Introduction

Most founders signing their first NYC office lease know they'll face a personal guarantee requirement. Few understand what they're actually agreeing to — or that the initial terms are almost always negotiable.

A commercial lease guarantor is a third party (an individual, parent company, or institutional entity) that agrees to cover a tenant's lease obligations if the tenant defaults. It's a simple concept with real financial consequences.

This matters most for high-growth startups, newly formed LLCs, and scaling companies without established financial track records. In competitive Manhattan neighborhoods like NoMad, Flatiron, and SoHo, landlords routinely require credit backing beyond the business entity itself — regardless of how much funding a company has raised.

Most tenants don't understand the different guarantee types, how they're structured, or what's actually negotiable — and that gap costs them at the negotiating table.

TL;DR

- A commercial lease guarantor backstops a tenant's rent and lease obligations if the tenant defaults

- Landlords require guarantors from startups and LLCs without operating history — not just financially weak companies

- Four guarantee types carry different exposure levels: Full/Absolute, Partial/Limited, Springing/Bad Acts, and Good Guy

- Guaranty terms are negotiable — scope, duration, and caps can all be structured to protect both sides

- Letters of credit, increased security deposits, and rent prepayment are all viable alternatives to a personal guaranty

What Is a Commercial Lease Guarantor Company?

A commercial lease guarantor is a third party that signs a separate guaranty contract alongside the lease, promising to fulfill the tenant's financial obligations — primarily rent, operating expenses, and related charges — if the tenant entity fails to do so.

The "company" framing matters because most commercial tenants aren't individuals. They're LLCs or corporations, which limit personal liability by design. That structure protects founders in most business scenarios, but it creates a real collection problem for landlords: if the LLC dissolves or becomes judgment-proof, a court ruling against the entity may be worthless.

A guaranty solves that by letting landlords reach beyond the entity to a person or organization with actual assets. Commercial guaranties work differently than their residential counterparts, though — and understanding those differences shapes how tenants should approach the negotiation:

- Cover larger, longer-term obligations — often $500,000 or more in total rent exposure

- Carry heavily negotiated terms, not standardized forms

- Can name a corporate parent or institutional entity as guarantor, not just an individual co-signer

Understanding this distinction matters because it shifts how tenants approach the conversation. A commercial guaranty isn't a form to sign — it's a contract to negotiate.

Why Landlords Require Guarantors in Commercial Leases

The core issue is collectability. If a tenant LLC has no track record, limited assets, or operates as a shell structure, a judgment against that entity may produce nothing. According to legal advisors at Bean, Kinney & Korman, landlords will "likely require owners to personally guarantee a new LLC's lease if the LLC has few assets or no track record." The guaranty converts a potentially hollow legal victory into a real, collectible obligation.

Which Tenants Trigger a Guaranty Requirement

Landlords most commonly require guarantors from:

- Newly formed businesses with no financial history

- Startups in early funding stages (even well-funded ones)

- LLCs with minimal balance sheets or few hard assets

- Tenants with prior defaults or weak credit

- Any company signing a high-value or long-term lease

Simply put: the larger the commitment — in square footage, term length, or total rent — the stronger the justification for a guaranty. Startups in Manhattan typically sign 3-to-5-year leases, while midsize businesses often commit to 5-7 years. That range of exposure is exactly why landlords want a backstop.

The NYC Market Context

In New York City, landlords in competitive neighborhoods like NoMad, Flatiron, and SoHo routinely require personal or corporate guarantees from any tenant that can't demonstrate sufficient operating history and net worth. According to Metro Manhattan, Good Guy Guaranties appear in the "vast majority" of NYC commercial leases — including office, loft, retail, and medical space.

That's worth keeping in mind before entering negotiations. Companies that understand what landlords are looking for — operating history, net worth benchmarks, clean financials — can structure their presentation accordingly. Nomad Group regularly works with Series A-funded startups making the transition from coworking to direct leases, helping them get ahead of these conversations rather than react to them.

A guaranty requirement isn't a red flag. Even financially strong tenants provide them. In high-value, long-duration contracts, it's simply how commercial landlords manage risk.

Types of Commercial Lease Guarantees

Guaranty type is one of the most negotiable elements of a commercial lease. Understanding the options lets tenants push for reduced exposure without derailing the deal.

