Introduction

Signing a commercial lease for the first time feels nothing like renting an apartment. The parties multiply — listing brokers, tenant reps, attorneys, landlords, managing agents — the terminology gets dense fast, and the financial stakes are orders of magnitude higher. A single lease decision can lock a company into six or seven figures of obligations for five years or longer — and many companies sign without fully understanding who's representing whom.

That's why understanding what a commercial real estate (CRE) broker actually does — and how they get paid — is the right place to start before touring a single space.

This guide covers the full picture: broker responsibilities across the deal lifecycle, the difference between tenant rep and landlord rep roles, how commissions work, and what to look for when choosing a broker in a market like NYC.

Whether you're a Series A startup preparing to leave coworking or an established company evaluating a renewal, knowing these fundamentals before you sit down at the negotiating table can mean the difference between a lease that fits your growth and one that constrains it.

Key Takeaways

- CRE brokers manage strategy, market research, negotiations, and execution — not just space tours

- Tenant rep and landlord rep brokers owe fiduciary duty to opposing sides — their interests don't align

- In both sales and leases, the property owner typically pays the commission; tenants rarely pay directly

- All commercial commissions are negotiable, with no standardized rates under antitrust law

- In NYC, neighborhood-level expertise matters; average asking rents vary significantly block by block

What Does a Commercial Real Estate Broker Actually Do?

Commercial brokerage and residential sales share a license category — and almost nothing else. Commercial transactions involve larger dollar amounts, longer timelines, more complex due diligence, and deep knowledge of multiple property types: office, industrial, retail, multifamily. The broker's role reflects that complexity.

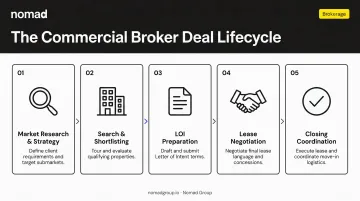

Core Responsibilities Across the Deal

That complexity plays out across every phase of a transaction. CBRE describes tenant representation as covering evaluation, planning, market research, financial analysis, document review, lease negotiation, move-in coordination, lease abstracts, and operating-expense review — the full lifecycle, not just a handshake at signing.

Here's what that looks like in practice:

- Market research and strategy — analyzing comparable transactions, building quality, and submarket conditions before a client tours anything

- Search and shortlisting — sourcing qualified listings, organizing tours, and helping clients compare options on cost, culture fit, and growth runway

- LOI preparation — drafting and submitting letters of intent, which NAIOP defines as the written agreement that comes before the formal lease

- Negotiation — structuring lease terms including rent escalations, free rent periods, tenant improvement (TI) allowances, renewal options, and co-tenancy protections

- Closing coordination — managing timelines, reviewing financial documents, and coordinating with inspectors and attorneys through signing

The Long-Term Advisory Role

The brokers worth working with don't disappear after the lease is signed. Good brokers provide ongoing market intelligence, advise on renewals 12–18 months before expiration, and help clients anticipate space needs as headcount grows. A broker who's already tracking your lease expiration and market conditions a year out gives you negotiating leverage that a reactive search never will.

Cresa recommends office tenants begin their search 12–24 months before lease expiration, and Colliers notes that complex requirements — those involving significant tenant improvements or ground-up work — can require 18–36 months of lead time.

A broker who's already tracking your situation well before the clock runs out delivers more value than one you call six months out.

Tenant Rep vs. Landlord Rep: Understanding Each Side

Every broker in a commercial transaction represents someone. Knowing who they represent — and what that means for you — is non-negotiable.

Tenant Representation

A tenant rep broker is hired exclusively to represent the company searching for space. Their fiduciary duty runs to the tenant: finding options that align with budget, culture, and growth trajectory, then negotiating terms that reduce risk and cost for the occupier.

That accountability covers the full cost picture — not just face rent, but:

- Free rent periods and concession structures

- Tenant improvement (TI) allowances

- Lease flexibility for expansion or early exit

JLL frames tenant representation as helping occupiers "explore and secure" spaces with a complete grasp of cost — a direct contrast to showing spaces without modeling the true financial exposure.

Landlord Representation

A listing broker is hired by the property owner to market the space, attract qualified tenants, and secure a lease at favorable terms for the landlord. Their fiduciary duty runs to the owner. This isn't a criticism — it's what they're hired to do. But tenants should never assume a listing broker is looking out for their interests.

