Introduction

Picture this: a Series A startup has been in their Flatiron office for two years. The suite next door opens up — perfect for the team they're about to hire. But before they can make a move, another tenant swoops in and signs a lease on it.

If only they'd negotiated a right of first refusal.

A right of first refusal (ROFR) is a lease provision that gives tenants the option to lease additional space before a landlord can offer it to outside parties. It's one of the most valuable — and most misunderstood — clauses in commercial real estate. This guide covers how ROFR works, when landlords will (and won't) agree to it, how it differs from a right of first offer, and how to negotiate terms that actually protect your growth plans.

Key Takeaways

- A Right of First Refusal (ROFR) gives a tenant the option to match any offer a landlord receives before leasing that space to a third party

- ROFR clauses apply most often to adjacent or nearby space — useful for growing companies that expect to expand

- The right is triggered only when the landlord receives a bona fide third-party offer, not when space simply becomes vacant

- Negotiation details matter: response windows (typically 5–10 business days), market-rate pricing, and carve-outs all affect how useful the clause actually is

- A poorly drafted ROFR can leave tenants with little real protection — getting the language right is critical

What Is a Personal Guarantee in a Commercial Lease?

A personal guarantee (also written as "personal guaranty") is a legally binding promise by an individual — typically the business owner or founder — to fulfill the tenant company's lease obligations if the company defaults.

Forming an LLC or corporation normally shields your personal assets from business debts. A personal guarantee contractually bypasses that protection. As Holland & Knight explains, landlords use guarantees to give themselves a direct claim against the individual — not just the business entity.

What the Guarantor Is Actually Agreeing To

Depending on how the guarantee is drafted, the guarantor may be liable for:

- Monetary obligations: rent arrears, CAM fees, operating expense escalations

- Non-monetary obligations: maintenance requirements, insurance, repair costs

- Post-default costs: legal fees, damages from breach of lease terms

The guarantee remains enforceable even if the company is dissolved — shutting down the LLC doesn't end your personal exposure.

Enforceability in New York

Under New York General Obligations Law Section 5-701(a)(2), a promise to answer for another party's debt or default must be in writing and signed by the guarantor to be enforceable. A guarantee that doesn't meet these requirements can be challenged — but a well-drafted one from a sophisticated landlord's attorney will hold up.

Treat every guarantee as a live personal obligation from the moment you sign.

When Do NYC Landlords Typically Require a Personal Guarantee?

Guarantees aren't universal, but in NYC they're close to it for certain tenant profiles. Four situations reliably trigger a landlord's demand:

- Startups and newly formed entities — an LLC with no operating history gives a landlord almost no recourse if things go wrong

- Businesses with limited financial documentation — no audited financials, no credit history, no demonstrated revenue

- Weak credit or prior payment issues — any red flag in the tenant's financial background

- Longer or higher-value leases — the greater the landlord's exposure, the more protection they'll want

The NYC Market Reality

Manhattan's office market has tightened considerably. According to Newmark's Q1 2026 Manhattan Office Market Report, Manhattan availability fell for eight consecutive quarters, dropping from 19.5% in Q1 2024 to 14.6% by Q1 2026. In neighborhoods like Flatiron and NoMad — where Nomad Group focuses much of its tenant representation work — landlords increasingly hold leverage on desirable spaces.

That said, Cushman & Wakefield reported Midtown South vacancy at 22.8% in Q1 2026. Conditions vary by building and submarket, which means funded startups with clean financials can negotiate guarantee terms — particularly in buildings with higher vacancy.

When a Guarantee May Not Be Required

A small subset of tenants can avoid personal guarantees entirely:

- Large enterprise tenants with audited financials and demonstrated creditworthiness

- Well-capitalized companies offering significant alternative security upfront

- Tenants whose balance sheet clearly supports the full lease obligation

For early-stage companies, these conditions are rarely met — which makes understanding how to negotiate guarantee terms, or offer alternative security, one of the more valuable skills in the leasing process.

