Introduction

Managing office space across multiple locations is a portfolio management problem — one that directly impacts growth, culture, and bottom-line performance. Most scaling companies don't recognize this until they're already in it.

Once your real estate footprint expands from one office to three, five, or ten locations, the operational load multiplies fast. Lease expirations become staggered landmines, operating budgets fragment, tenant improvement costs vary wildly by submarket, and tracking underperforming or overutilized assets becomes a full-time job.

This guide covers what real estate portfolio management is, the core responsibilities portfolio managers shoulder, how commercial portfolios differ fundamentally from residential, the steps to manage one effectively, and the metrics that matter most. Whether you're a corporate occupier managing your own footprint or an investor managing income-producing assets, this guide gives you the framework to manage it with intention.

TLDR

- Portfolio management is strategic oversight of multiple properties to maximize returns and align with business goals

- Commercial portfolios differ from residential through longer leases, complex tenant relationships, and TI allowances

- Asset allocation, performance monitoring, leasing strategy, and risk management form the core responsibilities

- NOI, cap rate, occupancy, and DSCR are the key metrics — tracked continuously

- Diversification across geography, property type, and lease structure reduces concentration risk

What Is Real Estate Portfolio Management?

Real estate portfolio management is the strategic oversight of multiple properties — coordinating acquisitions, leasing, finances, and operations to maximize returns and align with long-term investment or business goals.

Unlike managing a single asset, portfolio managers think across holdings: balancing risk exposure, allocating capital, and tracking performance at scale.

Two types of portfolios require this disciplined framework:

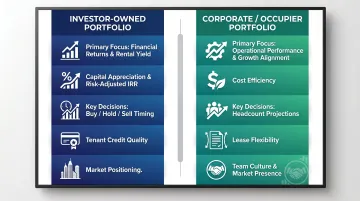

| Portfolio Type | Primary Focus | Key Decisions |

|---|---|---|

| Investor-Owned | Financial returns — rental yield, capital appreciation, risk-adjusted IRR | Buy/hold/sell timing, tenant credit quality, market positioning |

| Corporate/Occupier | Operational performance, growth alignment, cost efficiency | Headcount projections, lease flexibility, team culture, market presence |

According to CBRE, portfolio optimization is the #1 priority for 83% of corporate real estate teams.

Both require the same underlying discipline: tracking performance, reallocating resources, managing risk, and adjusting the portfolio mix as conditions evolve.

That discipline operates against a significant backdrop. The global commercial real estate market was valued at over $38 trillion in 2025, with North America holding more than $13 trillion. At that scale, how you manage the portfolio determines whether it compounds in value or quietly erodes over time.

Real Estate Portfolio Manager: Roles and Responsibilities

Portfolio managers function as the CEO of their real estate portfolios. Unlike asset managers who analyze from a distance, portfolio managers are directly involved in operational and strategic decisions across each property: acquisitions, leasing, budgeting, and dispositions.

Asset Allocation and Diversification

Portfolio managers assess resource distribution across properties, identifying which assets are underperforming and which deserve additional capital. They rebalance risk exposure across asset types, locations, and lease structures. For example, if three office buildings in one submarket all have leases expiring within six months, that's a concentration risk requiring immediate action.

Performance Monitoring and Financial Oversight

Financial responsibilities are active, not passive:

- Approving operating budgets for each property

- Tracking cash flow and net operating income monthly

- Overseeing capital expenditures and renovation timelines

- Ensuring financial reporting aligns with portfolio objectives

Portfolio managers don't just review quarterly reports. They direct where money goes and ensure each dollar deployed generates measurable return.

Leasing Strategy and Tenant Management

Leasing is one of the most value-determinative functions in portfolio management. Decisions about lease length, tenant mix, renewal timing, and rent pricing ripple across the entire portfolio value — not just individual properties.

Data from CBRE shows that renewals accounted for 42% of all office lease transactions in H1 2024, up from 31% pre-pandemic. That means nearly half of all leasing activity is retention-based, making renewal strategy central to portfolio performance.

Large occupiers (10,000+ employees) have a 92% renewal consideration rate compared to 47% for small occupiers. That gap shows how tenant scale shapes portfolio stability — and why leasing decisions can't be treated property by property.

Risk Management and Investor/Stakeholder Reporting

Portfolio managers identify macro and property-level risks:

- Interest rate changes affecting debt costs

- Tenant concentration (one tenant representing >30% of revenue)

- Market softening in specific submarkets

- Upcoming lease expirations creating income risk

They communicate portfolio health to investors or senior leadership through regular performance reporting — flagging risks early while framing them within the broader strategic picture.

Commercial Real Estate Portfolio Management: What Makes It Different

Commercial portfolios operate on a different scale than residential — longer commitments, more complex lease structures, and tenant relationships that directly affect business operations.

