Introduction

Sign a 10,000 SF office lease in Midtown South and the broker commission on that deal could quietly run $150,000 or more — paid entirely by the landlord, yet structured in ways that directly shape what you're offered and how hard anyone negotiates on your behalf.

Most tenants never see that number. Commercial broker commissions aren't disclosed in the lease, aren't regulated by New York statute, and aren't structured the same way twice. That information gap consistently costs tenants — whether it's accepting worse lease terms, skipping tenant representation, or not knowing when a broker's incentives diverge from your own.

This guide breaks down how commercial broker commissions work in NYC: how rates are set, who pays, how the money gets split, and what every tenant should know before signing.

Key Takeaways

- Commercial broker commissions in NYC typically range from 3% to 6% of total lease value, paid by the landlord

- Tenant rep brokers are almost always compensated by the landlord — signing with one costs you nothing

- Commission splits between listing and tenant brokers are usually 50/50, though this is negotiable

- Longer leases and larger spaces generate higher absolute commissions, which affects broker incentives

- An experienced tenant rep broker negotiates on your behalf, not the landlord's — that distinction matters

What Is a Commercial Lease Security Deposit?

A commercial lease security deposit is an upfront payment made by the tenant at lease commencement, held by the landlord as financial protection against unpaid rent, property damage, or other lease defaults. When the lease ends cleanly, the deposit is returned — less any legitimate deductions.

The rules governing commercial deposits differ sharply from what most tenants know through renting apartments.

How Commercial Differs from Residential

New York's residential deposit rules — including the one-month cap and 14-day return requirement — live in GOL Section 7-108, which applies exclusively to "dwelling units in residential premises." Commercial leases are not covered. As Akerman's commercial lease state comparison chart confirms, New York places no statutory limit on commercial deposit amounts and no specific statutory deadline for their return.

What New York does require, under GOL Section 7-103, is that deposit funds remain the tenant's property, be held in trust, and not be commingled with the landlord's own money. If the landlord holds the deposit in a bank account, the tenant must receive written notice of the bank's name and address.

The Dual Purpose of a Deposit

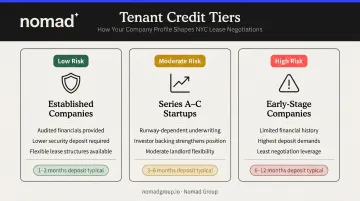

The deposit protects the landlord's financial exposure, but it also functions as a credit signal. For landlords evaluating tenants without long operating histories, the deposit amount is effectively their risk assessment in dollar form.

How much leverage a tenant has typically comes down to their track record:

- Established companies with audited financials and clean payment history can often negotiate lower deposits or alternative structures

- Series A–C funded startups may receive more flexibility if they can demonstrate runway and investor backing

- Early-stage companies with limited financials generally face the highest deposit demands and the least room to negotiate

What Determines How Much Security Deposit You'll Pay?

Commercial deposit amounts aren't standardized. They're the product of negotiation shaped by several factors — and understanding each one gives tenants real leverage before signing.

Tenant Creditworthiness

Landlords review financial statements, tax returns, and funding history to assess default risk. This is the single most influential factor in most deals.

According to Metro Manhattan's NYC office deposit guidance, deposits commonly range from 2 to 12 months depending on perceived financial risk. OfficeSublets is more specific: expect a minimum of 3 months for a direct NYC office lease, 6 months if you're a startup or have weak financials, and 8 to 12 months if no principal is willing to sign a good-guy guaranty.

VC funding doesn't automatically translate into landlord creditworthiness unless it shows up in financial statements. Landlords want to see runway, not a term sheet.

Lease Incentives (TI Allowances)

The more a landlord invests in your buildout, the more financial exposure they carry before you've paid a single month of rent. A substantial tenant improvement allowance — funding for construction, custom buildout, or space reconfiguration — often triggers a higher deposit demand.