Types of Personal Guarantees You'll Encounter

Guarantees aren't one-size-fits-all. There's a spectrum from maximum landlord protection to more tenant-friendly structures — and knowing which type you're being asked to sign is the first step to negotiating it.

Full or Absolute Guarantee

The landlord's preferred starting point. A full guarantee makes the guarantor liable for all tenant obligations under the lease — both monetary (rent, operating expenses) and non-monetary (insurance, maintenance). There are no conditions or triggers; the landlord can pursue the guarantor directly upon default without additional steps.

This is the highest-exposure structure for founders. If you see a full guarantee in a first draft, treat it as an opening position, not a final one.

Limited or Partial Guarantee

Liability is capped — either by dollar amount, time period, or the specific obligations covered. Two variations worth knowing:

- Rolling guarantee — exposure stays constant (for example, always capped at 12 months of rent) rather than accumulating over the lease term

- Burn-off or sunset provision — the guarantor's liability decreases over time and may expire entirely after a defined period of on-time payments

Holland & Knight confirms both structures as recognized commercial lease guarantee forms. Burn-off provisions are a strong negotiating win for startups: they reward financial discipline and give founders a milestone to work toward.

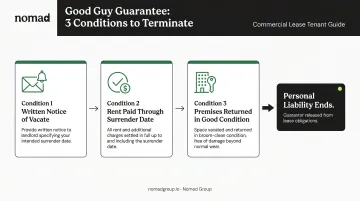

Good Guy Guarantee

This is the NYC standard, and for most startup founders negotiating their first commercial lease, it's the most important structure to understand.

Under a Good Guy Guarantee, the guarantor's personal liability ends when three conditions are met:

- The tenant provides advance written notice of intent to vacate (typically 3–6 months)

- Rent is paid in full through the surrender date

- The premises are returned in good condition

The New York Court of Appeals addressed this structure in 1995 CAM LLC v. West Side Advisors LLC (2025), holding that a guarantor's liability ended upon vacatur and surrender because the guarantee did not require landlord acceptance of surrender as an express condition.

The lesson for tenants: exact language controls the outcome. Review surrender conditions, notice periods, and any surviving obligations carefully before signing.

Springing or Bad Acts Guarantee

This guarantee only activates upon specific triggering events — typically bankruptcy, insolvency, the tenant's net worth falling below a defined threshold, or deliberate bad acts like fraud or property damage. It's less common than the structures above, and more tenant-friendly than a full guarantee. That said, the trigger definitions deserve close scrutiny: a vaguely drafted threshold can expose a guarantor to liability they didn't expect.

How to Negotiate Your Personal Guarantee

A landlord asking for a guarantee is rarely the end of the conversation — it's the opening move. Most terms are negotiable, and your leverage depends on financial strength, market conditions, and how desirable your tenancy is to the landlord.

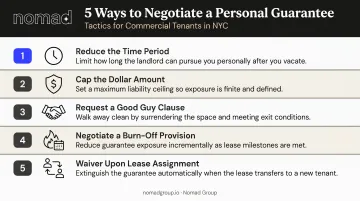

Nomad Group's tenant representation team, which has leased over 2 million square feet across NYC's most competitive neighborhoods, regularly navigates these negotiations on behalf of startup and growth-stage clients. Here are the five most effective tactics:

Tactic 1 — Reduce the Time Period

Push to limit the guarantee to 12–24 months rather than the full lease term. Most lease defaults happen early, so landlords often accept shorter windows when the tenant has some demonstrated financial credibility. A rolling guarantee structure — where exposure stays capped at a fixed number of months regardless of where you are in the lease — is a strong outcome.

Tactic 2 — Cap the Dollar Amount

Negotiate a maximum dollar figure rather than open-ended exposure. If total rent over five years is $750,000, a $150,000 cap is a fundamentally different liability than unlimited personal obligation. Frame the cap around the landlord's realistic recovery window, not the full contract value.

