks (Q3 2025)

| Submarket | Asking Rent (PSF) | Vacancy |

|---|---|---|

| Greenwich/NoHo | $113.63 | 17.6% |

| Midtown South Overall | $83.06 | 24.9% |

| Madison/Union Square | $76.14 | 25.2% |

| SoHo | $74.76 | 29.9% |

Non-Midtown is not uniformly cheaper. Greenwich/NoHo asks above the Manhattan Class A average of $81.89 PSF. The right comparison is always building-specific, not submarket-level.

Why High-Growth Companies Are Choosing These Neighborhoods

Nomad Group refers to the NoMad-Flatiron-Union Square corridor as "Unicorn Lane" — and the tenant roster backs it up. Snappy, dbt Labs, Optimove, and deepIntent have all established offices here because the neighborhoods deliver:

- Proximity to tech and creative talent pipelines

- Walkable amenities that support in-office culture

- Building stock with character and collaborative layouts

- Competitive effective rents relative to Midtown trophy towers

What's Driving These NYC CRE Trends — and How They're Impacting Businesses

Three converging forces are shaping the NYC CRE market right now — and each one affects how tenants and landlords should be making decisions.

Macroeconomic and Lending Conditions

Interest rates have been the most direct lever on deal flow. The Fed's first rate cut of 2025 prompted CBRE to raise its U.S. CRE investment volume growth forecast to 15% for the year. In NYC, the data shows deal momentum had already begun recovering in 2024 — Manhattan investment sales more than doubled year-over-year before full rate normalization arrived.

Many transactions had been stalled by the bid-ask spread between buyers and overleveraged sellers — and as financing opens up and values stabilize, those deals are finally moving.

Demand Shifts from Hybrid Work

Office space has to justify its existence now. Companies aren't leasing for headcount capacity — they're leasing for collaboration, culture, and experiences that can't be replicated on a video call.

That's why average lease sizes are compressing while demand for quality is accelerating. Commodity space with nothing distinctive to offer sits vacant; well-located, amenity-rich buildings fill up.

Business Impact on Tenants and Landlords

Those demand shifts translate directly into negotiating dynamics — and right now, tenants have real leverage. But it won't last everywhere.

Key dynamics to understand:

- Concessions are still elevated — 11.2 months of free rent and up to $150 PSF in TI allowances were reported in high-end Manhattan buildings

- That leverage is narrowing as quality supply tightens and Class A absorption accelerates

- Landlords are investing in capital improvements to compete, which has long-term implications for operating costs and lease structures

- **Effective rent matters more than asking rent** — the spread between the two is currently significant, and negotiating it requires market knowledge

What to Watch Next: Future Signals in NYC Commercial Real Estate

The next one to three years will be defined by a few developments worth monitoring closely.

Watch for:

- The pace of conversion approvals — if the 467-m and 485-x pipelines accelerate, Class B availability could shrink faster than current forecasts suggest

- Class A vacancy compression — if it continues tightening while Class B widens, the two-tier market becomes permanent, not cyclical

- Interest rate movements — further cuts would unlock additional deal flow and capital availability, tightening the window for opportunistic tenants

Companies that act in the current window — when quality space is accessible and concessions are still on the table — will be better positioned than those waiting for the market to "normalize." History in NYC CRE suggests that window doesn't announce itself before it closes; vacancy tightens, asking rents firm up, and suddenly the leverage tenants had is gone.

Nomad Group has leased more than 2 million square feet across NYC's most active neighborhoods, guiding high-growth companies from initial search through lease execution and buildout. If you're making office decisions in the next 12 months, the advisors you engage now will determine what options you see, what terms you secure, and how fast you can move when the right space surfaces.

Frequently Asked Questions

What does CRE mean in real estate?

CRE stands for commercial real estate — income-producing properties used for business purposes, including office, retail, industrial, and multifamily buildings. It's distinct from residential real estate, which covers single-family homes and non-income-producing properties.

Is the NYC commercial real estate market recovering?

The market is in an active recovery phase. Investment sales volumes have risen sharply, quality office leasing is accelerating, and values have largely stabilized — though conditions vary significantly by asset class and submarket. Class A is tightening while Class B faces ongoing pressure.

What are the best neighborhoods for office space in NYC right now?

Flatiron, NoMad, Union Square, SoHo, and Williamsburg have become primary destinations for tech and high-growth companies, offering strong amenities and access to talent. Non-Midtown rents vary widely by building, so submarket comparisons alone don't tell the full story.

How is hybrid work affecting office space demand in New York City?

Hybrid work has reduced total square footage needs while raising the bar for space quality. Companies are upgrading rather than simply renewing — average new-lease sizes have fallen roughly 15% since 2019, while demand for amenity-rich, well-located buildings has intensified.

What is the difference between a traditional office lease and a flex office lease in NYC?

Traditional leases typically run 5–10 years and require significant tenant improvement negotiation on bare or vanilla space. Flex leases — like Nomad Group's Flex by Nomad model — offer shorter terms, fully fitted spaces, and all-inclusive pricing, letting companies scale without locking into more space than they need.