Introduction

Signing a multi-year NYC office lease is one of the most consequential financial commitments a growing company will make — and one of the most misunderstood. The rent per square foot on a listing rarely tells the full story. Hidden cost layers can push your actual occupancy cost 20–40% above the headline number.

That gap isn't accidental. Commercial leases are layered documents, and most tenants don't fully understand what they've agreed to until an unexpected true-up bill arrives.

This guide covers what actually makes up your rent, how the three main lease structures shift costs between landlord and tenant, and where tenants consistently leave money on the table.

Key Takeaways

- A commercial lease payment includes base rent plus operating expenses, CAM charges, and annual escalations — the headline rate is rarely the total cost.

- Gross, net (NNN), and modified gross leases assign operating cost responsibility differently — misreading the structure is an expensive mistake.

- Escalation clauses, free rent periods, and TI allowances carry real dollar impact and belong at the center of every negotiation.

- NYC asking rents range from ~$59/SF Downtown to ~$85/SF in Midtown and Midtown South; quoted rent and true occupancy cost rarely match.

- Rentable vs. usable square footage confusion, CAM reconciliation exposure, and misreading free rent as savings are the most common and costly tenant mistakes.

What's Actually Included in a Commercial Lease Payment

Most tenants budget for rent. What they actually owe is more complicated.

A commercial lease payment has multiple line items, and the gap between "quoted rent" and "total cost of occupancy" can be significant. Knowing each component before signing is the difference between an accurate budget and an unpleasant surprise eighteen months in.

Base Rent

Base rent is the foundational charge: a fixed per-square-foot rate applied to the rentable square footage (RSF) of your space, typically expressed as an annual figure billed monthly.

The formula is straightforward:

Annual base rent = $/RSF × total RSF Monthly payment = annual base rent ÷ 12

So a 4,000 RSF space at $80/SF costs $320,000 annually, or roughly $26,667/month. That's the floor of your cost — not the ceiling.

Operating Expenses and NNN Charges

Operating expenses (OpEx) are the landlord's costs of running the building: property taxes, building insurance, and maintenance. In net leases, these are passed through to tenants proportionally.

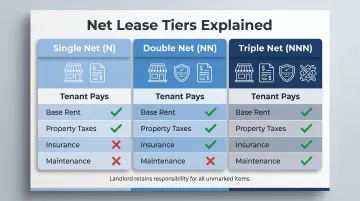

The three tiers of net lease pass-throughs:

- Single net (N): Base rent plus property taxes — landlord still covers insurance and maintenance

- Double net (NN): Base rent plus taxes and building insurance — maintenance stays with the landlord

- Triple net (NNN): Base rent plus all three — taxes, insurance, and full operating/maintenance costs

Under a NNN structure, your base rent is typically lower, but you absorb full operating cost variability. A bad winter, a tax reassessment, or a major building repair can all affect what you owe.

CAM Charges

Common area maintenance (CAM) charges are your proportionate share of costs to maintain shared spaces — lobbies, elevators, hallways, restrooms, and building systems. CAM is typically estimated at lease signing and reconciled annually against actual costs, which can generate year-end reconciliation charges you didn't budget for.

One provision tenants frequently miss: gross-up clauses. Landlords may gross up variable expenses (like cleaning or HVAC) to 95% or 100% occupancy when calculating your share — even if the building is only 70% occupied.

The effect is that your CAM bill reflects a fuller building than actually exists, inflating your proportionate cost. Before signing, verify:

- The gross-up percentage being applied

- Which specific expenses are subject to gross-up

- Whether any annual caps limit your exposure

The Main Commercial Lease Structures Explained

Accepting a lease structure without fully understanding it is one of the most common and costly tenant mistakes. Each structure allocates operating cost risk differently, and two spaces quoted at the same $/RSF can have very different actual cost profiles.

