Introduction

Signing your first NYC commercial lease is a milestone. But buried in the paperwork is a clause that catches many founders off guard: the personal guarantee.

Landlords routinely ask a founder, CEO, or major shareholder to personally back the company's lease obligations. Sign the wrong version of this clause, and you're not just committing your company — you're putting your personal bank accounts, real estate holdings, and future income on the line.

Most tenants sign without fully understanding what they've agreed to. That's a real problem when a five-year lease in Flatiron or NoMad can represent millions of dollars in total obligations.

Here's what this guide covers:

- What a personal guarantor is and why landlords require one

- The types of guarantees you'll encounter in NYC leases

- The real financial risks involved

- How to negotiate better terms before you sign

TLDR

- A personal guarantor is an individual who pledges personal liability for a company's lease obligations if the business defaults.

- Landlords use personal guarantees as risk protection, especially for startups with limited credit history or no operating track record.

- Four main guarantee types exist: full/unlimited, limited/capped, burn-down, and the NYC-specific "good guy" clause.

- Signing without negotiating puts personal savings, property, and income at risk — not just business assets.

- Terms are negotiable. Caps, burn-down structures, letters of credit, and good guy clauses can all reduce personal exposure.

What Is a Personal Guarantor in a Commercial Lease?

A personal guarantor is an individual — typically a founder, CEO, or major shareholder — who signs the lease alongside the business entity and accepts personal liability for rent, damages, and other obligations if the company defaults.

The lease itself is signed by your LLC or corporation — but landlords often view that entity as insufficient protection, particularly for startups with no operating history or meaningful assets. A personal guarantee makes an individual directly responsible when the business can't cover its obligations.

What You're Actually on the Hook For

Most founders assume a personal guarantee covers missed rent. The reality is broader. Depending on how the guarantee is worded, a guarantor may be liable for:

- The full remaining rent balance for the entire lease term

- Unpaid operating expenses and real estate taxes

- Property damage costs beyond normal wear and tear

- Legal fees incurred by the landlord in pursuing the default

Holland & Knight's 2023 analysis of commercial lease guarantees confirms that a full or absolute guaranty can cover all monetary and non-monetary lease obligations, including insurance requirements and repair obligations.

When Does the Guarantee Activate?

The guarantee typically triggers when the tenant company:

- Fails to pay rent for a defined period

- Abandons the space

- Files for bankruptcy

- Violates material lease terms

In many cases, landlords can pursue the guarantor directly without first exhausting remedies against the tenant entity. Most founders don't realize this until they're already in default.

That exposure matters even more in NYC's competitive office market. For startups signing their first lease in Midtown, Flatiron, or SoHo, landlords will almost always require a personal guarantee — but how that guarantee is structured, and for how long, is typically open to negotiation.

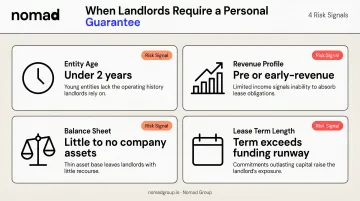

Why Landlords Require Personal Guarantees

From a landlord's perspective, a commercial office lease is a multi-year financial commitment worth hundreds of thousands — sometimes millions — of dollars. A newly formed LLC with six months of operating history and no significant assets provides very little comfort.

The personal guarantee is the landlord's insurance policy.

Risk Signals That Trigger a PG Demand

Landlords look for specific indicators when deciding whether to require a personal guarantee and how broad to make it:

- Entity age: Companies under two years old almost always face PG requirements

- Revenue profile: Pre-revenue or early-revenue companies offer limited financial certainty

- Balance sheet: Little to no company assets leaves the landlord with nothing to recover in a default

- Lease term length: A 7-year lease extending well beyond the company's funding runway raises real red flags

Even well-funded startups face PG demands in tight markets. Colliers reported Manhattan Q1 2026 leasing volume of 11.78 million SF — the strongest first quarter since 2014 — and CBRE reported Midtown Manhattan's prime vacancy rate at just 2.9%. When good space is scarce, landlords negotiate from strength.

The scope, duration, and cap of the guarantee are all negotiable. Having an experienced tenant's broker at the table — one who knows which landlords flex and where the real leverage lives — is often what separates a two-year PG from a full-term one.