Dual Agency: The Conflict Worth Understanding

Dual agency occurs when one broker represents both landlord and tenant in the same transaction. The NY Department of State is direct about this: a broker in a dual agency situation cannot provide undivided loyalty to both adverse parties. In New York, this arrangement requires informed consent from all principals — and commercial tenants should document that consent in writing.

In practice, a dual agent cannot fully advocate for your lease terms while also serving the landlord's interests. For growing companies, a dedicated tenant rep with no financial stake in any particular property gives you the cleaner — and less conflicted — outcome.

How Commercial Real Estate Brokers Get Paid

CRE brokers work almost entirely on commission. No deal, no fee. That creates strong incentive to close transactions — which is useful context for evaluating advice you receive during a search.

Commission Basics

Commercial commissions are calculated as a percentage of the total transaction value — either the sale price or the aggregate lease value. The most important thing to understand upfront: no standardized commission rate exists. The Massachusetts commercial antitrust guidance explicitly states that commercial real estate fees are not standard and are highly negotiable. Any broker quoting you a "standard" rate is oversimplifying.

This is grounded in federal antitrust law. Price-fixing among competitors — including agreements to set commission rates — is prohibited under the Sherman Antitrust Act.

Who Pays in a Sale

In most commercial property sales, the seller pays the full commission out of the proceeds at closing. That fee is then split between the listing broker (representing the seller) and the buyer's broker. The specific split depends on what's negotiated in the listing agreement — there's no universal standard.

The Broker-to-Agent Split

A portion of every commission an agent earns flows back to the brokerage firm. This internal split varies by firm, experience level, and production volume. Common structures include:

- Early-career agents: typically 50/50 splits with the firm

- High-producing agents: often negotiate 70/30 or better in their favor

- Top producers at some firms: may retain 80–90% depending on volume agreements

Every split is negotiated individually, so these figures shift based on the broker's track record and the firm's compensation model.

Flat Fee Arrangements

Some institutional or high-value transactions use flat fees rather than a percentage of deal value. This structure can make sense when total commission exposure on a large transaction would otherwise become disproportionate to the actual work involved. As a tenant or buyer, knowing this option exists gives you more room to negotiate — especially on transactions above $10M where percentage-based fees can climb quickly.

Commission Structures for Sales vs. Leases

Sales and lease commissions are calculated differently, and the distinction matters for anyone trying to understand what a broker actually earns on a transaction.

How Lease Commissions Work

Instead of a percentage of a purchase price, lease commissions are calculated against the aggregate value of the lease — total rent paid over the full term.

A basic example using the methodology from NAI Long Island's lease commission calculator:

- 5,000 sq ft at $70/sq ft/year = $350,000 annual rent

- Over a 5-year term: $350,000 × 5 = $1,750,000 aggregate lease value

- At a 4% negotiated rate: total commission = $70,000

The landlord typically pays this commission, which is then split between the listing broker and the tenant rep broker. Tenants don't usually pay the broker's fee directly — though the economics are embedded in the deal structure.

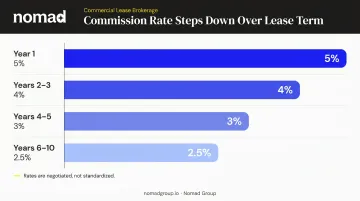

Tiered Commission Schedules

That 4% flat-rate example is a simplification. In practice, most lease commissions are tiered across the term — the rate steps down as the lease extends into later years.

One NYC brokerage publishes a representative schedule structured like this:

| Lease Year(s) | Commission Rate |

|---|---|

| Year 1 | 5% |

| Years 2–3 | 4% |

| Years 4–5 | 3% |

| Years 6–10 | 2.5% |

These figures are source-specific, not market standards. But the pattern holds broadly: later years and renewals are compensated at lower rates, reflecting the reduced search and negotiation work involved.

All of these figures are negotiated in the underlying brokerage agreement — not set by any industry rule.

What to Expect From Your Broker at Each Stage

Needs Assessment and Market Search

Before presenting a single option, a good broker spends time understanding the business: headcount today and projected, budget range, culture priorities, neighborhood preferences, and timeline.

In NYC, that groundwork matters more than in most markets. Average asking rents across Manhattan submarkets vary significantly — Midtown South ran $79.30/sq ft in Q4 2025 while certain Flatiron/Union Square Class A buildings approached $100/sq ft — and landlord quality and flexibility can shift block by block.

Nomad Group, which focuses on tenant representation for high-growth companies across Flatiron, NoMad, SoHo, and Williamsburg, structures early conversations around cultural priorities as much as physical requirements.

