For many founders signing their first NYC office lease, this is the moment the process gets real. Suddenly, the LLC you formed specifically to limit personal liability isn't doing what you thought it would. Your name is on the hook, not just your company's.

Personal guarantees are standard in commercial leasing, but "standard" doesn't mean you have to accept whatever form the landlord puts in front of you. The type of guarantee, its duration, and its dollar exposure are all negotiable — and those differences can mean the gap between a manageable risk and a multi-year financial liability that follows you personally.

This post breaks down exactly what a personal guarantee is, when landlords require one, what types exist, what's actually at risk, and how to negotiate smarter — particularly relevant for startups and high-growth companies leasing space in NYC.

Key Takeaways

- A personal guarantee (PG) makes a business owner personally liable if their company defaults on a commercial lease — even through an LLC or corporation.

- Landlords routinely require PGs when the tenant entity lacks operating history, strong financials, or substantial assets.

- Four main types exist: full/absolute, limited/rolling, good guy, and springing guarantees — with very different risk profiles for each.

- Negotiation targets: cap the dollar amount, shorten the time period, add a burn-off provision, or push for a good guy clause.

- Alternatives like a larger security deposit or prepaid rent exist but are rare — landlords accept them only when tenants have significant leverage.

What Is a Personal Guarantee on a Commercial Lease?

A personal guarantee is a separate legal contract — distinct from the lease itself — in which a business owner personally promises to cover the tenant's lease obligations if the business entity defaults. That means rent, fees, damages, and other costs the tenant fails to pay.

When a business signs a lease as an LLC or corporation, the owner's personal assets are normally shielded from company debts. A PG contractually bypasses that protection.

As Holland & Knight explains, landlords require guarantees precisely because tenants may be shell companies or newly formed entities with limited assets — making a judgment against the company alone a "hollow victory."

Unlike a mortgage, a PG is an unsecured promise — not tied to any single asset. That means a landlord who wins a court judgment can potentially pursue bank accounts, real estate, vehicles, or other personal property to recover what's owed.

Three structural details define how personal guarantees work in practice:

- The lease and the guarantee are legally distinct documents with different rights and remedies, even when physically attached

- The guarantor and the tenant are treated as separate legal persons

- The landlord can, in many cases, pursue the guarantor directly without first exhausting remedies against the tenant entity

Do You Have to Sign a Personal Guarantee?

The short answer: almost certainly yes — but what you're agreeing to is negotiable.

Holland & Knight notes that landlords "routinely demand" personal or corporate guarantees where the tenant entity may have limited assets. For startups and early-stage companies, that describes virtually every deal.

When a PG Is Almost Certain

- Early-stage companies with limited or no operating history

- Businesses with revenue that looks thin relative to the rent obligation

- Companies signing their first commercial lease

- Tenants whose balance sheet doesn't support the lease term independently

When a PG May Be Reduced or Waived

- Established companies with audited financials and strong cash positions

- Large corporations with institutional credit ratings

- Tenants offering substantially higher security deposits or prepaid rent

- A highly desirable tenant in a market where the landlord has competing offers

That last point matters more than it might seem. Colliers reported Manhattan asking rent averaged $76.00/SF in Q4 2025 with over 3.9 million square feet of positive net absorption — a recovering market where well-positioned tenants carry real negotiating weight. The guarantee rarely disappears entirely, but its terms — duration, cap, burn-down schedule — are where tenants can and should push back.

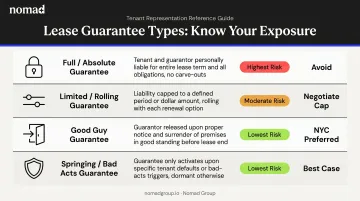

Types of Personal Guarantees in Commercial Leases

The type of guarantee matters enormously. A full guarantee and a good guy guarantee are not the same risk — not even close.

Full or Absolute Guarantee

The most landlord-favorable form. The guarantor covers all lease obligations — monetary (rent, operating expenses, utilities) and non-monetary (insurance, maintenance, repairs) — with no cap, no conditions, and no time limit.

Critically, the landlord can pursue the guarantor immediately upon default without first exhausting remedies against the tenant. If the lease also contains a rent acceleration clause — which allows the landlord to demand all remaining rent at once — the guarantor's exposure could equal years of rent in a single judgment.

Avoid this structure if at all possible.

Limited or Rolling Guarantee

A limited guarantee caps the guarantor's liability — either to a fixed dollar amount or a defined number of months of rent. A "rolling" structure means total liability never exceeds that cap at any point during the lease, even as the remaining term shrinks.

Burn-off provisions are the key feature to negotiate here: liability decreases incrementally over time (often tied to on-time payment history) and eventually terminates entirely before the lease ends. This is one of the most practical protections a founder can secure.

Good Guy Guarantee

Especially common in New York City. Pryor Cashman describes it as a "ubiquitous concept" in many NYC commercial leases.

Under a good guy guarantee, the founder's personal liability ends when the tenant properly surrenders the premises — meaning:

- Advance written notice is given (typically 3-6 months)

- Rent is current through the surrender date

- The space is returned in good condition

This is particularly valuable for startups that may need to pivot, downsize, or relocate. Instead of being personally liable for years of remaining rent, you exit cleanly as long as you follow the surrender conditions.

Springing or Bad Acts Guarantee

Tenant-favorable and rare. This guarantee only activates on a specific triggering event — tenant bankruptcy, fraud, intentional property damage, or net worth dropping below a defined threshold. Outside those scenarios, the guarantor has no exposure at all.