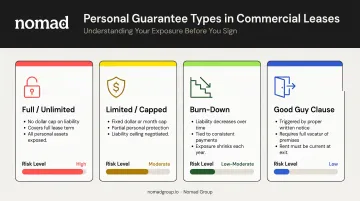

Types of Personal Guarantees You'll Encounter

Not all personal guarantees carry the same risk. Understanding the differences is the first step to knowing what to push back on.

Full (Unlimited) Personal Guarantee

This is the landlord's preferred starting position. The guarantor is personally liable for the entire value of all lease obligations for the full lease term — no financial ceiling, no time limit. Every personal asset is exposed. A 2026 New York County court judgment in 312 E. 30th LLC v BLK Empire Holdings awarded $447,685 against individual guarantors and tenant entities jointly and severally, including rent arrears, real estate taxes, late fees, and interest — with attorneys' fees reserved for later determination. That's what a full guarantee looks like when enforced.

Limited (Capped) Personal Guarantee

A capped guarantee restricts liability to a fixed dollar amount — commonly expressed as a set number of months of rent — or a defined percentage of total lease value. One New York law firm gives the example of a limited guarantee covering the first 12 months of rent as a financial cap.

This structure protects the individual from catastrophic exposure while still giving the landlord meaningful security. It's often achievable through negotiation, particularly when the tenant can demonstrate solid funding or a strong financial position.

Burn-Down Guarantee

A variation of the capped guarantee, this structure reduces the guarantor's liability over time as the lease progresses. The guarantee might start at 24 months of rent and decrease by six months for every year the tenant pays on time. Holland & Knight describes these as "burn off" or "sunset" provisions — they reward performance and reduce long-term personal risk without eliminating the landlord's upfront protection.

The "Good Guy" Clause (NYC-Specific)

This is one of the most valuable protections a tenant can negotiate in New York commercial leases. A good guy clause allows the guarantor to be released from future liability if certain conditions are met — typically:

- Providing sufficient advance written notice (terms vary by negotiation)

- Vacating the space and returning keys

- Remaining current on all rent through the move-out date

- Delivering the premises in broom-clean condition

The New York Court of Appeals recently clarified in a 2025 decision (1995 CAM LLC v West Side Advisors LLC) that guarantor liability ends upon vacatur and surrender under the guaranty's terms — without requiring separate written acceptance from the landlord, provided the guaranty itself doesn't specify that requirement. What this means in practice: the specific release conditions written into the guaranty — not general assumptions — determine when your personal liability actually stops.

A NYC commercial brokerage notes that landlords include good guy guaranties in the vast majority of NYC commercial leases. The notice period required, the condition of the premises at exit, and whether a formal landlord acceptance is needed are all points that can — and should — be negotiated before signing.

Joint and Several Guarantees

When multiple founders are involved, landlords often require joint and several liability — meaning each guarantor is individually liable for the full amount, not their proportional share. If two founders each sign a joint and several guarantee on a $2 million lease obligation, either one can be pursued for the entire $2 million. This distinction matters when determining true personal exposure for each signatory — it's not split 50/50 by default, regardless of equity split or internal agreements.

The Real Risks of Signing a Personal Guarantee

Personal Asset Exposure

A personal guarantee is not limited to business assets. If the company defaults, a landlord can pursue:

- Personal bank accounts

- Real estate holdings, including a primary residence depending on state exemptions

- Investment and brokerage accounts

- Future income

This exposure follows the individual even after the company dissolves or is wound down.

Bankruptcy Doesn't Necessarily Extinguish the Guarantee

This is one of the most common misconceptions. If the tenant company files for Chapter 11 and rejects its commercial lease, the landlord's claim against the company is subject to Bankruptcy Code limits. The personal guarantee, however, may survive entirely. The landlord can still pursue the individual guarantor for outstanding obligations, with the bankruptcy cap on the company's liability providing no protection to the guarantor.

Duration Risk in Long-Term Leases

A two-year personal guarantee is a very different commitment than a seven-year one. Founders who later exit the company, sell their equity stake, or bring in new leadership may still be personally on the hook for the remaining lease term if they failed to negotiate a release provision upfront.

Assignment of the lease doesn't automatically release original guarantors either. In a recent 312 E. 30th LLC ruling, the court held that assignment did not release the guarantors because the guaranty language explicitly stated that obligations would not be impaired by transfer.

