Market Report: Q3 2025

Executive Summary

Q3-25 Market Update: Demand Remains Resilient, Availability Tightens.

If Q2 2025 felt tight on inventory, Q3 pushed it even further. Leasing availability contracted again, and premium space grew increasingly scarce as tenant demand continued to outpace historical averages.

The market is continuing to pivot toward higher-quality product, underscoring the flight-to-quality trend we saw in Q2. While Q3 may feel a touch more normalized compared to the headline-grabbing momentum of the previous quarter, the underlying strength of demand has proven remarkably strong.

Largest Transactions of Q3

In Q3, Manhattan’s office leasing market showed strong momentum with over 9.5 MSF (million square feet) leased, marking the most active quarter since Q4-19. While many major leases were renewals or expansions, several landlords, particularly those with trophy and Class A assets, secured large transactions exceeding 200,000 squre feet (SF) with marquee tenants such as American Eagle Outfitters, Samsung, Salesforce, and Scotiabank. Notably, WeWork made its first return to Manhattan since bankruptcy filings, signing a 55,000 SF lease at Moinian Group’s 245 Fifth Avenue. The bulk of big leases remained concentrated in premier Midtown assets, reflecting growing tenant preference for quality product in tightly supplied, high-demand submarkets. Vacancy rates began to tighten, and the availability of top-tier, move-in-ready space continues to underpin serious leasing demand.

Deals completed over 50K SF: 22 – 3.1 MSF

Deals completed over 25K SF: 35 – 3.6 MSF

American Eagle Outfitters | 65 Madison Ave | 392,185 SF

American Eagle Outfitters expanded its NYC footprint significantly at 65 Madison Avenue, adding about 54,100 SF to its existing lease, bringing its total to approximately 392,185 SF. This move consolidates multiple brand offices under one roof and marks one of the largest office expansion deals in the city this year. Asking rents for the property are in the high-$70s to high-$80s per squ n are foot (PSF).

Samsung | 277 Park Ave | 316,000 SF

Samsung renewed and increased its leased space, reinforcing the continued value of prime office space in Midtown. This move is another signal from the financial sector that stability and expansion are still very much in play in NYC’s luxury lease market.

Salesforce | 3 Bryant Park | 310,500 SF

Salesforce expanded its lease at 3 Bryant Park in Midtown Manhattan by 71,000 SF, locking in the sublease through 2029. The additional area will be used for training, hybrid work, and customer innovation initiatives. With this expansion, Salesforce now occupies about 310,500 SF in the tower.

Amazon | 1440 Broadway | 259,000 SF

BACK AT IT AGAIN! Amazon has expanded its footprint at 1440 Broadway, signing a deal for an additional 259,000 SF in this Bryant Park office tower, bringing its total space in the building to about 560,000 SF. The property, owned by CIM Group and operated by WeWork, is a 25-story, 745,000-square-foot tower where Amazon is now the anchor tenant. The deal, one of the largest office leases in NYC in August 2025, underscores Amazon’s continued growth in the city despite broader market challenges.

Q3 2025 Builds on Q2 Momentum

Availability on the Decline:

After a record-setting start to the year, Manhattan’s office market entered Q2 2025 with a measured yet powerful stride. Leasing cooled from the Q1 spike but remained historically strong, with nearly 9 MSF transacted.

By the end of the first half, activity totaled more than 20.6 MSF, up more than 36% year-over-year and marking the most active start since 2014. This trajectory set the stage for a pivotal Q3, as the market’s strength continued to show durability.

Sustained Leasing Pace:

Early indications suggest that Q3 pushed forward, keeping Manhattan firmly on track to exceed 40 MSF of annual leasing for the first time since 2019. While the quarter did not feature the blockbuster headline deals of Q1, leasing volumes matched or slightly surpassed Q2 levels, underscoring a market that remains remarkably resilient. Large transactions in the 50,000+ SF range continued, with a mix of relocations, renewals, and expansions shaping the activity.

Supply Pressures Emerge

One of the most defining shifts between Q2 and Q3 has been availability. Manhattan’s overall office availability rate dropped to roughly 16.4% by the close of Q2, down sharply from nearly 20% the year before. Q3 extended this trend, with both direct and sublease availability contracting further. Sublet space, once a hallmark of pandemic-era oversupply, is now shrinking to its lowest point in years, signaling a healthier balance between supply and demand.

Comparing Q2 and Q3

Where Q2 was characterized by breadth of transactions and a moderation from the Q1 surge, Q3 built upon that base with sustained volume and sharper supply-side tightening. Leasing activity in both quarters reflected tenants’ commitment to long-term decisions, but Q3’s landscape leaned more heavily toward strategic moves: renewals, consolidations, and selective relocations, rather than headline-grabbing new entrants. The steady pace of deals has allowed the market to maintain momentum without overheating, suggesting a more sustainable cycle.