It's worth pursuing if you have real negotiating leverage, but treat it as an upside ask, not a starting position.

At a Glance: Guarantee Types Compared

| Guarantee Type | Liability Scope | Landlord Favorability | Best For |

|---|---|---|---|

| Full / Absolute | Unlimited — all obligations, no cap | Highest | Avoid if possible |

| Limited / Rolling | Capped by dollar amount or months; burns off over time | Moderate | Negotiating a defined ceiling |

| Good Guy | Ends upon proper surrender of premises | Moderate | Startups needing exit flexibility |

| Springing / Bad Acts | Triggered only by specific bad acts | Lowest | Strong bargaining positions |

What Personal Assets Are at Risk?

Under a full guarantee, a defaulting tenant leaves the guarantor exposed to significant personal collection risk. According to Nolo, judgment creditors can pursue:

- Real estate — including a primary residence in many states

- Bank and investment accounts

- Vehicles

- Stocks, bonds, and other personal property

Unlike a secured loan, the PG isn't attached to one asset. A court judgment means the landlord can pursue any of the above. The landlord's attorneys will conduct a thorough financial disclosure process to identify what you own.

That exposure isn't uniform across every state, though. Florida and Texas offer strong homestead protections under their constitutions that can shield a primary residence from forced sale. Those protections are real — but they're state-specific and don't extend to bank accounts, vehicles, or investment holdings.

Consider a concrete example: a tenant defaults in year two of a five-year deal. The landlord accelerates rent, demanding all remaining payments immediately. At Manhattan's current average of ~$76/SF, a modest 2,000 SF office with three years remaining represents roughly $456,000 in potential accelerated exposure (before legal fees, operating expenses, and damages). That figure comes out of the guarantor's personal assets — not the company's.

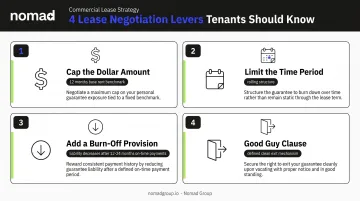

How to Negotiate a Personal Guarantee

The guarantee itself may be unavoidable. Its terms are not.

Four Core Negotiation Levers

- Cap the dollar amount — Push for a fixed ceiling — 12 months of base rent is a common benchmark — rather than unlimited exposure across the full term.

- Limit the time period — Ask for a rolling structure where total exposure never exceeds the cap, regardless of how far into the lease you are.

- Add a burn-off provision — Request that liability decreases after 12-24 months of on-time payments and terminates entirely before the lease ends.

- Good guy clause — For NYC startups, this is often the most valuable swap available: replace a full guarantee with a good guy structure that gives you a defined, clean exit mechanism.

The Joint and Several Problem

When multiple founders sign a lease, landlords typically require joint and several liability — meaning any one partner can be pursued for the full amount. Push back on this. The goal is to limit each partner's liability to their proportional ownership stake, with the agreement documented in a side agreement among guarantors.

Alternatives to a PG

Security deposit substitutes and prepaid rent arrangements do exist, but they're not common. A landlord may accept a larger upfront deposit — several months held in escrow — in lieu of a personal guarantee when:

- The tenant has audited financials demonstrating financial strength

- The tenant is highly desirable (specific industry, strong brand)

- The market favors tenants (vacancy up, few competing deals for that space)

These alternatives require genuine leverage. Don't lead with them unless you have the financials to back the ask.

Working with the Right Representation

Knowing which of these levers is realistic — and how to frame them with a specific landlord — directly shapes which terms you walk away with. Nomad Group has negotiated hundreds of NYC office leases across Flatiron, NoMad, SoHo, Williamsburg, and beyond, working with startups from their first lease through Series C expansions.

That transactional history tells you which landlords routinely accept good guy clauses, which will negotiate burn-offs, and which terms are off the table in current market conditions.

Frequently Asked Questions

What is a personal guarantee on a commercial lease?

A PG is a separate legal contract making a business owner personally responsible for the tenant's lease obligations — rent, fees, and damages — if the business entity defaults. It contractually bypasses the liability protection an LLC or corporation would otherwise provide.

Do I have to personally guarantee a commercial lease?

In most cases, yes — especially for newer businesses without established credit or financial track records. The guarantee itself is often non-negotiable, but its structure, dollar cap, duration, and conditions are all negotiable.

What happens if I can't pay a personal guarantee?

The landlord can pursue a court judgment and go after personal assets including bank accounts, real estate, and other valuables. If the lease includes an acceleration clause, the landlord may demand all remaining rent at once, compounding the exposure significantly.

How can I get out of a personal guarantee on a commercial lease?

Exiting a signed PG is difficult. Options include triggering a good guy clause exit (surrendering the premises properly), negotiating a settlement with the landlord, or — in extreme cases — filing personal bankruptcy, which Nolo identifies as a mechanism that can discharge PG debt under qualifying circumstances.

Is a good guy guarantee better for tenants?

Yes. For NYC founders especially, a good guy guarantee is the most practical protective structure — it caps liability to the period you actually occupy the space and provides a defined, manageable exit path if your business needs change.

Can you negotiate a personal guarantee on a commercial lease?

Yes. The type, duration, dollar cap, and triggering conditions are all negotiable. Push for a limited or rolling structure with a burn-off provision — or ideally a good guy clause — rather than an unlimited, full-term guarantee.