The short answer is no. But the reasoning matters, especially if you're a business owner deciding which professionals to engage for a major office commitment, or an investor trying to understand what your brokerage partner can and cannot advise you on.

This article breaks down exactly what separates a financial intermediary from a real estate brokerage, where they overlap structurally, and why getting this distinction right has practical consequences for your business.

Key Takeaways

- A financial intermediary pools, holds, or transforms capital — banks, mutual funds, and insurance companies are the classic examples

- Real estate brokerages connect parties in property transactions but never take custody of client capital

- Both reduce information gaps between two parties, which is why the terms get conflated

- Real estate brokers answer to state licensing boards; financial intermediaries face federal oversight from the SEC, FINRA, and bank regulators

- For major lease commitments, you need both a commercial broker and a financial advisor — each covers a distinct domain

What Is a Financial Intermediary?

Investopedia defines a financial intermediary as an institution that stands between savers and borrowers, performing asset transformation, risk transformation, and information production. The critical word is transformation — a financial intermediary doesn't just connect two parties, it takes capital in one form and converts it into another.

The Core Mechanics

A bank accepts deposits — short-term liabilities to depositors — and converts them into long-term loans, bearing the credit risk in between. An insurance company collects premiums and assumes risk on behalf of policyholders, with real financial exposure if claims exceed projections. In both cases, the intermediary takes a position. It holds something, and it bears consequences if that position goes wrong.

That's what separates a financial intermediary from a matchmaker. A matchmaker connects two parties and walks away. An intermediary stays in the transaction, holding capital and managing the exposure that comes with it.

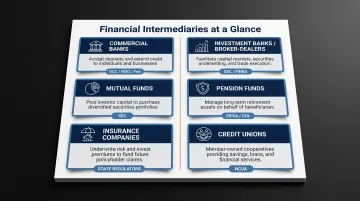

Primary Types of Financial Intermediaries

| Type | Core Function |

|---|---|

| Commercial banks | Accept deposits, issue loans; regulated by OCC/FDIC/Fed |

| Investment banks / broker-dealers | Underwrite securities, execute trades; subject to SEC and FINRA oversight |

| Mutual funds | Pool investor capital into diversified portfolios |

| Pension funds | Collect contributions, manage long-term retirement assets under ERISA |

| Insurance companies | Pool premiums to pay claims; regulated at the state level |

| Credit unions | Member-owned depositories supervised by the NCUA |

Why Regulation Follows Custody

The regulatory logic is straightforward: financial intermediaries are subject to federal oversight — SEC, FINRA, OCC, FDIC — precisely because they hold or manage other people's money. Broker-dealers, for instance, must safeguard customer funds and securities under SEA Rule 15c3-3, maintaining reserve accounts specifically to protect client assets.

Securities brokers (stockbrokers) occupy a gray area here. They're often classified as financial intermediaries because they maintain client accounts and execute trades on behalf of clients. Real estate brokers don't maintain those kinds of accounts, which is precisely where the comparison breaks down.

What Does a Real Estate Brokerage Firm Actually Do?

A real estate brokerage represents buyers, sellers, landlords, or tenants in property transactions. Brokers facilitate negotiations, manage the deal process, and earn a commission when the transaction closes. They are agents — not principals with capital at stake.

Two Sides of Brokerage

On the tenant/buyer side, the broker works on behalf of a company searching for space — identifying properties, coordinating tours, analyzing market comparables, and negotiating lease or purchase terms.

On the landlord/seller side, the broker lists and markets properties, fields inquiries, and works to secure qualified tenants or buyers at favorable terms for the property owner.

Commercial brokerage goes further than those two sides suggest. Unlike residential practice, it layers in lease structuring, buildout coordination, market analysis, and space strategy tied directly to a company's growth trajectory.

The Expanded Role of Modern Commercial Brokerages

Firms like Nomad Group have extended well beyond the transaction. Their platform covers tenant representation, construction management, facilities management, and asset management — functioning as a full-service real estate partner rather than a one-time deal facilitator. Nomad has completed over 300 tenant buildouts across NYC and manages more than 2 million square feet, which illustrates how commercial brokerage has evolved into ongoing operational partnership.

Even so, the classification stays the same. Operational depth doesn't convert a service firm into a financial intermediary — these remain real estate and property services, not capital management or investment advisory functions.

Compensation Structure

Real estate brokers earn commissions paid by landlords or sellers. How that differs from financial intermediary revenue:

- Brokers: Commission on closed transactions (paid by the property owner)

- Financial intermediaries: Interest income, fund returns, or risk premiums tied to capital deployment

That distinction in fee structure reflects something deeper — brokers have no financial stake in client capital. They facilitate; they don't manage money.

New York-licensed brokers operate under Article 12-A of the Real Property Law, governed by the Department of State, not by financial regulatory bodies like the SEC or FINRA.

Where Real Estate Brokerages Overlap With Financial Intermediaries

The confusion isn't baseless. Real estate brokerages and financial intermediaries share clear structural similarities.

Information asymmetry is one shared trait. Research in the Journal of Real Estate Finance and Economics finds that real estate markets carry significant asymmetry because properties are heterogeneous and trade infrequently. Brokers reduce those frictions by providing local market knowledge, comparable lease rates, and transaction expertise neither party alone possesses. Banks do something structurally similar: they evaluate creditworthiness that borrowers can't credibly signal on their own.

Search costs are another overlap. Both broker types solve a matching problem. Without a broker, a startup looking for 8,000 square feet in Flatiron and a landlord with a vacant floor would struggle to find each other, assess fit, and structure a deal. That search function mirrors what financial intermediaries perform in capital markets.