Tactic 3 — Request a Good Guy Clause

In NYC, asking for a Good Guy Guarantee is standard practice. Landlords expect it and rarely view the request as aggressive. Focus your negotiation on the details:

- Notice period — 3 months is more tenant-friendly than 6

- Surviving obligations — check whether restoration obligations outlast the guarantee termination

- Surrender conditions — ensure "good condition" is defined clearly, not left open to interpretation

Tactic 4 — Negotiate a Burn-Off Provision

Ask for the guarantee to reduce or expire automatically after a defined period of clean payment history — typically 24 or 36 months. This aligns the landlord's protection with actual default risk and gives founders a concrete milestone where personal exposure ends.

Tactic 5 — Waiver Upon Lease Assignment

Without this clause, the original guarantor may remain personally liable even after selling the business or exiting. Ask explicitly that the guarantee be released upon a legally approved lease assignment or transfer to a creditworthy new tenant.

Alternatives to a Personal Guarantee

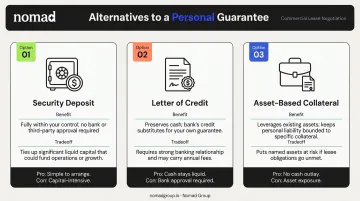

For tenants who want to avoid personal exposure entirely — or reduce its scope — three alternatives are worth understanding:

Security deposit / cash deposit The tenant places a cash deposit (typically 2–12 months of rent, depending on the landlord's risk assessment) in a landlord-held account. The landlord can draw on it without litigation if the tenant defaults. The tradeoff: this locks up working capital. For Series A companies, depleting cash reserves for a deposit can be more operationally damaging than the guarantee itself.

Letter of credit A standby letter of credit is a bank commitment to pay the landlord up to a defined amount if lease-default conditions are met. Patterson Belknap's analysis notes that courts have consistently held that a landlord's right to draw on a letter of credit is not blocked by a tenant's bankruptcy automatic stay — more landlord-friendly than a cash deposit, and more capital-efficient than fronting a large sum upfront. The catch: it requires an established banking relationship and sufficient creditworthiness to obtain.

Asset-based collateral or co-tenants In some deals, a landlord may accept a lien on business assets — equipment, IP, receivables — or the addition of a financially strong co-tenant. This is less common and requires case-by-case negotiation, but it's worth raising for tenants with significant non-cash assets and limited liquid capital.

Frequently Asked Questions

Is it normal to have a guarantor on a commercial lease?

Yes, standard practice — especially in NYC and for newer businesses without established financial histories. Landlords view guarantees as baseline protection, not a signal of distrust. Even well-funded startups routinely face guarantee requests on their first office lease.

What is a "Good Guy" guarantee on a commercial lease?

A Good Guy Guarantee limits the guarantor's liability to the tenant's active occupancy period. Once written notice is given, rent is paid through move-out, and the space is surrendered in good condition, the guarantee terminates. It's common — and expected — in NYC commercial leases.

What is the minimum income required for a commercial lease guarantor?

There's no universal minimum. Landlords evaluate guarantors case by case based on net worth, liquid assets, and total lease obligation. A guarantor should generally demonstrate the ability to cover 12–24 months of rent from personal assets, though this varies by deal.

Can you negotiate out of a personal guarantee on a commercial lease?

Complete elimination is possible for well-capitalized tenants, but uncommon for early-stage startups. More realistic targets include:

- Limiting the guarantee's duration

- Capping the total dollar amount

- Adding a Good Guy clause

- Negotiating a burn-off provision tied to on-time payment history

What happens if a personal guarantor cannot pay?

The landlord can pursue legal action — including New York's CPLR 3213 summary judgment procedure, which enforces the guarantee without a full trial. They may also draw on held rent deposits, seek possession of the premises, or negotiate a repayment arrangement directly with the guarantor.

What are alternatives to a personal guarantee on a commercial lease?

The main alternatives are a cash security deposit, a standby letter of credit, asset-based collateral, or a creditworthy corporate guarantor such as a parent company. Which option works best typically comes down to how much working capital the tenant can tie up versus the strength of their banking relationship.