Raw, unbuilt space leads to more TI negotiation and more deposit pressure as a result. Prebuilt or move-in-ready spaces can reduce both variables at once.

Market Conditions

Landlord leverage varies by submarket and building class. Two data points worth knowing:

- Manhattan-wide: Colliers reported Q1 2026 availability at 13.7%, with the strongest first-quarter leasing volume since 2014

- Midtown South (Flatiron, NoMad, SoHo): CBRE reported availability at 17.7% in Q1 2026, down significantly year over year

Higher submarket availability gives tenants more room to push back on deposit demands. Negotiate to local conditions, not citywide averages.

Nature of the Business

How a business uses space affects its risk profile. A software company with minimal physical footprint looks very different to a landlord than one requiring specialized buildout, heavy foot traffic, or complex mechanical infrastructure. Landlords factor in how difficult and expensive it would be to restore the space after a default.

This is where tenant representation pays off. Firms like Nomad Group, which specializes in NYC's high-growth office submarkets, benchmark deposit demands against comparable deals and structure terms that reflect the tenant's actual risk profile, not a landlord's opening position.

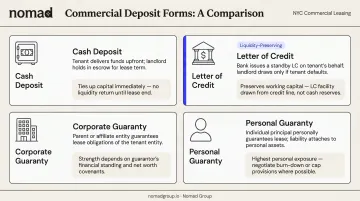

What Forms Can a Commercial Lease Security Deposit Take?

"Security deposit" doesn't always mean a wire transfer sitting in an escrow account. Tenants and landlords can agree on several structures, each with different implications for cash flow and risk.

| Form | How It Works | Key Consideration |

|---|---|---|

| Cash deposit | Lump sum held by landlord for lease term | Simple, but locks up working capital |

| Letter of credit (LOC) | Bank-issued instrument; landlord draws from issuing bank after default | Preserves cash; bank charges ~1% of face value annually |

| Corporate guaranty | Parent or related entity guarantees tenant's obligations | Shifts liability to another entity; scope matters |

| Personal guaranty | Founder or executive assumes personal liability | Highest personal risk; always negotiate a cap |

Cash vs. Letter of Credit

Cash deposits are universally accepted, but they tie up capital a scaling company could put to work elsewhere.

A standby letter of credit lets the tenant preserve liquidity. The bank funds any draw after a default, not the tenant. The tradeoffs:

- Requires a creditworthy banking relationship

- Must be renewed annually (failure to renew can trigger a landlord draw)

- Issuing banks typically charge around 1% of the face amount per year in fees

Guaranties and the "Good Guy" Clause

Personal guaranties carry serious financial exposure. A founder signing an unlimited personal guaranty on a 5-year lease with a large rent obligation is taking on real personal risk.

A "good guy" guaranty offers a middle ground: it limits the guarantor's liability to the period during which the tenant actually occupies the space. Once the tenant vacates and gives proper notice, the personal guaranty ends. NYC landlords accept these regularly, particularly for corporate tenants without an extended operating history. They can also be used to negotiate a lower cash deposit in exchange.

What Your Security Deposit Lease Clause Must Cover

Most deposit disputes trace back to a vague lease clause. A well-drafted clause gives you clear, enforceable protections. A vague one hands the landlord open-ended discretion — which rarely works in your favor.

Permissible Deduction Grounds

Push to define exactly what the landlord can draw from the deposit. Acceptable grounds typically include unpaid rent and documented damage beyond normal wear and tear. Resist broad language like "any amounts owed under the lease" — it creates an opening for disputed charges with no clear standard.

Return Timeline

New York has no statutory return deadline for commercial deposits. Market practice points to around 30 days — but that's industry guidance, not law.

Negotiate a specific number of days (21 to 60 is a reasonable range) and tie it to clear conditions: final inspection completed, written accounting of any deductions provided. Without a deadline in the lease, "reasonable time" can mean whatever the landlord decides.