Scale of capital committed ties them together as well. Global commercial real estate transaction volumes reached approximately $703 billion in 2024, with U.S. office leasing volumes running about 18% above 2023 levels. A 10-year lease on a Manhattan office floor can represent millions of dollars in committed capital. Brokers don't hold that capital, but they're central to the decision that commits it.

M&A advisory literature regularly cites real estate agents as the textbook non-financial example of intermediation logic — which confirms the structural parallel, and also marks exactly where the comparison stops.

Key Differences: Why Real Estate Brokerages Aren't Traditional Financial Intermediaries

The similarities are real but don't survive the decisive test: capital custody.

Financial intermediaries hold, pool, or transform capital. A bank takes deposits and makes loans. A fund pools investor money. An insurer collects premiums and assumes risk. Real estate brokers never hold client capital — they facilitate a transaction between two other parties and step back.

Risk exposure draws the sharpest line. A bank bears credit risk on every loan it issues. A mutual fund bears market risk on assets it holds. A real estate broker earns or loses a commission based on whether the deal closes — but has no exposure to the capital outcome of the underlying transaction.

The regulatory framework confirms this. Because real estate brokers don't manage or custody funds, they fall entirely outside federal financial regulation. New York-licensed brokers operate under state real estate law — licensing, agency disclosures, continuing education — a fundamentally different compliance environment from SEC registration or FINRA oversight.

There is one nuance: in New York transactions, a broker may sometimes hold a down payment in escrow while the transaction is pending. That limited arrangement is not the same as ongoing asset management or pooled intermediation — and it's governed by specific rules requiring separate accounts and no commingling with firm funds.

Why the Distinction Matters for Your Business

Getting this right has practical implications, not just conceptual ones.

Understanding What Your Broker Can and Cannot Advise On

A commercial real estate brokerage's duty runs to your real estate interests — market conditions, lease structures, space strategy, buildout timelines, and negotiation outcomes. That's a real and valuable form of expertise.

Nomad Group, for instance, works with scaling companies across NYC to handle everything from initial space search through construction management and facilities operations — all within that commercial real estate scope.

What a brokerage cannot do is advise on investment returns, capital structure, or portfolio-level financial risk. Those questions belong to a registered investment adviser or corporate finance team operating under a different regulatory framework — the Investment Advisers Act of 1940, not state real estate licensing law.

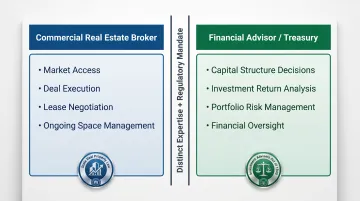

When to Engage Both

Companies making significant real estate commitments — long-term leases, custom buildouts, asset acquisitions — benefit from working with both:

- Brokerage — market access, deal execution, lease negotiation, and ongoing space management

- Financial advisor or internal treasury — capital structure decisions, investment return analysis, and portfolio-level risk management

Each role requires distinct expertise and a different regulatory mandate. A broker who tries to provide investment advice is operating outside both their expertise and their license. A financial advisor who tries to negotiate a commercial lease lacks the market knowledge and deal-specific context to do it effectively.

For NYC companies navigating significant space decisions, that means knowing when to call your broker — and when to loop in your CFO.

Frequently Asked Questions

Is a real estate brokerage firm a financial intermediary?

A real estate brokerage is an intermediary in the general sense — it connects buyers and sellers or tenants and landlords. But it is not a financial intermediary in the technical sense because it does not hold, pool, or manage capital on behalf of clients — the defining requirement of that classification.

What is considered a financial intermediary?

A financial intermediary is any entity that channels funds between savers and borrowers or manages capital on behalf of clients. Classic examples include banks, mutual funds, insurance companies, and pension funds. What sets them apart: the intermediary takes an active position in capital — it holds or transforms funds, rather than simply facilitating a transaction between two parties.

What are the main types of financial intermediaries?

The primary types include:

- Commercial banks — accept deposits and issue loans, bearing credit risk directly

- Investment banks and broker-dealers — underwrite and trade securities on behalf of clients or their own accounts

- Mutual funds — pool investor capital into diversified portfolios

- Pension funds — manage long-term retirement assets on behalf of beneficiaries

- Insurance companies — pool premiums and assume policyholder risk

- Credit unions — member-owned depository institutions offering similar services to banks

Each holds or manages client capital under a specific regulatory framework.

What is the difference between a real estate broker and a financial intermediary?

The key difference is capital custody. Financial intermediaries hold or manage client funds and bear ongoing financial risk as a result. Real estate brokers facilitate transactions as agents — they never control the capital involved, and unlike a bank that carries credit risk through the life of a loan, a broker earns a commission at closing and has no further exposure to the deal's outcome.

Do real estate brokers have a fiduciary duty to their clients?

Fiduciary duty in real estate varies by state and representation type. In New York, brokers owe agency duties under Article 12-A of the Real Property Law, including disclosure obligations. This duty applies to the transaction and negotiation — not to financial or investment advice, which falls outside a broker's licensed scope.

What's the difference between a residential and commercial real estate brokerage?

Commercial brokerages handle office, retail, and industrial space with significantly more complexity than residential transactions — longer deal timelines, intricate lease structures, tenant improvement negotiations, and often additional services like construction management, market analysis, and facilities oversight. Nomad Group's commercial model, for example, covers the full lifecycle from lease search through buildout and ongoing operations, which residential brokerages don't offer.