In NYC's office market, modified gross and full-service gross leases dominate multi-tenant office buildings. NNN arrangements appear primarily in retail and industrial contexts.

| Lease Type | Tenant Pays | Best For |

|---|---|---|

| Gross (Full-Service) | Base rent only | Predictable budgets, multi-tenant office |

| Triple Net (NNN) | Base rent + taxes + insurance + maintenance | Retail, industrial, single-tenant |

| Modified Gross | Base rent + negotiated pass-throughs | NYC mid-market office, flexible deals |

Gross Lease (Full-Service Lease)

In a gross (full-service) lease, the tenant pays a single all-inclusive rent figure and the landlord covers all operating expenses from that payment. The appeal is straightforward: predictable monthly costs with no surprise invoices.

The trade-off: landlords price gross leases higher to absorb OpEx risk. And most gross leases aren't truly all-inclusive — they use a base year mechanism.

The landlord covers operating expenses up to the level incurred during the base year — typically the first lease year. Any increases above that threshold are passed through to the tenant proportionally.

The timing of your signing matters here. A high-expense base year is actually favorable: future cost increases above it will be smaller. Sign in a low-expense year, and you carry more exposure as costs climb.

Net Lease (NNN)

In a triple net lease, the tenant pays base rent plus their proportionate share of all three nets: property taxes, building insurance, and maintenance. Base rent is typically lower than in a gross lease, but the tenant assumes full operating cost variability.

NNN leases are more common in retail, industrial, and single-tenant buildings. In Manhattan's multi-tenant Class A office market, you're more likely to encounter base-year gross or modified gross structures — though NNN-like recoveries can be embedded through expense stops.

Modified Gross Lease

A modified gross lease is a negotiated hybrid: some operating expenses are bundled into rent, others are passed through separately. Because the tenant and landlord negotiate which expenses fall on each side, it's the most adaptable structure — and the most common in NYC's mid-market office segment.

Typically, base rent covers property taxes and insurance, while utilities, janitorial services, or above-base-year OpEx increases fall on the tenant. The exact split varies deal by deal.

That variability is why lease abstract review matters in modified gross arrangements. Two leases quoted at $75/SF in the same neighborhood can carry very different true costs once pass-throughs are factored in. The headline number tells you almost nothing without knowing which side of the line each expense falls on.

Key Lease Terms That Directly Affect What You Pay

These provisions modify, cap, expand, or defer the payment obligations established by your lease structure. Understand each one before you sign — they're where landlords and tenants negotiate the real economics of a deal.

Annual Rent Escalation Clauses

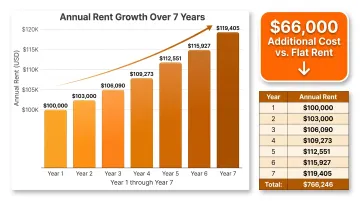

Most commercial leases include annual rent increases — either a fixed percentage (commonly 2–3% per year) or a CPI-linked adjustment. The compounding effect over a multi-year term is significant.

A simple illustration: starting base rent of $100,000/year at 3% annual escalation over a 7-year term:

| Year | Annual Rent |

|---|---|

| 1 | $100,000 |

| 2 | $103,000 |

| 3 | $106,090 |

| 4 | $109,273 |

| 5 | $112,551 |

| 6 | $115,927 |

| 7 | $119,405 |

| Total | $766,246 |

Without escalation, you'd pay $700,000 over the same period. That's a $66,000 difference — just from a 3% annual increase. Model your full-term obligation, not just year-one rent.

Free Rent Periods

Free rent (abatement) refers to months at the start of a lease term during which no base rent is owed. It's typically granted to offset buildout disruption or to make a deal competitive when landlords don't want to reduce the stated rent.

Three things to know before counting on abatement:

- Operating expenses still apply in most structures — free rent means base rent relief only, not a full cost holiday

- Clawback provisions require repayment if you exit early; know exactly what triggers repayment before relying on abatement as a budget benefit

- Abatement timing matters — front-loaded free rent is more valuable than back-loaded; model the net present value, not just the gross months

Tenant Improvement (TI) Allowances

A TI allowance is the landlord's contribution toward building out the space to your specifications, expressed in dollars per square foot. It's one of the most negotiated concession items in NYC.