Burn-Down Provisions

A burn-down clause allows the deposit to decrease over the lease term as the tenant demonstrates consistent performance. Common structures include:

- Time-based reductions — deposit steps down at year 2 or year 5

- Performance-based reductions — tied to net worth thresholds, EBITDA milestones, or funding events

- Default forfeiture — missing a burn-down trigger (such as a late payment) can forfeit that reduction

For startups that may have limited financials at signing but expect to grow, this is one of the most valuable provisions to negotiate.

Deposit Storage and Transfer

Two protections worth negotiating explicitly:

- No commingling — require the deposit be held in a separate, federally insured account, consistent with GOL Section 7-103's trust requirements

- Building sale transfer — under GOL Section 7-105, a landlord conveying the property must transfer the deposit to the successor and notify the tenant by registered or certified mail; make sure your lease mirrors this obligation so there's no ambiguity about who owes the refund

How to Protect Your Deposit — and Get It Back

Negotiating solid lease language matters — but so does how you execute at move-in and move-out. These steps cover both.

Document Everything at Move-In

Photograph or video every room, surface, and fixture before you occupy the space — and again at move-out. Date-stamped documentation is the most defensible evidence in a deposit dispute, particularly after buildout work when pre-construction condition can become contested.

Know the Wear and Tear Standard

Commercial leases typically require tenants to return the space in its original condition, minus normal wear and tear. Minor scuffs, routine cleaning needs, and standard aging aren't deductible. Damage caused by operations, modifications, or negligence is.

Know the line going in — and consider negotiating a specific wear-and-tear definition into the lease itself. Vague language almost always favors the landlord at move-out.

Schedule a Pre-Vacate Walkthrough

Request a joint walkthrough with the landlord before the lease ends. Any items flagged during that inspection can be addressed before final surrender — which costs less than losing deposit funds retroactively. Get every identified repair or deduction confirmed in writing.

If the Landlord Doesn't Return It

The escalation path:

- Written demand referencing the lease return deadline and GOL Section 7-103 trust obligations

- Formal demand letter from an attorney if no response within 5–10 business days

- Commercial Claims Court for amounts up to $10,000 — NYC Courts' Commercial Claims Part allows corporations, partnerships, and associations to sue without an attorney, subject to filing requirements

For larger amounts, claims for breach of contract or conversion (improper withholding) are the appropriate vehicle. Consult a commercial tenant attorney for disputes above small claims thresholds.

Frequently Asked Questions

Who pays the broker commission in a commercial lease?

In most NYC commercial transactions, the landlord pays the full commission — typically split between the listing broker and the tenant's broker. Tenants generally pay nothing out of pocket, which is why working with a dedicated tenant rep broker costs you nothing directly.

What is the standard commission rate for commercial real estate brokers in NYC?

NYC commercial broker commissions typically range from 3% to 6% of the total lease value, though the exact rate depends on lease size, term length, and deal complexity. Larger, longer-term leases often carry lower percentage rates negotiated between the brokers and landlord.

Can broker commissions be negotiated?

The commission rate is set between the landlord and the listing broker — tenants don't directly negotiate it. However, a skilled tenant rep broker can sometimes structure deals where concessions flow back to the tenant in other forms, such as free rent or a larger tenant improvement allowance.

How is the commission split between brokers?

When both sides have representation, the landlord's total commission is divided between the listing broker and the tenant's broker. The split varies by deal but is typically 50/50, though it can shift depending on which broker originated the deal or drove the negotiation.

When is the broker commission paid?

Commission is usually paid at lease execution, though some deals structure payment in two installments — part at signing and part at tenant occupancy. The timing is outlined in the listing agreement between the landlord and the listing broker.

Does using a tenant rep broker cost me anything?

No. Tenant representation is paid by the landlord through the commission already built into the deal. You get dedicated advocacy, market expertise, and full negotiating support — at no direct cost. Firms like Nomad Group work exclusively on the tenant side, meaning their interests stay fully aligned with yours throughout the process.