What’s Trending in SoHo?

NYC’s Most In-Demand Office Neighborhoods | Q3 2025

SoHo: A Tight Market for a Premium Brand Presence

Over the past 90 days, SoHo’s limited inventory has been absorbed faster with very little replenishment in sight. The 5,000 – 10,000 SF sweet spot is almost nonexistent and much harder to secure as companies are locking in space with unprecedented speed. The race for SoHo lofts is starting earlier than ever. Many of the most desirable, turnkey spaces never make it to broad marketing, and tenants are now locking in renewals far ahead of schedule. Instead of the usual 6–8-month lead time for a 10,000 SF renewal, it’s not uncommon to see discussions begin a full year or more in advance. The competitive tension across the submarket is rewriting the playbook.

The momentum from Q2, driven largely by AI startups flush with new venture capital, accelerated in Q3. Following the example of market-defining players like OpenAI, a new wave of Series A and B companies are positioning themselves in SoHo, cementing the submarket’s role as the epicenter for innovation-driven office users. Among them, Alexis Ohanian’s venture firm, Seven Seven Six, recently leased an entire building at 216 Lafayette Street.

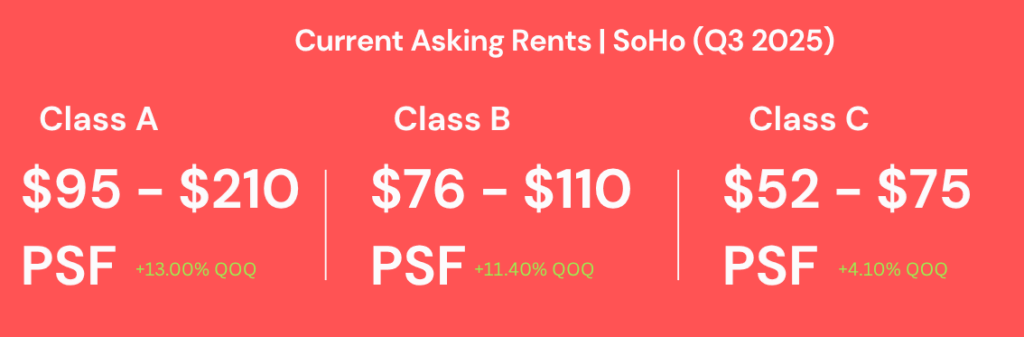

Asking rents continued to climb in Q3, with Class A space now holding steady between $95–$185 PSF, depending on size, buildout, and whether furniture is included. Fully built, plug-and-play offerings on Greene, Spring, and Crosby Streets command the steepest premiums and often lease within days.

Class B assets have also seen notable appreciation, with properties such as 96 Spring Street commanding $95 PSF on the lower levels and reaching $110 PSF on the tower floors (7 & 8).

Nomad’s Choice: 96 Spring Street – Entire 7th Fl (7,415 SF) $68K / Month (Tenant Rooftop👀)

Riding Along Unicorn Lane

NoMad’s Upward Trajectory Holds Strong in Q3

NoMad’s demand remained steady and pricing power continuing to tilt upward across building classes. While verified Q2 data shows the average asking rent climbed from $49.75 PSF in Q1 to $51.00 in Q2, early reports indicate Q3 sustained that trajectory, inched higher ($53.00 PSF) as larger tenants absorbed remaining space. NoMad still offers tenants a substantial discount compared to SoHo, creating urgency as occupiers recognized both the relative value and diminishing availability.

At 799 Broadway, a strengthened tenant roster has left just one office floor available, with asking rents now at $160 PSF, even for the building’s least desirable floor. Despite limited light at the base of the asset due to 801 Broadway’s obstruction along East 11th Street, pricing has continued to climb, and the space is expected to lease before year-end.

As Union Square and Flatiron tightened in Q2, the pull north of Madison Square Park into NoMad only intensified in Q3. The neighborhood continued to distinguish itself as Manhattan’s most balanced commercial submarket, attracting a mix of creative startups, venture-backed firms, and established industry players. This breadth of demand underscored NoMad’s reputation as a hub for design, innovation, and culture and signaled that its surge is not fleeting but sustained. Companies like Grammarly are keeping their roots in NoMad, signing on for 23,322 SF at BXP’s fully redeveloped 360 Park Avenue South, a Class A tower reimagined as a modern workplace destination with world-class amenities.

Class A assets remain in command, with pricing now spanning $105–$160 PSF. Class B has also gained traction, climbing into the $50s PSF, while some landlords pushing higher, most notably at 37 East 18th Street, where new prebuilt’s on lower floors (2 – 4) are listed at $98 PSF.