CBRE reported that average U.S. TI allowances declined from $97.55/SF in 2023 to $87.51/SF in 2024 as landlords pulled back on concessions. NYC fit-out costs can exceed $212/SF according to Cushman & Wakefield's fit-out cost data — so the allowance frequently covers only a fraction of actual buildout cost.

The practical implication: TI allowances are effectively amortized into your rent. Landlords offering higher TI typically charge higher base rent to recover the investment. Evaluate TI as part of the total deal economics, not as a free benefit sitting outside the rent calculation.

Security Deposits and Letter of Credit Requirements

NYC commercial landlords typically require a security deposit or letter of credit (LOC) as financial protection. The amount — often 3–6 months of base rent for creditworthy tenants, and potentially 6–12 months for early-stage companies with limited operating history — is negotiable.

Key negotiation points:

- LOC vs. cash deposit: Letters of credit preserve your operating capital; cash deposits tie up liquidity

- Burn-down provisions: Allow the security to decrease over time as you establish a payment track record — negotiate clear, milestone-based triggers

- Personal or parent company guarantees can sometimes substitute for or reduce deposit requirements when available

Renewal and Expansion Options

Renewal options and expansion rights lock in your ability to extend or take additional space at pre-agreed terms. Negotiate them into the original lease or you'll be back at the table with no leverage.

Renewal rent is typically specified as one of three structures:

- Fixed rate: The most favorable for tenants; eliminates future uncertainty

- Fair market value (FMV): Leaves renewal rent open to negotiation at the time of exercise — which can mean paying market rates you didn't anticipate

- FMV with a cap: A reasonable middle ground; protects against dramatic rent spikes while keeping terms tied to market reality

For high-growth companies expecting headcount increases before the original term expires, expansion options — specifically Right of First Offer (ROFO) on adjacent space — can be critical to negotiate upfront, before you need the space and before the leverage disappears.

What Drives Commercial Rent Levels in NYC

Quoted rent per square foot in NYC varies dramatically by submarket, building quality, and deal terms. Without comparative context, tenants often pay above-market or accept unfavorable structures simply because they lack a reference point.

Submarket Benchmarks

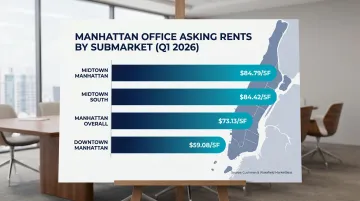

Cushman & Wakefield's NYC MarketBeat report shows significant variation across Manhattan's primary office submarkets:

| Submarket | Average Asking Rent (Q1 2026) |

|---|---|

| Midtown Manhattan | ~$84.79/SF |

| Midtown South | ~$84.42/SF |

| Downtown Manhattan | ~$59.08/SF |

| Manhattan Overall | ~$73.13/SF |

Midtown South (which includes Flatiron, NoMad, and the neighborhoods where Nomad Group has concentrated much of its deal activity) commands pricing on par with Midtown, despite offering more creative and flexible inventory. Downtown remains the relative value play on a per-square-foot basis. The trade-off is typically fewer amenities and different commute dynamics.

Building Class and Its Pricing Impact

According to the NYC Comptroller's office, Manhattan Class B/C space averages approximately $54/SF, while trophy 5-star space averages approximately $100/SF. Class A sits in between, offering newer construction, higher-end finishes, and amenity packages at a premium over Class B.

For growth-stage tech and startup companies, Class B inventory in neighborhoods like Flatiron, NoMad, or SoHo often delivers the best balance of location, character, and cost. The flight-to-quality trend has widened the gap between Class A and B vacancy rates — which can create negotiating leverage in B buildings for tenants willing to look beyond trophy space.

Lease Length and Tenant Credit

Location and building class set the baseline, but lease economics shift further based on term length and tenant creditworthiness. Landlords offer better economics (higher TI, more free rent, lower base rent) to creditworthy tenants signing longer terms. The certainty of cash flow reduces their risk, and they price accordingly.