Full/Absolute Guaranty

The broadest form. The guarantor is liable for all of the tenant's obligations under the lease (unpaid rent, operating expenses, non-monetary obligations like maintaining insurance) without conditions or dollar caps.

The landlord can pursue the guarantor immediately upon default, without first exhausting remedies against the tenant entity. Holland & Knight describes full guaranties as the "gold standard for most landlords" — which is exactly why tenants should push back on them.

Partial or Limited Guaranty

Partial guaranties cap the guarantor's exposure, typically in one of three ways:

- Capped at a dollar amount, such as six months of base rent

- Limited to a defined period, such as the first two years of the lease

- Restricted to monetary obligations only, excluding non-monetary defaults

Many partial guaranties also include burn-off (sunset) provisions: if the tenant stays current on rent for a defined period, the guaranty reduces or terminates automatically. Landlords may accept a 6-month security deposit that burns down to 3 months after years two or three of good standing.

Springing or Bad Acts Guaranty

This type sits dormant until a specific trigger event occurs. Common triggers include:

- Bankruptcy filing by the tenant entity

- Net worth falling below a defined threshold

- Specific "bad acts" such as fraud or hazardous contamination

For tenants, the appeal is straightforward: liability only activates for events largely within the guarantor's control to avoid. For landlords, it provides backstop coverage against the most serious default scenarios.

Good Guy Guaranty

The Good Guy Guarantee is NYC's signature compromise structure, and it's become standard in Manhattan leases for a reason. The guarantor's liability terminates when the tenant:

- Provides advance written notice (typically 90 to 180 days)

- Pays all rent through the agreed surrender date

- Vacates and returns the premises in good condition

This limits the guarantor's exposure to the period the tenant actually occupies the space. A recent New York Court of Appeals ruling (1995 CAM LLC v. West Side Advisors LLC, October 2025) confirmed that guarantor liability ends upon vacating and surrendering premises even without formal written acceptance by the landlord Review the burn-off conditions, surrender notice requirements, and any carve-outs carefully before signing.

How a Commercial Lease Guarantee Works

The guaranty is a separate contract executed alongside (or as a rider to) the lease. Here's how it flows from negotiation to enforcement.

Step 1: Landlord Requires and Defines the Guaranty

During lease negotiation, the landlord assesses whether a guaranty is required based on the tenant's financial profile and lease size. The starting position is almost always a full guaranty. This is the stage to negotiate: countering with a limited scope, a burn-off provision, or a Good Guy structure. Tenants who accept the first draft without pushback are leaving real money and protection on the table.

Step 2: Guarantor Underwriting and Execution

The guarantor submits financial documentation (typically two years of tax returns, current profit and loss statements, and a balance sheet) to demonstrate capacity to cover the obligation. Both parties' attorneys review and finalize the guaranty agreement, which is signed at lease execution alongside the lease itself.

Step 3: Enforcement Upon Default

If the tenant defaults, the landlord sends notice and, depending on guaranty type:

- Full guaranty: the landlord can pursue the guarantor directly, without first exhausting remedies against the tenant

- Partial or limited guaranty: the landlord must typically pursue the tenant before turning to the guarantor

Once triggered, the guarantor becomes responsible for the covered obligations. Standard landlord guaranty forms typically include waivers of common defenses — stripping away notice requirements and the right to demand the landlord pursue the tenant first. Legal counsel should review the guaranty before signing specifically to identify and negotiate out those waivers.

What Affects Commercial Lease Guaranty Terms

Three factors drive how aggressively landlords push for broad guaranty coverage — and how much leverage tenants have to push back.

Tenant financial profile: Companies with audited financials, institutional investors, or significant assets carry more leverage to limit guaranty scope. Landlords weigh financial liquidity, entity type, asset ownership, years in business, and their own capital expenditure on the space — including tenant improvement allowances and free rent periods. The more a landlord has invested in a deal, the more protection they'll seek.

Lease size and term: A 1-year sublease at $8,000/month carries very different guaranty expectations than a 5-year direct lease at $20,000+/month. Shorter post-pandemic lease terms — the average for smaller Manhattan tenants dropped from five to four years — support arguments for limited rather than full guaranty coverage.