Four factors set commercial portfolio management apart:

- Lease length: Prime office leases average 107 months (~8.9 years) versus 86 months for non-prime space. Multi-year terms create income stability, but deteriorating tenant credit becomes a long-term risk.

- TI allowances: Landlords provide per-square-foot buildout allowances. The average TI allowance was $87.51/sf in 2024, down from $97.55 in 2023. In markets like San Francisco, fit-out costs reach $228/sf — making TI negotiations a significant financial lever.

- Lease structure: Triple-net (NNN) leases pass property taxes, insurance, and maintenance costs to tenants. Gross leases bundle everything into one payment. The choice directly affects cash flow predictability and operational burden.

- Occupier priorities: Corporate portfolio managers aren't purely optimizing for yield. They're balancing headcount growth, team culture, and market presence. With 57% of organizations expecting to shrink their footprints over the next three years — 67% citing reduced space needs driven by hybrid work — these decisions carry strategic weight beyond the balance sheet.

For scaling companies in NYC, managing this complexity in-house is costly and time-consuming. Nomad Group works with high-growth companies across Manhattan neighborhoods — from Flatiron to SoHo — handling everything from site selection and lease negotiation to buildout and facilities management. That reduces the operational burden on internal teams while keeping spaces on time and on budget.

How to Build and Manage a Real Estate Portfolio: Step-by-Step

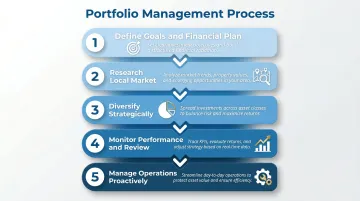

Step 1 — Define Your Goals and Financial Plan

Clarify whether the objective is rental yield, capital appreciation, portfolio diversification, or operational efficiency for corporate portfolios. Your goal determines everything: property type selection, financing strategy, and hold period.

Investor portfolios target specific IRR or cash-on-cash return thresholds. Corporate portfolios target cost per employee, lease flexibility, and alignment with growth milestones.

Step 2 — Research the Local Market

Understanding local supply-demand dynamics, vacancy trends, rental benchmarks, and neighborhood growth trajectories is essential before acquiring or leasing. In commercial real estate, submarket expertise matters.

Consider Manhattan: Madison/Fifth commands $103.95/sf while Downtown averages $56.67/sf — an 83% spread across a single metro. Park Avenue vacancy sits at 10.6% while SoHo reaches 27.4%.

These extreme submarket variations explain why granular neighborhood knowledge — Flatiron vs. Midtown vs. Williamsburg — translates directly into better lease terms and faster site selection.

Step 3 — Diversify Strategically

Diversify across:

- Property types: Office, residential, industrial, retail

- Geographies: Primary, secondary, and tertiary markets

- Lease durations: Stagger expirations to avoid concentrated rollover risk

- Tenant profiles: Mix credit-quality tenants across industries

Balance stable income-generating assets with higher-growth-potential properties. A portfolio entirely composed of Class A offices in one city carries concentrated risk; a mix across asset classes and regions reduces it.

Step 4 — Monitor Performance and Conduct Regular Portfolio Reviews

Track which assets to hold, upgrade, or exit. Benchmark against market data. Adjust the portfolio mix as investment goals or business needs evolve.

Quarterly reviews are the baseline; annual deep dives should follow. Ask:

- Which properties are underperforming their market?

- Where is capital best redeployed?

- Are lease expirations creating near-term risk?

Step 5 — Manage Operations Proactively

Operational management directly drives both asset value and portfolio returns. Reactive management erodes value over time. The core functions to stay ahead of:

Operational management directly drives both asset value and portfolio returns. Reactive management erodes value over time. The core functions to stay ahead of:

- Maintenance scheduling to prevent deferred cost build-up

- Tenant satisfaction to reduce turnover and protect NOI

- Lease renewals tracked 12-18 months out to maintain negotiating leverage

- Capital improvements timed to market cycles and asset repositioning goals

For corporate occupiers, a full-service partner like Nomad Group can absorb this operational load — handling buildouts, facilities, and space delivery so internal teams stay focused on hiring and growth. With 300+ tenant buildouts completed across NYC and a 90-day turnaround, the model is built for companies that can't afford real estate to slow them down.

Key Metrics Every Real Estate Portfolio Manager Must Track

Net Operating Income (NOI) and Cap Rate

NOI is property revenue minus operating expenses, before debt service. It measures the cash a property generates from operations.

Cap rate is NOI divided by property value, expressed as a percentage. It's the foundational measure of property profitability and how one property's returns compare to another's.

For example, a property generating $100,000 in NOI valued at $2,000,000 has a 5% cap rate. NYC average office cap rates reached 5.91% in Q4 2025. Cap rates guide buy/sell/hold decisions — higher cap rates indicate higher yields but often higher risk.