Startups with limited operating history can offset credit risk through:

- Larger upfront security deposits or LOCs

- Personal guarantees from founders

- Parent company guarantees when a parent entity has stronger financials

- Shorter initial terms with renewal options rather than long commitments on uncertain credit

Common Misunderstandings That Cost Tenants Money

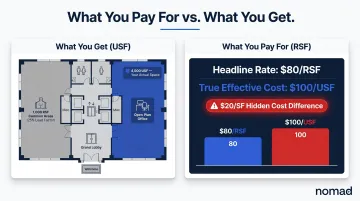

Rentable vs. Usable Square Footage

The rent you pay is calculated on rentable square footage (RSF), which includes your proportionate share of common areas — lobbies, elevator banks, mechanical rooms — via a load factor or loss factor. In NYC office buildings, that factor typically runs 15–30%.

A concrete example: a tenant signing for 5,000 RSF at a 25% load factor occupies only 4,000 usable square feet. If the rent is $80/RSF, you're paying $400,000/year — but your effective cost per usable square foot is actually $100/USF, not $80. That's a meaningful difference when comparing buildings or evaluating space efficiency.

Always ask for the building's BOMA measurement standard and confirm the loss factor before making space comparisons.

Quoted Rent ≠ Total Cost

Many tenants budget based on the base rent per square foot in the listing, then get surprised by additional costs during the lease term. The most common surprises include:

- Operating expense pass-throughs billed separately from base rent

- CAM reconciliations settling the difference between estimated and actual costs

- Annual escalations built into the lease at fixed percentages

- Above-base-year expense increases passed to tenants as building costs rise

By the time all components are factored in, total occupancy cost typically runs 20–40% higher than the headline number.

Nomad Group — with over 2 million square feet of NYC office space managed across 300+ tenant buildouts — helps companies model true total occupancy cost before signing, not after the invoice arrives.

Free Rent Is Not Savings

Free rent represents an economic concession embedded in the overall deal structure, not money you've kept. Landlords who grant 6 months of free rent on a 7-year lease have typically structured the base rent to recover that concession over the remaining term.

Most free rent provisions also include clawback clauses: terminate early and you may owe back every month of abatement received. Know the specific triggers — default, early termination, assignment — before treating free rent as a budget lever.

Frequently Asked Questions

How are lease payments structured?

Commercial lease payments consist of base rent plus additional charges — operating expenses, taxes, insurance, and CAM — depending on the lease type. Gross leases bundle these into one payment while net leases pass them through separately. Most leases also include annual escalation provisions that increase rent over time.

What are the 90% rule and the 1.25% rule in leasing?

The 90% rule was an accounting threshold under ASC 840 used to classify capital leases; ASC 842 replaced it with a principles-based "substantially all" test. The 1.25% rule is an informal heuristic estimating monthly lease payments at roughly 1–1.25% of asset purchase price. Neither applies to commercial real estate lease negotiation.

What is a 99-year lease called?

A 99-year lease is commonly called a ground lease, where a landowner leases the land itself to a developer or tenant for an extended period while retaining underlying ownership. Ground leases are used in commercial development but are rarely relevant to standard NYC office tenants.

What is the difference between a gross lease and a net lease?

In a gross (full-service) lease, the tenant pays one inclusive rent and the landlord covers operating expenses. In a net lease (especially NNN), the tenant pays lower base rent but takes on property taxes, insurance, and maintenance directly — making total occupancy costs less predictable.

What is a tenant improvement allowance and how does it affect rent?

A TI allowance is a landlord contribution toward buildout costs, expressed in dollars per square foot. Landlords typically recover this investment through slightly higher base rent, so tenants should evaluate TI as part of the total economic package — not as a standalone benefit separate from rent.

What does free rent mean in a commercial lease?

Free rent (rent abatement) refers to months at the start of a lease during which the tenant pays no base rent, often granted to offset buildout disruption. Most free rent provisions include clawback clauses requiring repayment if the tenant exits before the lease term ends.