When the team worked with Authentic Insurance on their transition from coworking to a dedicated HQ, the focus wasn't just square footage — it was identifying a space that could signal quality and support team culture, ultimately landing a 5,500 sq ft full-floor office at 30 West 21st Street in Flatiron at 30% below comparable coworking costs.

Lease Negotiation and Execution

Once a space is identified, the broker leads LOI drafting, drives negotiation on key tenant protections, and coordinates closely with the client's attorney. The groundwork from the needs assessment — knowing the client's timeline pressure, budget ceiling, and growth plans — is exactly what creates leverage at this stage.

Key terms to push for include:

- Free rent periods — CBRE reported an average of 8.9 months free rent across 12 major U.S. markets including Manhattan in 2024

- TI allowances — averaging $87.51/sq ft across those same markets, with Class A Manhattan buildings running higher

- Renewal options — the right to extend at defined terms without re-entering the open market

- Expansion rights — rights of first refusal on adjacent space as headcount grows

Brokers who negotiate these provisions well can deliver savings that far exceed their commission cost.

Post-Lease Coordination

The broker's job doesn't end at lease signing. After execution, responsibilities typically include:

- Facilitating the handoff to construction and project management teams

- Advising on space planning and design alignment

- Supporting the client through move-in and early operations

For firms like Nomad Group — which has completed 300+ tenant buildouts with a 90-day turnaround target — brokerage and construction teams operate as one. When FloraFauna AI signed at 300 Kent Avenue in Williamsburg, project management and vendor coordination were looped in immediately. The company doubled their office footprint within 30 days of moving in — a result that depends on brokerage and construction sharing the same client context from day one.

How to Choose the Right Commercial Real Estate Broker

The commission rate matters less than most people think. A broker who secures an extra two months of free rent or a higher TI allowance often delivers more value than the entire commission cost — which the landlord is paying.

Evaluate brokers on:

- Submarket depth — neighborhood-level knowledge, not just city-wide familiarity. Manhattan's submarkets each move differently; a broker who can't distinguish NoMad from Midtown South isn't working at the level you need

- Tenant rep focus — a broker who primarily represents tenants has no incentive to steer you toward a particular landlord or building

- Transparency about compensation — can they explain exactly how they're paid and whether any conflicts exist?

- Track record in relevant deals — completed transactions with companies at your stage, in your target neighborhoods

- Relationship vs. volume orientation — brokers chasing transaction volume move fast and may not stay engaged through the hard parts of a negotiation

A few red flags to watch for: pressure to sign exclusivity agreements before they've demonstrated any market knowledge, vague answers about compensation, or an inability to articulate what makes your target submarket different from the ones next to it.

Frequently Asked Questions

What is a typical commission split (80/20) for commercial real estate brokers?

The 80/20 split refers to the agent-to-brokerage arrangement — the agent retains 80% and the firm takes 20%. Senior and high-producing agents typically see this structure; newer agents often start at 50/50, with splits improving as their volume grows.

Are 3% commission rates normal for commercial real estate brokers?

A 3% rate shows up in specific situations: for example, as one point on a tiered lease commission schedule covering years 4–5 of a multi-year office lease. For sales or full-service tenant representation on smaller or more complex deals, rates often run higher. All commercial commission rates are negotiable.

How much commission does a commercial real estate broker earn on a $300,000 sale?

At a negotiated 6% total commission on a $300,000 sale, the total fee equals $18,000. If split 50/50 between two brokerage firms, each receives approximately $9,000 before any internal agent-brokerage split is applied. These percentages are deal-specific, not industry standards.

What is the difference between a tenant rep broker and a landlord rep broker?

A tenant rep broker works exclusively for the company searching for space, owing fiduciary duty to the tenant. A landlord rep broker is hired by the property owner to market the space and secure favorable terms. These are opposing roles, and tenants benefit most from a broker whose sole job is advocating for them.

Who pays the commercial real estate broker's commission?

In both sales and lease transactions, the property owner — seller or landlord — typically pays the full commission out of transaction proceeds. Tenants and buyers generally don't pay directly, though the economics are built into the deal structure.

What should I look for when choosing a commercial real estate broker in NYC?

Prioritize neighborhood-level market knowledge, a dedicated focus on tenant representation, and a verifiable deal track record in your target submarket. In NYC, where vacancy and pricing shift block by block, submarket specialization and strong landlord relationships matter far more than city-level credentials.