Nomad’s Choice: 215 Park Avenue South – Partial 18th Fl (12,660 SF) $68.5K / Month

Bryant Park South’s Value Edge

NYC’s Most In-Demand Office Neighborhoods | Q3 2025

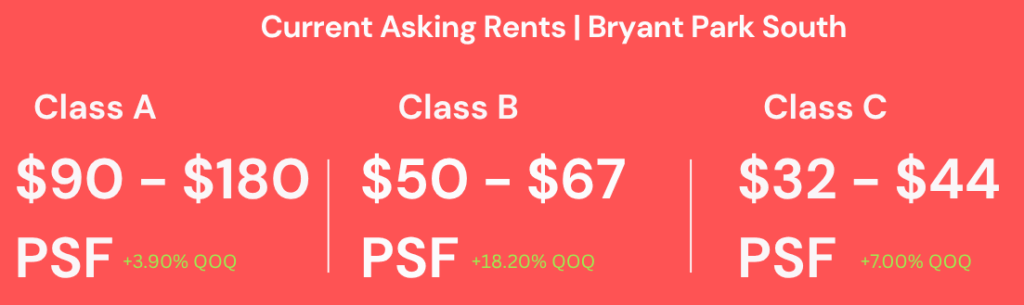

Heading into Q3, the Bryant Park South submarket showed no signs of slowing down. What began as steady in Q2 quickly evolved into a more competitive landscape, with tenants acting decisively and landlords gaining leverage as conditions tightened. The Q2 outlook proved accurate, leasing demand not only held but accelerated, signaling a market entering Q3 with conviction and strength.

Rising Leasing Velocity:

Leasing picked up noticeably heading into Q3, with deals being executed at a faster, more consistent pace. Following a very busy Q2, tenants in Q3 moved with even greater urgency to lock in quality spaces. This acceleration indicates that much of the touring activity and tenant interest generated earlier in the year translated into signed leases as Q3 progressed.

We saw major tenants like Amazon taking down 259,000 SF at 1440 Broadway, just steps away from Bryant Park on 40th and Avenue of the Americas. The expansion brings Amazon’s total leased space in the building to ~560,000 SF and total leased and owned square footage across Manhattan to ~3.4 MSF.

With activity picking up and concessions tightening, Bryant Park South is primed for steady absorption for year end. For tenants who value accessibility, budget discipline, and immediate move-in readiness, this corridor delivers unmatched performance and long-term value PSF.

Nomad’s Choice: 1450 Broadway – Partial 6th Fl (6,919 SF) $35K / Month (Private Terrace😎)

The Nomad Notion

Breaking the Stalemate in Today’s Office Market

By William Janetschek – COO & Co-Founder, Nomad Group

With top-quality spaces already spoken for, bidding wars breaking out, and virtually no new availabilities hitting the market, the pressure is high. For tenants, the search for the right workspace feels more competitive than ever. For landlords, the challenge is how to capture long-term value in an environment where flexibility drives tenant decisions. But instead of adding to the pressure, we focus on solutions.

The Gap in the Market

Many raw spaces hold tremendous potential. Yet here’s the problem: Landlords require 5-year commitments to justify the cost of a full build-out, while high-growth tenants typically only need 2 – 3 years before their business outpaces the space. The core of the disconnect is term length, landlords seek stability, while tenants demand flexibility.

That mismatch creates friction:

- Landlords won’t fund a build-to-suit with a 24-month breakeven on a 3-year term, making them more inclined to hold the space.

- Tenants are forced to assume unnecessary risk (5 Year Commitments) with that outlast their growth trajectory.

This disconnect has long left prime spaces idle even as demand grows.

The Breakthrough

That was the issue… until now. We’ve engineered a model that bridges the gap, aligning landlord investment with tenant flexibility. It unlocks untapped opportunities in raw spaces, accelerates time-to-value for owners, and gives tenants the right-sized commitment they need to grow without being trapped.

This isn’t just about filling space, it’s about redefining how it creates value.

Landlords secure clearer underwriting through term length, tenants gain the right fit with less risk, and the market finds relief where every square foot matters. We achieve this by working with tenants to deliver flexibility through 3 tailored strategies that align landlord objectives with tenant needs.

Download the full report below!

Let’s elevate your workspace—and your future.

Partner with Nomad Group for expert guidance, full-scale support and an enjoyable experience that prepares your team for a thriving future.

Get started

Featured resources

From commercial real estate fundamentals to extensive reports, stay in the know with Nomad Group’s insights, strategies and expert perspectives on office leasing.

Explore resources

Customers Over Everything: Ditch the Short-Term Profit Trap & Build Durable Growth

By Matthew DeRose – CEO, Nomad Group In hip‑hop, “Money over everything” might be a flex. In business, it’s a…

From Flex to Flagship: Knowing When to Make the Move

By Matthew DeRose – CEO, Nomad Group Coworking vs. Private Office Space: What CEOs Should Really Be Thinking About When…