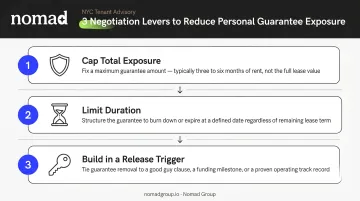

How to Negotiate Your Personal Guarantee Terms

Most founders don't realize how much of a personal guarantee is actually negotiable. The landlord's first draft is rarely the final word.

The Three Key Levers

Focus negotiation on:

- Cap your total exposure by pushing for a fixed number of months' rent rather than the full lease value

- Limit the duration by requesting a burn-down structure or time-limited guarantee instead of a full-term obligation

- **Build in a release trigger** — a good guy clause, or the right to exit the guarantee upon closing a funding round or hitting a defined revenue threshold

Using Financial Strength as Leverage

If the company has demonstrated financial credibility — through a recent funding round, strong revenue, or institutional backing — use it. Offers that give landlords comparable security without a personal guarantee include:

- A larger upfront security deposit (3–6 months of rent is a common starting point)

- A bank-issued letter of credit

- A corporate or parent company guarantee in lieu of an individual guarantee

The Value of Experienced Representation

The Nomad Group team regularly negotiates lease terms on behalf of NYC tenants, including startups navigating their first office lease. Having negotiated across 2M+ square feet of NYC office space, the team knows what's market-standard in a given building or neighborhood — and what's an overreach. That context changes what a founder ends up signing.

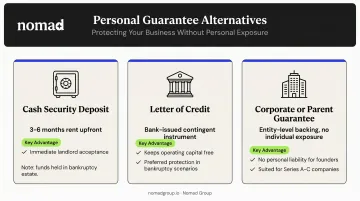

Alternatives to a Full Personal Guarantee

Security Deposit (Cash)

A substantial upfront cash security deposit — often equivalent to 3–6 months of rent — gives the landlord liquidity protection without requiring a personal guarantee. Landlords may accept this structure, particularly when the deposit size meaningfully covers their downside risk. One caveat: in a tenant bankruptcy, a cash deposit becomes property of the bankruptcy estate and may require court approval before the landlord can apply it — a meaningful constraint worth understanding before agreeing to this structure.

Letter of Credit (LOC)

A letter of credit is a bank-issued instrument that guarantees payment to the landlord if the tenant defaults. Unlike a cash deposit, the obligation sits with the bank — not the company's account — so operating capital stays free. Institutional landlords widely accept LOCs as a substitute for or supplement to personal guarantees. In tenant bankruptcy scenarios, irrevocable letters of credit are generally preferred over cash deposits because they're not property of the bankruptcy estate — meaning the landlord can draw on them without court approval.

Corporate or Parent Company Guarantee

For companies with a parent entity, holding company, or well-funded institutional backer, a guarantee from that entity can satisfy the landlord's risk requirements without exposing any individual personally. This works well for subsidiaries and Series A–C funded startups whose investors are willing to back the lease at the entity level.

Frequently Asked Questions

What is a personal guarantee in a commercial lease?

A personal guarantee is a legal commitment by an individual — typically a founder or executive — to be personally responsible for the company's lease obligations, including unpaid rent and damages, if the business entity defaults. It creates direct personal liability beyond the corporate structure.

Can a personal guarantee be negotiated in a commercial lease?

Yes. PG terms are almost always negotiable. Tenants can limit exposure through caps, burn-down structures, and good guy clauses, or reduce the need for a personal guarantee altogether by offering a larger security deposit or letter of credit.

What is a "good guy" clause in a commercial lease?

A NYC-specific provision that releases the personal guarantor from future liability after lease termination. To qualify, the tenant must give adequate advance notice, vacate properly, stay current on rent through the exit date, and return the premises in good condition. The exact release terms depend on negotiated language.

What happens to a personal guarantee if the company files for bankruptcy?

A personal guarantee typically survives a company's bankruptcy filing. The landlord can still pursue the individual guarantor for outstanding obligations, and the Bankruptcy Code's lease-claim cap does not apply to the guarantor claim — making the PG's scope and duration critical terms to nail down before signing.

How long does a personal guarantee last in a commercial lease?

Duration varies entirely by negotiation. It can span the full lease term, be time-limited to the first few years, or burn down over time as the tenant builds a payment track record. This is one of the most important terms to negotiate before signing.

Are personal guarantees required for all commercial leases?

No. Landlords typically require them for newer companies, those without strong financial history, or in highly competitive markets like NYC. Established companies with strong balance sheets and revenue history may avoid or significantly limit PG requirements.