Internal Rate of Return (IRR) and Cash-on-Cash Return

IRR is the long-term expected return on investment accounting for all projected cash flows over the hold period. Because it accounts for the time value of money across the full hold period, it's the most widely used benchmark for comparing deals.

Cash-on-cash return is the annual yield on actual cash invested — calculated as annual dollar income divided by total dollars invested. A return of 8-12% is generally considered solid for commercial real estate.

Together, they reveal the full picture. A property with 6% cash-on-cash but 18% projected IRR may warrant reinvestment over one with 10% cash-on-cash but only 12% IRR — the long-term upside outweighs the near-term yield gap.

Occupancy Rate and Lease Expiration Schedule

Occupancy rate is the primary indicator of income stability. Manhattan overall vacancy sits at 19.9% (approximately 80.1% occupancy), while the U.S. hit an all-time high vacancy of 20.4% — figures that underscore why monitoring your own portfolio's occupancy against market benchmarks matters.

The lease expiration schedule is a forward-looking risk tool. If 40% of your leases expire within 12 months, you face meaningful re-leasing exposure that requires immediate attention. Concentrations of near-term expirations signal where proactive tenant outreach and renewal negotiations should begin.

Debt Service Coverage Ratio (DSCR)

DSCR is the ratio of net operating income to annual debt obligations. It measures whether a property generates enough income to cover its debt.

Formula: DSCR = NOI / Annual Debt Service

A DSCR of 1.25x means the property generates 25% more income than required to service its debt. Most lenders require a minimum 1.20-1.25x DSCR for office properties. Drop below 1.0x and the property can no longer cover its obligations from operations alone — often the first hard signal that a property needs intervention.

Quick-reference benchmarks across the four core metrics:

| Metric | What It Measures | Target Range |

|---|---|---|

| Cap Rate | Property yield relative to value | Varies by market; NYC office ~5.9% (Q4 2025) |

| Cash-on-Cash Return | Annual yield on invested cash | 8–12% for commercial real estate |

| Occupancy Rate | Income stability | Above market vacancy benchmark |

| DSCR | Debt coverage from operations | Minimum 1.20–1.25x (lender requirement) |

Risk Management and Diversification Strategies

Real estate diversification is multi-dimensional. It goes beyond property type to include:

- Spread holdings across cities and regions — economic downturns hit individual markets differently.

- Mix short-term and long-term leases, along with gross and net lease structures, to balance income predictability with flexibility.

- Diversify across industries using SIC codes — a portfolio heavy in retail faces very different risk than one balanced across tech, healthcare, and finance.

Portfolio managers use scenario planning and stress testing to model outcomes under different conditions:

- Rising interest rates

- Economic contraction

- Major tenant departure

For example, the Federal Reserve stress-tested banks assuming a 40% drop in CRE prices. Under that scenario, 55% of banks would exhaust capital buffers. Stress testing identifies vulnerabilities before they materialize and ensures adequate financial reserves.

Too much exposure to a single tenant, market, or asset class leaves a portfolio fragile. Tenant concentration may improve operational efficiency, but it increases idiosyncratic risk — and lenders price that in, typically charging more to finance concentrated portfolios.

That vulnerability is exactly what periodic rebalancing addresses. As market conditions shift and investment goals evolve, even a strong portfolio can drift into over-concentration without active oversight.

Frequently Asked Questions

What is real estate portfolio management?

Real estate portfolio management is the strategic oversight of multiple properties to maximize returns, manage risk, and align assets with investment or business goals through coordinated acquisitions, leasing, financial tracking, and operations.

What are the roles and responsibilities of a real estate portfolio manager?

Portfolio managers handle asset allocation, performance monitoring, leasing strategy, financial oversight, risk management, and stakeholder reporting. They operate as the CEO of their portfolios, making strategic and operational decisions across all properties.

How do you manage a real estate portfolio?

Set clear financial goals, research local markets thoroughly, diversify assets across property types and geographies, track performance metrics continuously, and manage operations proactively. Regular portfolio reviews and rebalancing are essential.

What are portfolio operations in real estate?

Portfolio operations are the day-to-day execution layer (maintenance, tenant management, lease administration, and capital improvements) that translate strategy into property-level performance. They ensure assets stay income-generating and operationally efficient.

What is commercial real estate (CRE) portfolio management?

CRE portfolio management involves overseeing income-producing commercial assets — office, retail, and industrial properties. The focus falls on tenant relationships, lease structures, and aligning space strategy with business objectives or investment returns.

What is the 2% rule in real estate?

The 2% rule is a screening benchmark where a property's monthly rent should equal at least 2% of its purchase price, a higher bar than the 1% rule. It's used to quickly filter for higher-yield investment properties, though it's rarely applicable to high-value commercial office assets.