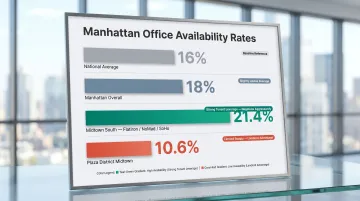

Market conditions: Manhattan's office availability rate stood at 18% at mid-2024, above the national average of 16%. Midtown South — Flatiron, NoMad, and SoHo — showed 21.4% availability in Q3 2024, giving tenants real negotiating leverage in those submarkets. Midtown's Plaza District sat at 10.6%, where landlords have far more room to insist on full guaranties.

Nomad Group's neighborhood-level knowledge of these dynamics helps clients identify where they have room to negotiate — and structure their ask accordingly.

Common Misconceptions About Commercial Lease Guarantors

A few widely held beliefs about lease guaranties can put tenants in a weaker position before they even start negotiating. Here's what the fine print actually says.

Only struggling companies need a guaranty. Most new or early-stage companies — including well-funded startups — face guaranty requirements because the LLC entity itself has no track record. A $10 million Series A doesn't automatically transfer to the LLC's balance sheet in a landlord's view.

A personal guaranty is unavoidable. Tenants can negotiate a limited guaranty, burn-off provision, or Good Guy structure — especially with broker representation. The first draft isn't the final offer; it's the starting position.

The guaranty ends when the lease ends. This one catches tenants off guard most often. Some obligations survive lease expiration — particularly outstanding rent arrears, restoration costs, or ongoing disputes. Without explicit termination language in the guaranty itself, guarantors can face liability long after they believe their exposure has ended.

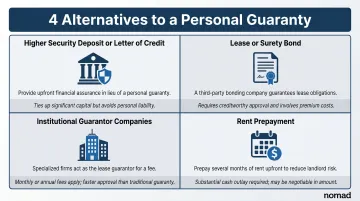

Alternatives to a Personal or Corporate Guarantor

When a traditional guaranty isn't workable, four alternatives are worth exploring with your broker and attorney.

Higher security deposit or letter of credit. Some landlords will accept a larger upfront cash deposit or a standby letter of credit in lieu of a personal guaranty. Typical ranges are 3–6 months of rent for established tenants and up to 12 months for startups. Key details to know:

- Drawing on an LOC in tenant bankruptcy generally doesn't violate the automatic stay, giving landlords immediate liquidity

- Banks charge annual fees to maintain the LOC and may require the tenant to post collateral

Lease or surety bonds. A lease bond involves a third-party surety company guaranteeing the tenant's obligations. The tenant pays the surety, provides indemnity, and agrees to reimburse any losses. It's less common, but a practical option for tenants who want to avoid personal exposure.

Institutional guarantor companies. A small number of companies — Insurent and TheGuarantors being the best-known — operate as third-party lease guarantors. Both focus primarily on residential and multifamily deals; no institutional third-party guarantor currently serves the commercial office market in NYC. Corporate parent guarantees and personal guarantees from principals remain the dominant structures here.

Rent prepayment. Some landlords will accept prepayment of the first 3–12 months of rent in place of a guaranty, reducing their exposure without requiring the tenant's principals to take on personal liability.

Frequently Asked Questions

Who can be a guarantor for a commercial lease?

A commercial lease guarantor can be an individual (typically a founder or principal), a parent or affiliated company with stronger financials, or in limited cases a third-party institutional entity. The core requirement is demonstrable financial capacity to cover the lease obligations if called upon.

Is it normal to have a personal guarantee on a commercial lease?

Yes — personal guarantees are standard in commercial leasing, especially for LLCs and new businesses without established credit history. In competitive markets like NYC, they're routinely required even for well-funded companies whose LLC entities have no operating track record.

Are there companies that act as a guarantor for commercial leases?

Institutional guarantor companies like Insurent and TheGuarantors exist, but they operate almost exclusively in the residential market. For commercial office leases, personal guarantees from principals and corporate parent guarantees remain the primary structures — no comparable institutional product has emerged for commercial tenants in NYC.

How much does it cost to hire a guarantor?

Institutional residential guarantor fees are personalized based on rent level and risk profile. For commercial deals, personal guarantors (founders, parents) bear no upfront cost but assume real financial liability. The true cost is the exposure itself — which is why negotiating a capped liability amount or burn-down provision matters before you sign.

How does a parent company guarantee work?

A parent company guarantee is a corporate guaranty where a financially stronger parent or affiliated entity co-signs the tenant subsidiary's lease obligations. If the subsidiary defaults, the landlord can pursue the parent directly — making it a practical alternative to personal guarantees when a more established entity sits above the operating company.